For that group, and for people new to the space that may just own a few hundred shares of a closed end fund or ETF, I am going to do two posts on the popular misconceptions I have encountered over the years. There will be at least 10, starting with 5 in this post. Feel free to add more misconceptions in the comments section below, or to correct me on anything I may be confused about. . .

MLP Misconceptions

1. MLPs are toll roads

A very prevalent way to describe MLPs is that they are essentially like toll roads for oil, natural gas and refined products. The idea is that the MLPs are like toll roads because they dont take commodity price risk, only get paid a fee to have commodities flow through their pipes. Toll roads don't carry the risk of whatever goods get trucked through their turnpikes, they just get tolls to maintain the road and provide access to markets for the goods and services being trucked along the toll road.

(Note: Toll roads are peripherally affected by commodity prices in that they could be affected by decreased demand from carpooling or conservation if gasoline got too be much more expensive, but if we're talking about trucking along toll roads, that increase in gasoline prices will be passed along to end users through higher prices, rather than result in much conservation, the last 3 years of data notwithstanding. . .)

While there are many MLPs that do not have direct commodity price exposure, almost all of them have businesses that are influenced by commodity prices to some degree. Some MLPs that get painted with the toll road brush have direct and significant exposure to commodity price changes.

Understanding that not all MLP assets are created equal is very important. For example, if you hear Jim Cramer refer to LINN Energy LLC (LINE:NASDAQ) as a pipeline partnership (which he has before), you might think LINE has limited commodity price exposure, when it obviously does have commodity price exposure. That's not so bad, but if a broker starts to talk that way in recommending a particular MLP to a client, it becomes a problem. I'm sure most of you do your homework, but I'm also sure there are plenty of you who have at some point bought a stock without doing adequate research. . .all MLPs are not created equal and are not toll roads, know what you are buying (or hire someone like me to know for you).

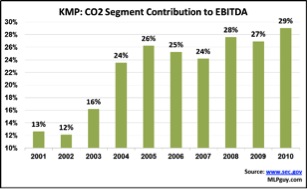

Also, often overlooked is the extent to which these relative commodity price exposures vary over time as the MLPs change the business lines they are in. Take Kinder Morgan Energy Partners ($KMP) for example. Historically, KMP owned assets with very limited commodity price exposure. Over the last decade, KMP's CO2 business, which carries direct commodity price exposure (approximately 72% of that segment is driven by oil production), has grown to represent close to 30% of EBITDA in 2010, up from 13% in 2001, as shown below.

This goes the opposite direction as well. Regency Energy Partners ($RGP) and Williams Partners ($WPZ) are good examples of MLPs that have less commodity price exposure than before as result of acquisitions and growth projects. According to a recent company presentation, $RGP will earn 82% of its segment margin from fee-based activities in 2011, compared with 71% in 2009.

All that being said, in general as a group, relative to the oilfield service sector or the exploration and production sector, MLPs have less commodity price exposure.

2. MLPs cannot be purchased in a retirement account.

Retirement accounts are tax-free accounts. The primary reason not to own MLPs in tax-free accounts is they generate (in varying degrees, depending on the MLP—some don't generate much UBTI at all) unrelated business taxable income (UBTI). There is a $1,000 exemption, meaning if you have less than $1,000 of annual UBTI, then you are not liable for any taxes. If you get more than $1,000 in annual UBTI, this may cause the account to be liable for taxes. The tax rates aren't outrageous (it's a graduated scale that starts at 15%), however, and if you can coordinate with the retirement account sponsor to get the taxes paid (their responsibility), it can be worth the trouble given the returns MLPs have had over the years.

3. MLPs are required to distribute all of their cash.

MLPs must earn at least 90% of their income from MLP qualifying sources, but there is no requirement on how much they must pay out. Real estate investment trusts (REITs) are required to distribute 90% of their taxable income to investors. The similarities of REITs as yield vehicles and the 90% number probably confuse people, which is understandable.

