We'll preface those comments in turn by stressing the debt crisis in Europe is very fluid. This is a crisis of confidence as much as anything else. Markets will be highly volatile and subject to reversals on every bit of news, rumor or innuendo until traders decide to take a time out. We're about to find out how good Europe's political class really is at calming a crowd. Their track record hasn't been great but if nothing else the latest market dives should add some immediacy and focus to the political tussles. That's a good thing, even coming at the expense of a market drop.

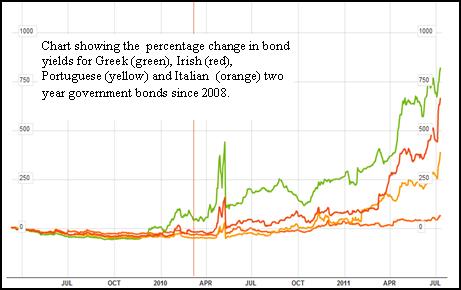

The bond vigilantes are making the rounds again in Europe. You could almost hear them saying "you're next" to Italy as they continued to trash other PIIGS sovereign debt issues. The chart below depicts the percentage change in bond yields for the hardest hit EU members over the last three years. Italy's bonds look stable by comparison but that is misleading;

Italian bond yields have risen about 50% in the past week. As this issue was being completed Italy sold one year bills at a yield of 3.67%. This compares to a yield of 2.15% at the last auction a month ago. The fact that both the Euro and the Milan stock exchange moved up smartly after this auction tells you how much fear there is in the markets.

Yields on 10-year Italian bonds ran up through the 6% level that is considered unsustainable prior to the auction, though it has fallen back since. The Euro has continued to rally, as have other markets and gold after Italy's leadership promised to get serious (again) about austerity measures.

Yields on Greek and Irish debt indicate traders expect both of these countries to default, period. That outcome would not surprise us. We expected, and saw, a deal in Greece but no one other than a handful of core EU political leaders and Eurocrats view this as more than extend and pretend.

Italy is a much bigger potential problem, having far larger debt balances, but it's really not in quite the dire straits that Greece and Ireland are. Italy has larger domestic ownership of its debt load and higher savings rates that could allow it to take over more of the outstanding debt. That said, it also has low growth and productivity and a political class that is a running farce more adept at providing titillation than leadership. Italy is in a better position to convince the markets that its Mediterranean neighbors, if its stops dodging and dawdling and gets on with it. Italy's finance minister, who seems the most capable guy in the room by far, pledged to pass austerity measure by the end of the week rather than the end of the summer.

We lay these issues out first because they are going to dominate trading and, in the final analysis they are all about politics. We could do reams of number crunching and prognostication but it would be meaningless without seeing how the politics get settled.

Italians have to decide if they will get serious about fixing their finances. Northern and central Europeans have to decide whether they suck it up and just pay allowance to Greece, and Ireland and whomever. They can afford to do it. The real question hinges on whether they are willing to do it. The debt numbers involved with those two countries are not large in relation to the EU economy but an actual decision needs to be made and stuck to.

It comes down to whether the populace in the better managed countries is willing to pay to keep the EU as presently constituted together. If not, they should cut loose the fiscal basket cases and let them devalue their way back to mediocrity and be done with it. Until we see how that question is decided no one really knows what the ultimate fallout is. Lest anyone have any illusions, a similar set of decisions faces Americans and there too the situation is completely politicized. With our rant du jour out of the way, we'll move on to the specific of the sectors we're dealing with.

The best reason to pick up juniors on the cheap during the summer months is that market issues are behind them. We still wouldn't say that the market should be comfortable about either western debt or eastern inflation fighting. However, the second reason for summertime bargain hunting is share prices so badly beaten down they are too cheap to ignore even if you are thinking medium term. Lately, quite a few traders seem to have come to that conclusion, though they are making the judgment about specific companies, not the sector as a whole.

That works if sellers finished offing before pulling out beach towels. The macroeconomic realities actually made this more likely as sellers don't want to wait for September when thinking about the mess outlined above. That does imply higher market risk this coming autumn, but looking at valuations and forward to eastern growth we think selective bargain hunting can begin. If the past week is any gauge, at least the algorithms that increasingly trade even small companies are willing to take the risk.

With Portugal joining Greece on the Euro bail out 2 (BOII) list we don't think the recent run in the copper price has a lot to do with recovery, per se. There are however unusually heavy snow in Chile and strikes in Indonesia that are slowing supply of mine product to smelters, and until Japan sorts out its power situation smelting capacity is below the glut level miners were enjoying before the tsunami took down generators.

Market listed stocks of the red metal in Shanghai moved up 10K to 90K tons in the past week while the light decline of LME listed stocks begun a month ago has become a trend line. Barring a large shift in the macro picture, the copper price has found a range above $4/pound pending news of how demand will be impacted by eastern inflation fighters.

