Back in the late 1980s and '90s, Barker was known for his insightful and accurate views on the U.S. economy and financial markets via his K Wave Report newsletter. Today, he shares his views on the global financial market and economic outlook through his Long Wave Dynamics Letter.

Barker recently shares with me his thoughts on what he sees ahead for the United States and the emerging markets in terms of the inflation/deflation scenario. He also discussed the debt crisis, China, and the oil price outlook among other topics of interest. What follows is the transcript of that interview.

Q: David, where are we in the inflation/deflationary cycle? Do you still expect a heavy amount of deflation between now and the anticipated long-wave bottom in 2012?

Barker: Yes. I'm still in the deflationary camp. [The cycle] might be extended out later than 2012 based on quantitative easing and government stimulus expanding. I'm really looking for a bottom in the long wave in 2013 based on what has been done in the way of government stimulus since last year. If you look at $600 billion in quantitative easing, in the long run I don't think it does anything; but, in the short run, it juices the cycle. Actually, in the long run, the quantitative easing makes the deflation worse than it would normally be.

Q: How so?

Barker: There's a big difference in quantitative easing and printing money. With quantitative easing there's always an offsetting debt created. Ultimately, if you're a large tax-paying individual or corporation you know that, ultimately, someone has to pay that debt, and it will likely be you. So, it does have a dampening effect on the economy.

There's another aspect to QE that I don't think Bernanke appreciates and that he's feeding deflation by keeping operators and manufacturers in businesses that probably should be taken out of business that would provide pricing power for manufacturers of any goods and services. But by keeping the weaker operators in business, it ultimately has a deflationary effect.

Q: Lately we've been hearing the financial press repeat the mantra "higher taxes are needed" to get the U.S. out of its fiscal mess. Would raising taxes in a recession be bad economic policy in your view?

Barker: Raising taxes in the long wave is an absolute disaster. Maybe if this was going on in the early 1990s you could make that case. We've tried spending and taxing and it's not working. The only way to get out of this is a lower corporate tax rate. I'm in favor of a fair tax but I realize that's unlikely to occur. The next best thing would be radically reducing the corporate tax rate to stimulate job growth and business investment. You're simply not going to get it without tax rate reduction.

The irony here is that the media focuses on people paying their faire share but my argument for a lower corporate tax rate is not because I want to be kind to the corporations. I want to be kind to the employees. The only thing that a higher corporate tax gives you is higher prices and lower wages. At some point, we're actually going to have a politician that can articulate that. It's not that complicated to figure out that if you raise taxes on corporations they pay their employees less and they charge more for their products.

Q: In your latest Long Wave Dynamics Letter you wrote, "There comes a point with debt where it reaches diminishing returns, and the developed world reached that point some time ago." Would this explain why the Fed's frantic efforts at providing liquidity have failed to revitalize the economy?

Barker: Correct. We're overproducing everything and we're doing it with extensive debt. The whole point of QE [quantitative easing] was ostensibly to create more borrowing and business activity. We're overproducing everything we need right now from services to manufacturing. What we need is whole new industries, which come with long wave innovation and lower taxes. But the stimulus simply isn't working and the old phrase "pushing on a string" applies here. The hedge funds want to borrow that money to buy commodities. The banks are taking that money that's created and they're buying Treasuries. They're not creating economic activity and true sustainable growth.

I think Bernanke believes in what he's trying to do but it just simply is not working. He doesn't understanding what's happening. He was testifying before Congress recently and basically said, "I don't understand what's going on with the economy." What he doesn't understand is long wave theory. He doesn't understand that he's pushing on a string and that what we need is to get rid of debt and we need some austerity. The notion that we can get through this economic problem without some pain is foolish; we need a painful adjustment to get us on the other side of this.

That being said, the positive aspect to this is the emerging markets. When you look at the whole inflation/deflation argument, you can see that the developed world is essentially deflation. The emerging markets with the growth of the middle class and the demand for goods and services there is an offsetting inflationary pressure on the global system.

