IF YOU'VE BEEN paying attention, then you'll remember how gold can make financial crises fun. Gold bulls were so short of things to keep them awake at night, in fact, many will no doubt be grateful for the 20% plunge of late 2011. Y'know, just to keep their hand in.

"We think the peak would be towards the end of this year or maybe some time in the first half of next year," says Neil Meader, research director for Thomson-Reuters' 2011 acquisition, the GFMS precious metals consultancy.

The trigger for gold's final top and decline? "Anything that really signals to the market that the structural imbalances and the various problems affecting the strength of various currencies are moving behind us, that we are moving beyond this current financial crisis situation," says , speaking to TheStreet after launching GFMS's latest Gold Survey Update in New York on Tuesday.

Now, whatever you make of that risk, gold investors should perhaps be pleased to see the world's leading data and analysis provider flagging such an event. Like pullbacks in a bull market, it can only be healthy to consider the inevitable end.

In particular, says Neil Meader, "One overt trigger that is worth looking for is the start of a serious ratcheting up of interest rates. Because, for gold investment to be popular, you do need really low interest rates."

Of course, the risk of higher interest rates look about as high right now as interest rates themselvesi.e., zero. Even where the cost of borrowing or the return on cash is better than nothing, it isn't after you account for inflation. And as BullionVault never tires of reminding people, it's that ratethe real rate of interestwhich really matters to the ebb and flow of gold demand in the end.

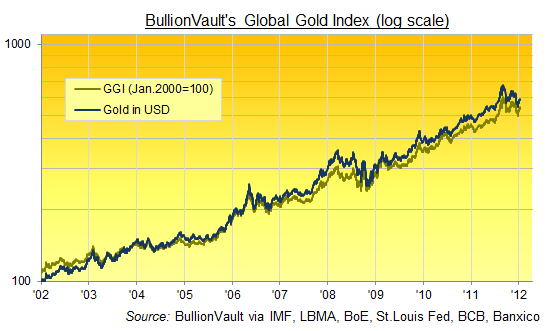

Hence the rise in global gold prices, rather than just in Dollars, over the last decade. It shows clearly in our Global Gold Index, mapped above. The GGI prices gold against a weighted basket of the world's top 10 currencies, as measured by the size of their issuing economy. It's risen fivefold over the last decade, just like the S&P index of the 500 largest US corporations did in the 1990s. Unlike the S&P, however, gold hadn't already risen fivefold in the 15 years previous.

Still, this run cannot continue indefinitely. And pending the big downturn in gold prices apparently nailed on for end-2012or early 2013, or maybe a bit after, if not whenever this financial crisis is finished and things get back to what we used to call normalhere are three things likely to make gold owners reach for the Valium at some point or other:

#1. Europe

Oh sure; gold offers unique insurance against default or devaluation, because it can't be created or destroyed, and it is no one else's liability to renege on (so long as you own it outright). Short term, however, a credit squeeze is likely to force up the Dollar and drain liquidity from derivative markets, including gold futures. Repeating the impact of Lehman's 2008 collapse, Europe's credit crunch in the second-half of 2011 forced the collapse of broker MF Global, further helping the speculative position in US gold futures fall in half. That's certain to dent prices short term, even if gold investment demand for physical bar and coin is surging for fear of the political and monetary reaction.

#2. China

The middle kingdom is supposed to be an unalloyed good for gold prices. Disappointing both GFMS and ourselves by failing to take out India's top spot in 2009, it's likely to stand closer still as world #2 in 2012. But unlike investors here in the developed West, Chinese gold demand clearly shows a significant and positive link with economic growthand no one yet knows how a credit squeeze or "hard landing" might affect the globe's fastest-growing demand for physical bullion. Our guess is that tight credit and stalling income growth wouldn't be good for gold. Beijing's response might be, however, if 2008-2009 is a guide.

#3. Volatility

Guaranteed in 2011, volatility in gold prices still lagged US equities, but that's small comfort if you imagined owning gold really would let you sleep through the night. Owning physical property, in law, means you escape credit, not price risk. Scarier still for retained wealth trying to hide from the storm in gold, volatility is known to dent India's household buying, the world's largest single source of demand. Imports fell 8% by weight in 2011, thanks to a near-collapse in the final 3 months. There's also a plain risk thatafter rising each year since 2001the recent whip-sawing of the gold price might dissuade Western investors, too. After all, if gold is supposed to be a "safe haven" amid any event, it failed in the second-half of 2011, even though it's tripled during this five-year crisis so far.

There, all that noise should help keep you awake tonight. As for tomorrow, there are plenty of other nightmares threatening your wealth elsewhere. Surging real interest rates paid to your cash savings shouldn't be one of them.

Please Note: This article is to inform your thinking, not lead it. Only you can decide the best place for your money, and any decision you make will put your money at risk. Information or data included here may have already been overtaken by eventsand must be verified elsewhereshould you choose to act on it.

Adrian Ash

BullionVault