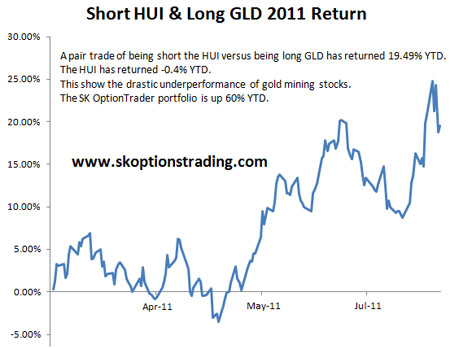

These past few weeks have affirmed our view that gold stocks are not a suitable vehicle for trading or investing in gold at the moment. We have held this view for a few years now and see no reason to change it, regardless of how undervalued mining stocks supposedly are. The chart below shows the performance of a pair trade which is short the HUI gold miners index and long GLD for 2011.

This shows the drastic under-performance of mining stocks. Of course there may be some individual gems in the sector that have done very well, but overall the sector continues to perform poorly. The fact that one could have made nearly 20% this year by being short mining stocks and long gold demonstrates the magnitude of this under-performance. If miners are indeed the best vehicle for trading or investing in gold, then one should be able to make a profit by being short gold and long the mining stocks, since their gains should outperform gold. However in reality they aren't outperforming, in fact they aren't even keeping pace, and therefore we will continue to avoid them as a trading vehicle.

A fair amount of this under-performance can be explained by the fact that gold mining stocks are still stocks; they are not gold. In a flight to safety investors by gold, not mining stocks and when the stock market tumbles, gold mining stocks will be sold off too. This has been evident in recent weeks and in fact throughout 2011 the HUI has only exhibited a 0.2 correlation to gold prices. We continue to think that options are the best vehicle for this environment. Options on GLD can be traded just like any other stock option.

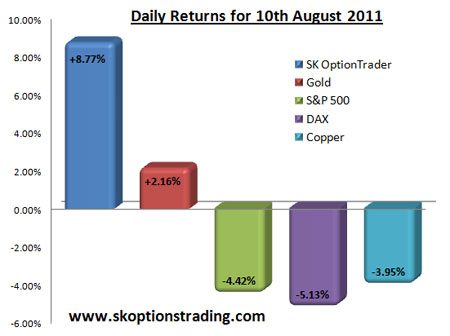

The above chart shows what a turbulent month August has been so far, with a massive risk off sentiment driving money from stocks to treasuries and other safe havens. The S&P 500 has lost 9%, copper is down 11%, gold is up 8% and there have been similar violent moves in other markets. However our SK OptionTrader model portfolio has fared well despite this turmoil, showing a gain of 16.5% for August. On days when other markets were plummeting, such as August 10th, our portfolio was making strong gains.

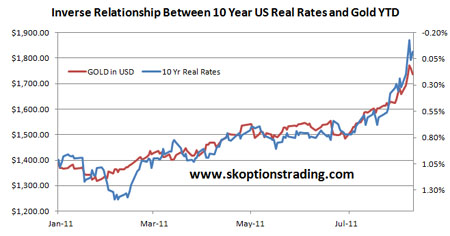

As our regular readers will know, we view U.S. interest rates as the key determinant of gold prices in the medium to long term, with U.S. real rates being particularly important. We view gold as a currency and since currencies are tightly linked with interest rates, we have a large focus on the U.S. and global interest rate market.

Gold prices have an inverse relationship with U.S. real rates and our view has been that a decline in U.S. real rates would send gold past $1800 (Please see our article on July 18th entitled "Decline In U.S. Real Rates To Send Gold Past $1800").

This scenario has indeed now come to pass, with U.S. real rates substantially lower and gold prices significantly higher. Whilst we think that gold prices are vulnerable to a correction in the short term, over the longer term the U.S. interest rate environment still points to much higher gold prices. Even with U.S. real rates at current levels, $2000 gold is not an unrealistic target in the next few months. Further declines in U.S. real rates would present an upside risk to that target.