Q: You also recently discussed the possibility of a "soft landing" of the current long wave. In your view, what are the odds for this and what is required, politically speaking, to engineer a soft landing?

Barker: If you give me a 15% corporate tax rate and you actually see some real spending, I think you could actually engineer a soft long wave [bottom]. It would be painful for certain entities. The problem we have is the large multinational corporations have favorable tax rates because of their political clout. But the small entities are paying much higher tax rates. For instance, I'm a large investor in a small entity and I pay a 40% tax rate whereas the big guys aren't paying that. The small guys can't afford to pay to get the exemptions in the tax code. Basically, it's a criminal situation.

I would support Obama if he would reduce the corporate tax rate to 15% I'd say abolish all loopholes. Why should a little company that's struggling and that has 10, 50 or 100 employees pay a 40% tax rate while the guys are paying nothing? So bring the corporate tax rate down and abolish all loopholes and I think you'd create a massive inflow of trillions of dollars into the United States. And you'd trigger all sorts of investment and ideas and creativity in the system and you would create a boom. And you would end up with a lot more tax revenues.

Q: Have we seen the end of the credit crisis or will the process of debt hemorrhaging and deleveraging continue? In other words, was the 2008 crisis a proverbial "shot across the bow," or was it a one-time situation?

Barker: It was a shot across the bow. I think there's a bigger credit crisis coming. Most of your big U.S. banks are insolvent. We don't have a liquidity problem—we have a solvency problem. The Fed can liquify the system but they cannot create solvency.

Q: Can you explicate on that?

Barker: By dropping interest rates to zero, it's a massive hidden tax on prudent savers in this country that's going to the big banks. The bailout is a lot bigger than people realize. Grandmother Barker is getting 0% on her savings. The big banks are paying her 0% and they're loaning to the government at a 3% 10-year [bond] or with a blended rate, and then they're pocketing the difference.

There's a massive bailout going on that people aren't talking about and it's destroying demand in the economy. Interest rates would be low anyway, they just wouldn't be quite as low and you wouldn't have the spread that the big banks are picking up. And that's how the Fed is liquefying the stem. They're creating the income there plus the income for the big banks. Their whole objective is liquidity, not solvency. They're hoping the liquidity will solve the solvency problem but as home prices and commercial real estate prices tick lower the solvency problem is getting bigger. So at some point the solvency problem will overtake the liquidity that the Fed is pumping into the system, and that's when the next leg of the crisis and deflation hits.

Q: You've stated that the only way out of the global financial mess is austerity. Could you expand on that statement?

Barker: We've all spent beyond our means. We have to pull in our horns here and we've got to focus on capital formation, savings and investment. You can't solve a debt problem with more debt. It's ludicrous.

Q: What are the odds of a third quantitative easing (QE3) and if it's coming, when do you see it coming?

Barker: I hope it's not coming. If the credit crisis takes, another big leg down and we see deflation in the system I have to believe that Bernanke will be permitted to do additional quantitative easing. I don't think it's politically viable that QE3 can stop the deflation that's coming, though. The amount of [quantitative easing] that would be required to stop the next leg of the credit crisis would create some political issues for the Fed.

Q: Bill Gross of PIMCO recently made headlines for his bearish outlook on U.S. government bonds. Does your reading of the long wave tell you that Mr. Gross is mistaken in shorting long-term bonds? Also, what is the general outlook for bonds in view of where we are in the long wave?

Barker: Mr. Gross is a lot smarter than I am but he obviously missed this call; bonds are still rallying and interest rates are falling. I think this is the long wave weakness out there. He's going to be right longer term but I think between now and 2013 the long bond is going to rally. I think the U.S. is going to figure out its debt issues and we're going to address them. That's part of why I believe the long bond is going to continue to rally. In the developed world it's a debt problem and a deflation problem. That means your German, your Swiss and your U.S. bonds are going to rally in price and interest rates are going to come down even lower because there's going to be even less demand in the system as the credit crisis accelerates.

