Notes to tables:

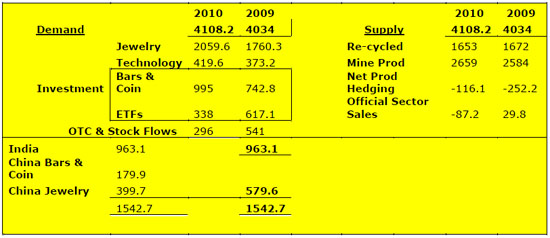

- China mined 340 tons and imported over 300 tons according to Chinese officials.

- The difference between these figures and the figures of the WGC imply further imports of 60+ tons.

- Were these for the central bank, the PBOC?

- OTC and Stock FlowsAlthough partly a statistical residue of demand in the OTC market, including an occasional additional contribution from changes to fabrication inventories.

- ETF total held 2,175 tons in 2010.

- The IMF sold 403 tons in 2010, which added to the purchases in the table, which shows total purchases by central banks at 490.5 tons

Clarifications

Central Bank Buying

We need to clarify certain points above if we are to understand the effect that these numbers will have on the numbers for 2011. The net official sales were in fact 87.2 tons bought by central banks in the open market. To that figure, you must add the 403.3 tons the IMF sold to give you the total amount central banks bought in 2010. In 2011 with such additional supplies no longer available in large chunks, we do not expect to see visible purchases by central banks in the market except for Russia, who is still buying (they bought 3.4 tons in January in line with the pattern they showed in 2010. They have stated they will continue buying upwards of 100 tons per annum. We are informed that the bulk of this is bought from local producers. So just how much gold central banks will buy in the open market is difficult to project. All we can say is that taking the amount over the IMF total of 403.3 tons plus the amount the IMF sold in the open market (181.3 tons plus 87.2 tons) we have a figure of the amount central banks bought in the open market in 2010 of 268.5 tons, told us that, that was their appetite for gold last year. We expect that appetite to grow in 2011. This amount of even 268 tons would now have to come from the open market in London.

China

We believe China is following the same path (though using an intermediary agency) to keep such purchases out of sight. Once every five years these are reported, when that agency hands over the gold it has bought in the previous five years. The last reported purchase over five years was an average of 91 tons per annum. Of course, the purchases may have been different over that period and may have matched growing local production. We do not have the information available to know what amount the PBOC is buying locally or whether they are buying direct off the international market and will only know that in two years time, when they make their next public statement. We know that China produced 340 tons last year and imported over 300 tons. The indications are that the People's Bank of China is buying in the international market too.

This is important because if the 640 tons for sale in China in 2010 was available to the local retail trade, then we expect this figure to rise (guided by the figures for the first two months of this year ahead of the Chinese New Year) by 70%. Hence, China could take in 1,088 tons for the private sector in 2011 if the demand remains at these levels. As you can see above, the numbers from the WGC show a total of 579.6 tons used in the private market in China in 2011. An increase of 70% over that figure gives a total of 985 tons projected as private demand from China. This reinforces our belief that the PBOC is buying in the international market as well. Such an increase over 2010 is confirmed by the retail demand for gold in China since the Chinese New Year.

Demand Factors in 2011

- With double-digit growth expected to continue for the next decade alongside a flat to growing developed world overall, jewelry and technology sector demand will either remain at current levels or rise.

- We must emphasize that the market has accepted these higher prices for gold and will continue to realize that gold is a precious metal. It remains the metal of choice for jewelry irrespective of the price.

- Demand for gold bars and coins will continue at very high levels in 2011 as there are no efforts visible that will reinforce or reform the global monetary system. Food and energy inflation is expected to continue at high levels, irrespective of efforts by central banks to tackle inflation. This will continue to make gold attractive.

- We do expect to see the shares of gold ETFs to be sold or redeemed as investors move their gold to another country or keep it at home. There remains a strong belief among the institutions owning gold that confiscation by government remains a strong possibility (but not for the same reasons as in 1933). Holding gold in banks in ones own country simple makes the process easier.

Newly mined gold production is expected to rise by just over 100 tons in 2011, but there is not the flexibility or sufficiently large deposits to increase that figure. Many mining companies are struggling to replace mined resources as it is.

We do expect to see a fall to almost zero of just over 100 tons in producer dehedging in 2011. This will release that gold for other users.

Official sector sales will almost disappear being replaced by official purchases in 2011.

Recycled gold should be re-named gold sold by current holders for this is what it is. In the developed world, profit seekers sell when they feel the price has peaked short, medium of long-term. In the emerging world, in particular India, long-term holders sell gold for personal situational reasons or because the gold price has risen too far or too fast. They then sell with the intention of buying that gold back once the price has made a new floor.

Ramifications for 2011 and the View from the Developed World

Subscribe at Gold Forecaster (gold); Silver Forecaster (silver).

Legal Notice/Disclaimer: This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Gold Forecaster - Global Watch/Julian D. W. Phillips/Peter Spina, have based this document on information obtained from sources it believes to be reliable but which it has not independently verified; Gold Forecaster - Global Watch/Julian D. W. Phillips/Peter Spina make no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Gold Forecaster - Global Watch/Julian D. W. Phillips/Peter Spina only and are subject to change without notice. Gold Forecaster - Global Watch/Julian D. W. Phillips/Peter Spina assume no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, we assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information, provided within this Report.