It is all very well to say that lower real interest rates send gold prices higher, but this hypothesis can produce little in the way of actionable information unless we have a view on where U.S. interest rates are going in the future.

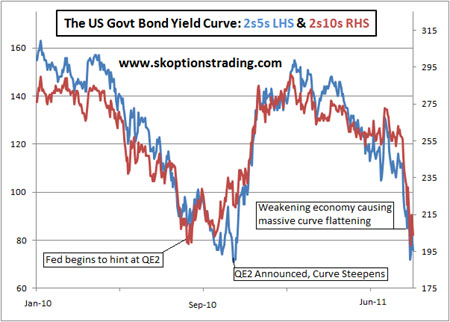

Our view was that a flattening of the U.S. yield curve, which we viewed as a symptom of economic weakness, would prompt further easing by the Federal Reserve.

For those readers who may be unfamiliar with how the yield curve works, we will provide a brief explanation. Bonds of different maturities have different yields. By plotting these yields against their maturities we can build a yield curve. The yield curve becomes steeper if longer term interest rates increase relative to shorter term interest rates. The yield curve becomes flatter if longer term interest rates decrease relative to shorter term interest rates. One way to measure the steepness of the yield curve is to look at the difference between the yields at two different points on the curve. For example one may look at the difference between the yields on 2 year Treasuries compared to the yield on 5 year Treasuries. Such a comparison will often be referred to as "2s5s" and is measured in basis points (bps) by subtracting the shorter term yield from the longer term yield. So if one says "2s5s are trading at +225" this means that the yield on 5 year bonds is 2.25% higher than the yield on 2 year bonds. If 2s5s go from +225 to +275 then the yield curve has steepened between those two maturities. If 2s5s go from +225 to +175 then the yield curve has flattened between those two maturities.

There is no one exact interpretation of what causes shifts in the yield curve. The curve changes with changes in inflationary expectations, default risk, equity markets, the outlook for future interest rates as well as other factors.

However in our opinion the run of poor U.S. economic data had been causing the curve to flatten. A weaker economy means that interest rates will probably be held lower for longer, therefore longer term interest rates fall relative to shorter term interest rates, causing a flattening of the curve.

In our article on August 3rd entitled "U.S. Yield Curve Flattening To Prompt Fed Easing" we commented that we did not think the Fed would immediately jump to QE3, but other forms of monetary easing that they would implement would still have the same effect bullish implications for gold prices:

"First we would expect to see a change in the language of the Fed statement, a change that implies that interest rates will remain lower for longer. We then could see the Fed setting a cap on longer term interest rates, such as the 2 year or 5 year rate on Treasuries. All these forms of monetary easing are massively bullish for gold prices."

The scenario unfolded with the latest Fed statement, where Bernanke pledged to keep interest rates low until mid 2013, effectively capping the 2 year rate on Treasuries. This also decreased interest rates at all maturities and sent U.S. real rates into a nosedive, whilst gold skyrocketed.

Moving on, from a psychological standpoint we are beginning to see signs that warrant caution going forward. We are not saying that gold is in a bubble, we are still very bullish on gold prices over the medium and longer term, but we are approaching bubble territory. Just last week I was asked about how to invest in gold by a lawyer and a snowboarding instructor on separate occasions. This follows overhearing a conversation about what a great investment gold is between a florist and an architect, including an eye popping quote that "you will always make money" investing in gold. We point out the respective professions of these people simply to demonstrate that those talking about gold are not in the investment industry, and normally never mention anything to do with the financial markets whatsoever. Combining this with gold being increasingly mentioned on CNBC and advertisements on TV here in New Zealand promoting gold investment has our alarm bells ringing. The TV advertisement promotes buying gold bullion as a safe investment with a general upward trend over the last ten years. This is eerily similar to the talk regarding real estate when the property market was in full swing.

