In 2001, the Chinese government lifted its final controls on the gold market, releasing a pent-up demand that since then has become stronger. From 2001 to 2010, China's annual consumption of gold grew at a 7.5% compounded annual growth rate. This chart shows how China's demand for gold jewelry has increased from just over 15.55 tonnes (500,000 ounces [oz]) in the late 1980s to over 373.25 tonnes (12 million oz) at the end of 2010, in spite of gold going from $200 $1,650/oz.

At the same time, China has emerged from a minor global player economically to the second largest economy in the world, with its sights set on being the largest. With its breakneck growth of around 10% per annum over this time, the transformation in China has been the envy of the rest of the world. Alongside this growth has been a transformation of Chinese society. From a working class society, we're seeing the burgeoning growth of the Chinese middle class with a commensurate growth in income.

To the gold market, a more important statistic is the spending and saving patterns of China. Like the Indian population, Chinese people are generally thrifty, inclined to save rather than spend disposable income. The Chinese government has always approved of their saving nature, but they have until recently only had bank deposits as a safe place to save. Inflation has robbed many of the benefits of savings and the stock exchangenot for the ordinary middle-class man across Chinahas been too much of a gamble.

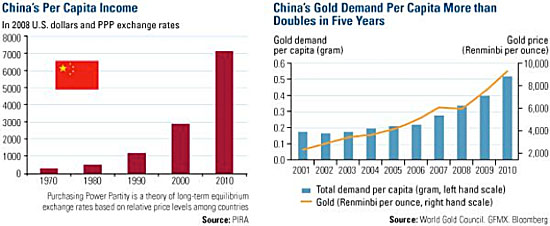

Then the government not only lifted all restraints on the gold market, but also actively encouraged gold buying while stimulating the development of a nationwide gold distribution system through their leading banks. The number of foreign banks now allowed to import gold has jumped. As the system of distribution has reached countrywide, the choice of gold as a savings option has grown. Over time, the rise of the gold price to the extent that they've seen (i.e., their savings in gold grew much faster than inflation) has confirmed the wisdom of gold as a prudent savings and investment means. Their traditional respect for gold as money was established in past generations, and continues right through to this day, now with government blessing. Consequently, since the gold price took off in 2005, on a per capita basis, investment in gold in China has more than doubled since 2005. Demand for gold as an investment has grown at a 14% annual pace since the Chinese government deregulated the local gold market in 2001.

The Rise of the Chinese Middle Class

The rise in gold prices and consumption has coincided with a dramatic rise in China's per capita income. As you can see from the chart on China's per capita income from 1970 to 2010, the Chinese suddenly have a life. The rise from the $3,000 level in 2000 to roughly $7,000 in 2010 has resulted in the rise of a middle class that is enjoying choices it has never had before.

In 2010, China became second only to the U.S. with a middle class population of 157 million (M) people, according to the Organization for Economic Co-operation and Development (OECD). Since then it has continued to grow at a rapid pace. With the U.S. middle class comprising roughly half its population and China with a population at 1.4 billion (B) people and the U.S. at 300M, the future holds the possibility of a middle class being larger than the population of not only the U.S. but also the Eurozone's 400M people (i.e., 700M people). Yes, its mind-boggling!

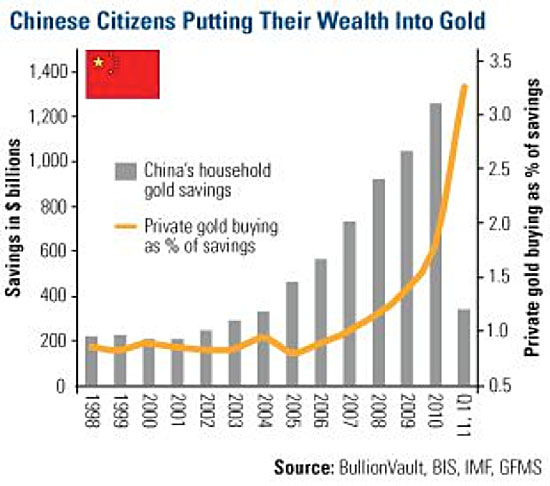

So not only will the Chinese middle class grow, but its disposable income will grow too. As you can see in the chart on the growth of the percentage of its savings entering the gold market, this percentage will keep risingthis tells us that our projections are likely to prove conservative!

Chinese Buy Physical Gold (Not Derivatives or Gold Shares)

A dramatic difference between western investors and Asian ones is the belief in the metal itself and not a derivative that is "related" to gold. All these savings in Asia are headed into the physical metal. In the developed world, only a small proportion of investment funds find its way into gold bars, coins and pure gold jewelry. Consequently, the U.S. accounts for only 8% of gold bullion demand, whereas Asia accounts for more than 70% of gold coin, bar and pure gold jewelry demand. What impact will this have on demand for gold?

With a rising percentage of savings going into gold and a middle class capable of growing to twice the developed world's middle classes, potential gold demand in China has the capacity to grow to over 3,000 tonnes per annum.

The fact that the People's Bank of China is buying all local production makes it clear that there will not be enough gold available to accommodate this demand.

Impact on Total Global Gold Demand

Total annual mine production, at below 3,000 tonnes, is insufficient to satisfy such demand, and with scrap gold supplies at around 1,650 tonnesnot necessarily the amount available in future yearsit is impossible to escape the conclusion that the future for gold is to see prices rise to the extent that is prompts current holders to sell. Add to Chinese demand that of the rest of the world, and we can see that prices have to rise to moderate future demand to the point that demand matches this supply levelfor there just aren't any more major easily mined gold deposits out there to grow supply to this extent.

Please note that these numbers have ignored central bank activity in the gold market. These numbers have also ignored any reformation of the global monetary system, which may include an incorporation of gold to bolster confidence in currencies. (Some countries may feel it necessary to confiscate their citizens' gold for this purpose too.)

China as Gold Hub

From these extrapolations, we can see that China, in time, will become the heart of the gold world. The Chinese government is moving toward China controlling what it deems important. This includes the gold market. Already we're seeing reforms to ensure that the gold market holds its standards high and ranks next to the professionalism of London. With demand at its current levels, gold imports unrestrained and its own gold production now the world's largest national production level, China is inexorably moving to the heart of the gold world. It's therefore expected that China will aim to do what it can to exercise administrative dominance over it.

Current gold market professionals and market makers would do well to learn Mandarin Chinese. . .

Julian Phillips, Gold Forecaster

Members only: Changes to the Gold Market / Asia Gold FIX

Get the rest of the report. Subscribe @

www.GoldForecaster.com / www.SilverForecaster.com

Legal Notice / Disclaimer

This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Gold Forecaster - Global Watch / Julian D. W. Phillips / Peter Spina, have based this document on information obtained from sources it believes to be reliable but which it has not independently verified; Gold Forecaster - Global Watch / Julian D. W. Phillips / Peter Spina make no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Gold Forecaster - Global Watch / Julian D. W. Phillips / Peter Spina only and are subject to change without notice. Gold Forecaster - Global Watch / Julian D. W. Phillips / Peter Spina assume no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, we assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information, provided within this report.