Q: Where do you see the next trouble spot occurring in terms of the next global crisis? Will it be here or abroad?

Baker: You could conceivably fix up the debt problem for another year and just kick the can down the road. China has to be at the top of the list in terms of the big problems that can happen. If China's economy gets weaker as this long wave bottoms out into 2013, and I think it will, then that could be the next crisis. Or, it could be a big U.S. bank that gets in trouble. I wouldn't name any of them specifically but there's a few of them where you have to wonder if the feds can address the bank solvency issue.

Q: What in particular do you see as the major stumbling blocks for China in the next one to two years? Will it suffer a major recession or depression before the next long-wave spring season begins?

Barker: It's been doing far more stimulus than the U.S. has. You think we've been doing QE—China has done even more. It's not specifically QE but rather aggressive fiscal and monetary policies. China has a significant housing bubble on its hands just as we did in 2006 that could potentially do some serious damage to the Chinese economy. Plus, its economy is still built on exports to the rest of the world; and as the U.S. consumer continues to pull in [spending], it will affect the Chinese economy.

Longer term, I've very bullish on the emerging markets and about the size and scale of the middle class coming into the political system. I think it's going to be phenomenal. It's just that the developed world's debt crisis we have to get over between here and there.

Q: In your view, does China need to shake off its Communist government before achieving true national and international greatness?

Barker: Absolutely. It's going to take a while but the country needs to shift toward a more Republican form of government. Remember, the U.S. wasn't formed as a democracy but as a republic. So, hopefully, China goes the direction of a republic as opposed to a democracy. It's ridiculous when you think about it. It's got a communist government running a central bank. People here complain about the Fed, but [China] is juicing its financial system like crazy. It put out all these mandates about growth and it doesn't care how you get there. The China story is real, don't get me wrong; and China's economic boom is real. And sure, the communist model that it's created could still be productive—it's really more a type of fascism or dictatorial system. Yet it has to convert to a freer society and I think it will, but I don't think we need to push it. That's its internal issue. And I think China will slowly convert to a non-communist system.

Q: Let's talk about the U.S. government's recent oil release from the Strategic Petroleum Reserve. Was this another attempt to juice the economy, or do you think there was another motive for this?

Barker: My reading is that there's panic going on in high places. It's asking, "Why is the economy still weak?" And of course, it's seeing that high oil prices are affecting the American consumer, so it had to get oil prices down. So, it was definitely an attempt to boost the economy. I don't think anything that happens in Washington is political, per se. I think the government's really just trying to get the economy going. It's a sign of panic because, at this stage, it thought it would see growth and improvement. So, it's scrambling to see what it can do to generate growth.

Trying to drop oil prices is obviously an attempt at generating growth but it's kind of silly because we've got a strategic petroleum reserve for a reason, and that oil has to be added back in there. So, it's just taking from the future. It's going to have to purchase from the future to put it back in there. That's just an attempt to stimulate the economy.

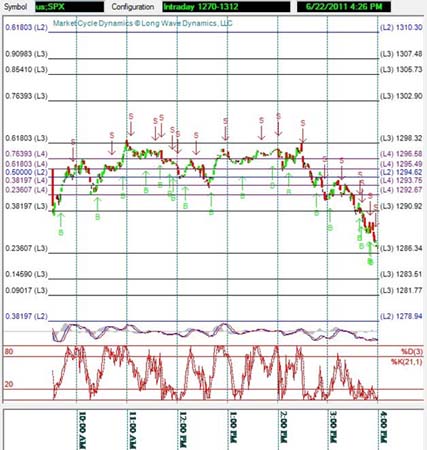

Q: I know you're a big believer in Fibonacci analysis as applied to not only cycle forecasting but also to market trading. You recently created a new software product called Market Cycle Dynamics (MCD), which you say is unique to any other trading system due to its Fibonacci applications. What can you tell us about it?