China hasn't yet seen a peak number on the inflation front and we expect at least some further tightening there. Harmony (or 'peace' according to Premier Wen's recent comments in London, which may be more to the point) will demand costs for lower wage Chinese drive policy.

If it were simply a matter slowing domestic demand China's growth could decline measurably enough to dampen inflation with little impact on metal prices. However, in the context of global trade and western uncertainties some over compensating is more possible.

One area where governments' policy has maintained good order is, so far, on keeping trade liberal. So long as beggar thy neighbor doesn't rear its ugly head in trade rules any inflation-related slowing in China and other growth economies should be short lived. If trade was to become a political football the copper support from supply/demand balance plus a new role as a paper money hedge would slip. That would mean hunkering down, but traders would look for lower support levels rather than a cascade as they did in late '08-early 09.

We think gold has similarly found a trading base from the $1500 level, pending in this case whether the Euro or the Dollar gest more distain going forward. We'd be more comfortable if the prices gains were less about fear buying, but that has always been part of the gold market. The rerating of senior gold producers also appears to have reached a bottoming point. There has been some tearing of cloth over the fact that gold producers haven't kept up with gold for price gains. We think that seeming anomaly should now be done.

Barrick and Newmont are up about 350% from both 10 years ago and Credit Crunch bottoms, while growth oriented Goldcorp has gained more like 450% over those periods. The metal is up 600% over 10 years and 100% from Crunch lows. Comparing these to the copper space is uninspiring, but there were no copper bugs to support weak bottom lines during the bear market. Base metal companies were badly hit during the "commodities are dead" Tech Bubble, and typically recovered first when this secular bull started.

As we have said before weak gold equities is a case of 'be-careful-what-you-wish-for'. Gold companies are becoming a normal part of portfolio planning, which means they are also being priced to normal valuation levels—you can't anticipate higher gold prices after they have arrived. The Credit Crunch rebased everything, but it came before gold producers had finished rebalancing output to more realistic cost assumptions.

Yes, we did go through this not so long ago. However, we thought it worth repeating since the notion of retying national currencies to gold is getting a bigger listen these days in some quarters. We aren't convinced that is good for gold over the longer run. Gold, copper, oil and other commodities are already effectively part of the monetary system. Trying to fix a part of the system that isn't broken we can do without. The notion may be good for gold companies near term though and is worth keeping an eye on.

As far as more local major markets go, traders will have to depend on earnings season to keep interest up. Job numbers in the US have been awful. We can only hope that situation improves but no one will believe until it happens at this point.

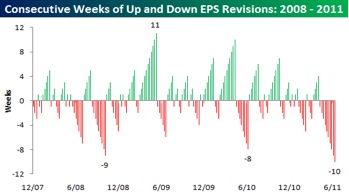

While the market hasn't priced in European calamity, it's set up for positive earnings surprises. The chart above from Bespoke Investment Group shows the weeks with either positive or negative earnings revisions by analysts going back three years. We're currently in the longest successive streak of negative earnings revisions in the whole period. With all the scary stuff out there analysts have been cutting earnings estimates constantly since the last earnings season. This is actually positive news. Its evidence that market sentiment is gloomy and substantially increases the odds that earnings surprises will be positive rather than negative. Odds are the earnings season we are entering will help support broader markets in the current range, assuming the world's political class doesn't screw things up yet again.

HRA has had some big wins in the iron ore and potash sector and we think it will continue to generate headlines and gains for a long time to come. One iron ore company in particular generated 650% gains for HRA subscribers and is being bought out—AND we now have another new highly prospective iron ore company that we will tell you about in this exclusive report that we're offering to you for FREE. This is a big, highly profitable market sector you'll want to learn more about today. Click here to receive our latest free report!

The HRA—Journal, HRA-Dispatch and HRA- Special Delivery are independent publications produced and distributed by Stockwork Consulting Ltd, which is committed to providing timely and factual analysis of junior mining, resource, and other venture capital companies. Companies are chosen on the basis of a speculative potential for significant upside gains resulting from asset-base expansion. These are generally high-risk securities, and opinions contained herein are time and market sensitive. No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer, solicitation or recommendation to buy or sell any securities mentioned. While we believe all sources of information to be factual and reliable we in no way represent or guarantee the accuracy thereof, nor of the statements made herein. We do not receive or request compensation in any form in order to feature companies in these publications. We may, or may not, own securities and/or options to acquire securities of the companies mentioned herein. This document is protected by the copyright laws of Canada and the U.S. and may not be reproduced in any form for other than for personal use without the prior written consent of the publisher. This document may be quoted, in context, provided proper credit is given.

©2010 Stockwork Consulting Ltd. All Rights Reserved.

Published by Stockwork Consulting Ltd.

Box 85909, Phoenix AZ , 85071 Toll Free 1-877-528-3958

[email protected] http://www.hraadvisory.com