However the key difference is that although gold is certainly being talked about more, those talking aren't yet putting their money where their mouth is. Although the amount that gold is talked about may be causing us some concern, the degree to which it is owned is not. When those people mentioned above are all talking about how much they are making from their gold investments, then gold will be in a bubble and it will be time to sell. At present, this is merely a warning shot across the bow of this bull market and therefore is a situation that we are monitoring closely.

Looking to the composition of those investors that were flocking to gold in recent weeks, we think they can be classified into two main types. Firstly there were those looking for a safe haven, a hedge against the turmoil that was gripping other markets. In human psychology, nothing sparks fear like uncertainty. One only has to watch a classic horror movie to see evidence of this. The monster doesn't create as much fear as the shadow that the monster forms, when we are unsure what the monster is. Markets were not sure of anything in recent weeks and this uncertainty is what was driving fear and creating carnage across the financial markets. Since gold does not have a central bank or government backing it, there is no uncertainty over what will happen to this currency. No central bank can cut its interest rate and no government can print gold to dump on the market, therefore gold was a safe place to be.

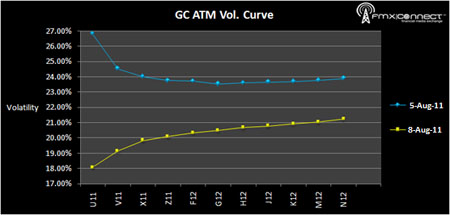

Secondly there were the speculators, who were not looking to hedge any other positions, but merely there to make a profit. A symptom of this speculative buying was evident in the gold options market. One of the more remarkable developments of the last week from our viewpoint was not the increase in volatility, but the change that we saw in the volatility curve for gold. This curve plots the volatility implied from the options market at different dates in the future. As the chart below shows (courtesy of FMX Connect), not only did the vol curve rise, it was actually flipped on its head. The term structure of volatility went into backwardation, a very, very rare occurrence in the gold options market.

This was a result of a dramatic spike in the demand for speculative calls near term, with a significant portion coming from retail investors. This backwardation was never likely to last however, since there was an arbitrage opportunity to sell near term volatility and buy longer term volatility with the aim of benefiting from a normalization of the term structure. However with the chaos taking place in all areas of the markets, traders did not quite have the temperament to fight the backwardation in volatility right away. As of the close on Friday the curve has now flattened and we appear to be returning to a more normal situation. Our subscribers were fortunate enough to be able to capitalize on this situation via our options trading recommendations. For more information on how to subscribe and to view our full trading record, please visit www.skoptionstrading.com

In conclusion there is still significant upside in the medium term for gold prices. We expect gold prices to move significantly higher over coming months, even if currently the yellow metal looks overextended and vulnerable to a correction in the short term. We still believe that gold stocks are not a suitable trading or investment vehicle for gaining exposure to rising gold prices. We continue to think that options trading is the best way to profit in this market environment, simply because trading options allows one to tailor trades to match one's market view. Futures, ETF's and stocks generally force the trader to simply bet up or down, whereas options are far more versatile and we think today's market environment demands versatility more than ever.

The SK OptionTrader model portfolio is up 389.58% since inception, boasting an annualized return of 119.37%. We have banked an average return of 42.47% per trade including losses, over our 84 closed trades. 81 trades were closed at a profit, 3 at a loss, a success rate of 96.4%. On average our trades remain open for 45.33 days.

Our service provides clear trading signals that are simple to understand and sent during the trading session at prices that are real in the market at the time of sending. A suggested capital allocation accompanies each trade and a model portfolio is produced for subscribers. We also provide regular market updates that outline our view on the market and give advanced notice of our trading strategy going forward.

Disclaimer: Gold-prices.biz or SK Options Trading makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents our views and replicates trades that we are making but nothing more than that. Always consult your registered adviser to assist you with your investments. We accept no liability for any loss arising from the use of the data contained on this letter. Options contain a high level or risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. Past performance is not a guide nor guarantee of future success.