Barker: My whole approach to technical analysis is price, time and sentiment. And I believe that Fibonacci is the pricing mechanism of markets. It's simply a tool that allows you to more quickly uncover where a turn is happening in a market either on a short- or long-term basis. There are a number of innovative things about the software but one of the main things is the Fibonacci drill down grid, where you can get down to a daily basis and see what's happening in the market. "Quant X-ray" is what I call it. You've got the quantitative analysts out there writing the code for the computer programs that their using for the high frequency trading. And invariably they're using Fibonacci ratios in their algorithms.

For the first time, I think Market Cycle Dynamics allows you to drill down and see where those turns are being triggered. And that's relevant whether you're a long-term investor or a short-term trader to see where those programs are going to kick in and either trigger selling or trigger buying. MCD acts as an x-ray on the market to see where those grid structures are. It will startle people to see a level three or -four Fibonacci grid on an intraday basis where you see the market ticking and reversing on these grids.

So, you use price, which is Fibonacci, and then you use time or the cycle approach. You use sentiment and for that; I use stochastics. And you just use this to find when you a market turn could occur. The MCD software, which runs with MetaStock, combines all three of these elements.

Q: For the benefit of those unfamiliar with Fibonacci, could you give us a brief overview of how it's important to understanding market turning points?

Barker: I believe that Fibonacci is the pricing mechanism of markets. When you look at a decent presentation of Fibonacci grids, you realize that where the market turns, big turns, are typically at Fibonacci key points in the market. Italian Mathematician Fibonacci discovered the Fibonacci [numerical] sequence and Fibonacci ratios are a function of those sequences. What they've discovered is that Fibonacci appears in all natural forms of growth, whether it's pinecones, seashells, the ocean or the galaxies. We find that Fibonacci is in all natural systems of growth and decay, and it governs growth and decay in natural systems. I believe markets are a natural system of growth and decay; and when you use Fibonacci correctly, it picks up the market's turns.

Note: More information on the Market Cycle Dynamics software is available here

Q: What's your take on the recent stock market rally?

Barker: It looks like we got the turn of an important Wall Cycle. It's a phenomenal rally, which makes you wonder what's going on out there. But long term it doesn't change anything. Short term, I think it's a function of all the liquidity in the system.

Q: How long can the feds keep the economy at its current level before deflation makes its presence known again?

Barker: I think we're in a window where the deflationary pressures are overwhelming. I know everyone is concerned about inflation but if you look at it, Bernanke is actually correct to be scared of deflation. He knows what he's talking about and the deflationary pressures are just phenomenal. It can overwhelm any efforts to kick the debt time down the road.

With my whole cycle approach the most important cycle is the business cycle, which I think ideally runs 42 months short or long. The effect of this quantitative easing and lower interest rates just makes the cycles run a little bit longer—but it actually is leading us toward chaos. Markets are complex systems; central bank intervention messes with that system and fiscal policy messes with that system. They can make the cycles run longer, but they can't stop the cycles. When they do make it run longer, they have a tendency to push the system toward chaos, not toward order.

You have bifurcation in cycles sometimes. I think the 20022009 period was a doubling bifurcation within in a cycle. Anyone who understands complex systems understands that the doubling effect in a system leads to chaos, whereas halving bifurcation leads to order. Basically, I believe that all the intervention is creating a system that leans toward chaos. But it will be resolved and, eventually, we will move into the next advance. I think we're on the cusp of a major global boom; we just have to get past the disasters related to the debt bubble. I don't think the political will is there to sufficiently juice the system to get past the deflation. So, I think we're going to have resolution to the crisis between 2012 and 2013 wherein we do have a deflationary crack and a real debt-bust crisis. But then, we're able to move on to the other side.

Clif Droke is the editor of the three times weekly Momentum Strategies Report newsletter, published since 1997, which covers U.S. equity markets and various stock sectors, natural resources, money-supply and bank-credit trends, the dollar and the U.S. economy. The forecasts are made using a unique proprietary blend of analytical methods involving cycles, internal momentum and moving-average systems, as well as investor sentiment. He is also the author of numerous books, including The Stock Market Cycles. For more information visit www.clifdroke.com.