"ARE YOU available for an interview this afternoon? I'd like to discuss the possibility that we're in a gold bubble!" So asked a journalist's email we got here at BullionVault. . .back on 30th January 2009. Such bubble talk has only grown louder since then.

Yet gold has risen a further 56%. Which over two and more years is hardly the stuff of bubbles, however you define them.

Gold investing used to be seen as a contrarian move, of coursea rejection of the happy-clappy bullishness pervading the late-20th century's credit-fueled stupidities. So, what about mass participationthat frenzy of Joe Public buying as the mass media urges him on?

Well, "My esteemed colleague, the astrologer Christine Skinner, says in her latest financial newsletter that over the next few months, 'precious metals should hold their value and, indeed, increase,'" wrote the UK's Jonathan Cainer this week in mass-market tabloid The Daily Mail.

Oh lordy! Gold investing is being tipped in tabloid horoscopes. . .Sell!

But what's this? "Generally," Cainer goes on, "precious metals rise when international insecurities rise. I, too, foresee a bumpy few months on the world markets. . .but the further into the future I gaze, the more I like the look of the global economy. For Japan in particular, the financial outlook is surprisingly rosy."

So here again, gold's bubble finds its pin all too soon. Christeen Skinnersource of the gold tip"has studied space and time for over 40 years," according to her website, but doesn't currently have a million-strong following. Unlike Jonathan Cainer, who takes instead what you'd have to call the contrarian line, if only gold investing really were all the rage today, which it's not.

1. It's the Wrong Shape

Compared with undeniable bubbles, gold's recent climb just isn't steep enough. Gold prices rose 85% for UK investors in the last 3 years, but US stocks rose 160% in that length of time in the 1920s, and Germany's Neuer Markt rose over 1600% starting in 1997. The South Sea Bubble in 1720 rose ninefold in five months! What makes gold remarkable today is the longevity, not speed, of its bull marketnow delivering positive, inflation-beating returns to savers pretty much everywhere worldwide each year since 2000.

2. Investment "Mania" Still Missing

The financial pages might be packed with gold comment, but actual participation by both professional and private investors remains low. In the early 1980s, private-bank clients were expected to hold 3% of their wealth in gold, many times the 0.5% allocation seen in the finance industry today. Even in the bullion market itself, three-quarters of the +500 analysts and traders attending last autumn's LBMA conference in Berlin said they held as little as nothing ("Between 0% and 10%") of their savings in precious metals. Saturation is a long way off.

3. . . .As Is True "Bubble" Psychology A speculative bubble, by definition, needs the mass of investors and analysts to ignore its faults until it's much too late. As late as summer 2007, for instance, and with US home prices already falling fast, housing was called a "serious national bubble" by only 29% of professional business economists, up from just 14% two years earlier. In Jan. 2011, in contrast, over half the 1,000 Bloomberg terminal users answering the newswire's quarterly survey called gold a bubble. Just this week, Barclays Capital's latest institutional survey found no onenot one!who thought gold would be the best performing commodity in 2011. With prices hitting new all-time highs vs. the Dollar right alongside, does that sound like bubble behavior to you?

4. Gold's Far from Overvalued

All the gold outside central-bank vaults today (jewelry plus bars and gold coins) is now priced around £3.7 trillionbarely 3% of the world's total private wealth and far below the 15-30% estimated for the 1930s and early 1980s, the last two global financial crises. It's only just climbed back to one-fifth of the value of G7 government debt, a level last seen in 1990 and well below the near-parity of 1980. And on a risk-adjusted basis, calculated as an actuary would price insurance, fair value for gold could now be nearer $3800 per ounce than the $1440 being asked in the market. That's because the market continues to discount to zero the risk of a severe, even hyperinflation, such as the rich West hasn't seen since WWIIwhich could no doubt prove the correct view, if only it weren't so complacent.

5. Money-Crisis Insurance Still Needed

It's always hard to accuse gold buyers of "over-optimism" (Charles Kindleberger's definition of bubble mentality), but this market will only switch to "irrational exuberance" (Robert Shiller's phrase) when its key driverloose monetary policyceases to be true. That's what happened as interest rates began rising sharply at the start at the end of the 1970s. In the early '80s, cash in the bank started to pay double-digit returns over and above inflation, so inflation defence just wasn't needed. Whereas today, in contrast, real interest rates in the UK are worse than at any time since 1978, with our record peace-time deficitsplus the loose money consensus which continues to dominate both monetary and fiscal policy capping any hope savers might have of earning a decent yield on their cash.

To recap, nothing has changed fundamentally. Ultra-loose monetary policy is chipping away at the value of official cash, only it's now locked in by record peace-time deficits, which have hamstrung central bankers' ability to respond to rising prices. As an aside, emerging-market demand continues to grow, but mass participation in the rich West is a very long way off.

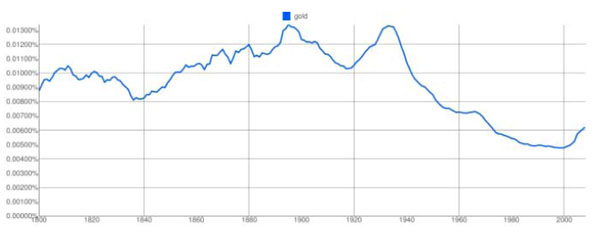

Or as GoogleLab's Ngram widget puts itsearching books published in English since 1800the word "gold" is only just making a comeback. Gold investing is by no means sure to defend or grow your savings; it certainly remains far from a bubble.

Adrian Ash

BullionVault

Gold price chart, no delay | Buy gold online at live prices

Formerly City correspondent for The Daily Reckoning in London and head of editorial at the UK's leading financial advisory for private investors, Adrian Ash is the editor of Gold News and head of research at BullionVaultwinner of the Queen's Award for Enterprise Innovation, 2009 and now backed by the World Gold Council market-development and research bodywhere you can buy gold today vaulted in Zurich on $3 spreads and 0.8% dealing fees.

(c) BullionVault 2011

Please Note: This article is to inform your thinking, not lead it. Only you can decide the best place for your money, and any decision you make will put your money at risk. Information or data included here may have already been overtaken by eventsand must be verified elsewhereshould you choose to act on it.