The phenomenon of MLPs distributing virtually all of their available cash is a function of their history and what the market has proven to bear. MLPs were initially sold as income vehicles, and the market valued them almost exclusively using relative yield metrics. Therefore, to get the best possible valuation for a partnership, bankers and management teams needed to structure the partnership agreements with distribution policies specifying that the MLP would distribute as much cash as possible.

Much of the retail market that invests in MLPs is still attracted to the high yields MLPs have, but many in the industry have started to recognize value for MLPs that retain cash flow and therefore can fund ongoing capital projects out of cash flow as opposed to purely through the public markets. $EPD and $ARLP are the best examples of this in the sector today. Also, these days, with yields on everything else so low, the smarter MLPs are realizing that the market will still view a 6% yield as attractive, even if they could afford to pay a distribution that would result in a 7.5% yield. In a more normalized interest rate environment, with the interest rate on the 10-year treasury above 4%, I would bet that MLPs would not get as much credit for carrying high distribution coverage.

4. MLPs are a Ponzi scheme.

People I speak with about MLPs sometimes jump to the conclusion that just because MLPs must access the capital markets to grow distributions, that therefore if MLPs don't have access to capital, they will have to cut distributions. I've even heard some people refer to MLPs as a Ponzi scheme. As I've written about here, there are times when the financial engineering and IDR manipulation may seem shady, but that doesn't make MLPs a Ponzi scheme.

In a Ponzi scheme, when the new money stops flowing in, the scheme falls apart and the schemer is unable to meet obligations to the old money. When the capital markets are closed to MLPs, they should be able to maintain distributions indefinitely. See the difference?

MLPs that depend more directly on declining assets should be booking maintenance capex (and reducing cash flow available for distributions with it) on an ongoing basis that accounts for all capex needed to replace lost cash flow from decline in assets. That's why you'll routinely see maintenance capex levels for gathering and processing MLPs at 20%+ of EBITDA, as compared to traditional pipeline MLPs that can have maintenance capex that is less than 10% of EBITDA. Gathering and processing MLPs have to spend money every year to hook up new wells, and build more small pipeline to connect the wells. Long haul, large diameter pipeline operators don't have to spend as much to maintain cash flow.

Either way, assuming that an MLP has properly accounted for the capital expenditures required to maintain cash flow, and assuming that their business fundamentals stay intact (i.e. not huge drop offs in pipeline volumes), then not having access to capital markets will not cause an MLP to cut its distribution. This was proven pretty soundly in late 2008, early 2009 when only a handful of MLPs cut their distribution and many of them actually raised distributions.

5. MLPs allow you to avoid taxes altogether.

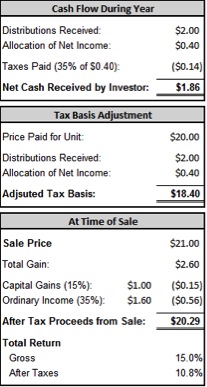

MLPs allow you to defer paying taxes on most of the distributions you receive. That deferral is a result of some of your cash being considered return of capital, which reduces your tax basis in the MLP. When you go to sell that MLP at some point in the future, the difference between what you originally paid for the MLP and your tax basis is considered ordinary income and will be taxed as such. Then, you will pay capital gains taxes on the difference between what you sold the MLP for and the original price you paid for the MLP. See below for a simplified example of what taxes you would pay if you purchased an MLP yielding 10% for $20.00, with 80% estimated tax shield, held it for a year and sold it for $21.00.

So, eventually, the tax man gets his pound of flesh, with the exception being (under current rules), if the MLP owner never sells the MLPs, and passes along the units to an heir who gets stepped up tax basis, washing away the built in gains.

That's it for now, but here is the list of other misconceptions to be covered in Part II:

- MLP price changes are uncorrelated to the broader stock market

- MLPs can't be purchased by foreign investors

- Rising interest rates automatically and immediately means rising yields (lower valuations) for MLPs

- MLP cost of capital is equal to its equity yield

- The best way to value MLPs is using relative yield

- MLPs with high GP takes are inherently unattractive

Disclosure: The information in this article is not meant to be financial advice, we are not your financial advisor and I am posting my comments for informational purposes only.