Since the beginning of 2012, gold has trailed its precious metals peers, gaining only about 6 percent compared to double-digit returns for silver and platinum. At the end of February, gold was especially hard hit, following Ben Bernanke's announcement that there would be no additional quantitative easing and the European Central Bank offering additional LTRO loans to banks.

With this news, we've witnessed the fairly rare event of bullion falling below its 200-day moving average. In fact, over the past 10 years, there have only been about 30 times (or around 3 times per year) where gold has fallen below its 200-day moving average. And each time, gold has been down for the count for only an average of 10 days. This time around, I believe gold has the resilience to endure, as the long-term drivers remain in place.

In his latest Gold Monitor, Dundee Wealth Economics Chief Economist Martin Murenbeeld lists eight factors in support of the bear argument. He points to a stronger dollar, fiscal retrenchment in the European Union, improving equity market confidence, and an exit strategy from the Federal Reserve forecasting a federal funds rate hike well before late 2014 as significant factors driving gold lower.

Dr. Murenbeeld adds a caveat: while this bearishness may be a "new, exciting story" for the markets, it doesn't make the case for gold any less compelling. In fact, he "anticipates market sentiment to flip back to the bullish half of the story as the year progresses."

On the bullish side of the ring, Dr. Murenbeeld says there are 10 positive factors for gold, one of which is monetary reflation. I've discussed how global money supply has been growing in recent months, which provides liquidity for the market, but also can devalue the currency. Dr. Murenbeeld reminds readers that "money doesn't grow on trees; it will have to be borrowed by some government and/or it will have to be printed by some central bank."

While in Hong Kong, Global Resources Fund Portfolio Manager Brian Hicks appeared on Bloomberg to talk about the drivers for oil and gold with John Dawson earlier this week. For gold, Brian says the positive factors are alive and well, namely, rising wealth in China, Europe's financial instability and high fiscal deficits in the U.S.

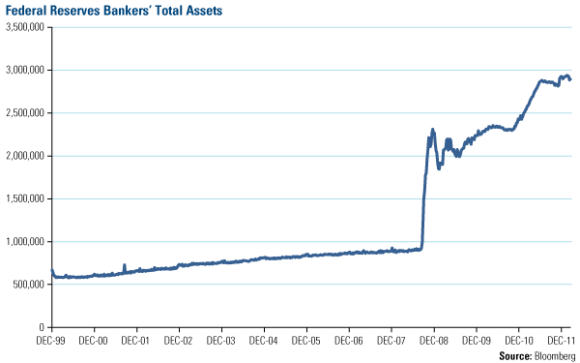

The U.S. debt situation hasn't been on investors' radar for a while, but it's still a significant factor in gold's eventual recovery. Take a look at the chart below, which shows the condition of all Federal Reserves Banks' total assets over the last 10 years. During 2008, total assets jumped vertically and since then, the Fed's balance sheet has maintained a much higher level.

In addition, real interest rates are still negative for many areas around the world. Historically, negative real interest rates (the inflationary rate is greater than the current interest rate) combined with global stimulative money supply efforts have been an especially powerful combination for gold prices.

I believe the yellow metal will go the distance, and with bullion below its long-term average, it makes for a rare and attractive entry point for investors today.

Please consider carefully a fund's investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Distributed by U.S. Global Brokerage, Inc.

Foreign and emerging market investing involves special risks such as currency fluctuation and less public disclosure, as well as economic and political risk. Because the Global Resources Fund concentrates its investments in a specific industry, the fund may be subject to greater risks and fluctuations than a portfolio representing a broader range of industries.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Frank Holmes, U.S. Global Investors