One analyst who doesn't share this newfound optimism is far from the conventional Wall Street type. He correctly predicted the 2008 credit crash and also turned bullish in March 2009 following the crisis low. He has made a career of going against the consensus and he's once again staking his reputation against the Wall Street establishment. He believes that far from being the dawn of a bullish economy, 2011 will witness the end of the post-credit crisis economic recovery. He also believes 2011 will witness a "crisis high" in the stock market and most likely a turning point within the context of the long-term cycles. That analyst is none other than Samuel "Bud" Kress of the SineScope advisory (SJK Capital, 15 Phoenix Ave., Morristown, NJ 07960). His 10th and latest Special Edition is aptly titled, "Crisis High 2011-2014."

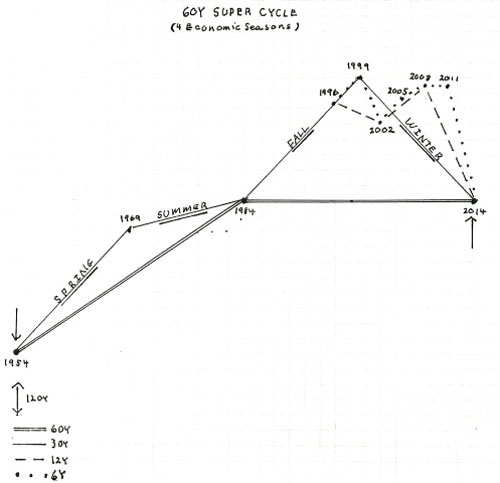

In the more than 10 years that Kress has been writing his Special Editions, we've seen the long-term sequence of yearly cycles that bear his name unfold according to schedule. We saw the Kress 12-year cycle bottom hard in 2002, producing a major bear market low. We saw the 10-year cycle bottom in 2004, producing a mini-cyclical bear market and another leg of the bull market following its bottom. We saw the 6-year cycle descend into 2008, adding downside impetus to the credit crisis and producing another cyclical bull market in 2009. This year's notable cycle event is the peaking of the 6-year cycle, which takes on special significance because the 6-year cycle is the last of the major yearly cycles to be in the ascending phase. Once the 6-year peaks later this year, each one of the Kress yearly cycles (with the exception of the 4-year) will be in the final "hard down" phase until late 2014.

Until the 6-year cycle peaks, the next few months are likely to witness the transfer of wealth from the insiders to the outsiders. Private equity groups, for instance, will be looking to offload debt via the IPO market. Institutional traders who bought stocks around the lows of the last bear market in late 2008/early 2009 will be looking to sell to the public, which is only just beginning to return to the equities market after spending the last two years in low-yielding bond funds. Such tactics are always employed in critical years when the major yearly cycles are peaking and 2011 should prove to be no exception.

Kress sees 2011 as being the last year of the financial recovery that began in March 2009. He uses the metaphor of a storm to describe the 2008 credit crash and believes the financial storm of that year arrived beginning with the "leading edge," which gave way in 2009 to the benign "eye of the storm." As with a hurricane, the storm's "eye" isn't the end of the storm, rather it's merely a temporary respite as the storm's "trailing edge" follows at some point. Kress believes the "trailing edge" of the financial storm will begin by next year and he says it could be a tsunami.

In section two of the latest Special Edition, Kress provides an in-depth look at the major yearly cycles that comprise the 120-year Grand Super Cycle scheduled to bottom in 2014. When analyzing the impact of the yearly cycles it's important to keep in mind that the final 12% of the duration of any cycle is the "hard down" phase. The 120-year cycle's hard down phase began 14 years prior from 2014, which was 2000. This, says Kress, "was the peak of the nation's economic expansion, the beginning of economic winter and the terminal high."

The 120-year cycle includes two 60-year cycles, which also answers to the economic long wave (also known as the Kondratieff Wave, or K Wave). The K Wave tracks the four economic phases of the credit cycle from boom to bust. Applying the 12% "hard down" rule of thumb, seven and a quarter years retroactive from the scheduled 2014 Grand Super Cycle bottom is mid-2007. "This period began the 'hard down' phase of economic winter prior to the 'credit crash' and the beginning of deflation," writes Kress. "Of greater significance," he adds, "the current 60-year [cycle] is the fourth, which completes the series that began with the first 120-year, which transformed America into an independent country as we know it today." The inference here is that when the current 120-year/60-year cycles bottom in 2014, the United States will experience a revolutionary transformation, of which Kress has more to say elsewhere in the report.

The 120-year cycle has also aptly been termed the "revolutionary cycle," as its bottom is always accompanied by a revolution of sociopolitical and economic import. Concerning the upcoming 2014 revolutionary cycle low, of which the recent Middle East uprisings are merely a portent, Kress asks: "Could wealth creation become a rarity; could the American Dream become a fantasy; could we become a socialistic economy; could a WWII equivalent develop; could our political structure be reformed; could it be the end of the Federal Reserve; could the USA's premier world power become subordinated to second rate???"

In regard to the 6-year cycle, Kress points out that the present 6-year cycle began in late- 2008 and is scheduled to peak in late September/early October this year. He says the peaking of the 6-year cycle should begin the second half of the credit cycle, and that "depression could accelerate the decline of the final three years of all the higher cycles comprising the 120-year Grand Super Cycle in later 2014."

Kress observes, "With all of SineScope's cycles being in the down phase for the first time since 1890, the potential for the worst of anything to occur exists. This elicits some very disarming implications for the USA and our lifestyles for the next three years."

The latest Special Edition by Kress also discusses the outlook for consumer spending in light of the long-term cycles. "With the consumer representing approximately 70% of our economy," he writes, "growth is dependent on consumer spending, which is a function of credit expansion and increased employment." The credit crisis, however, elicited a sea change of consumer attitude toward debt. As Kress observed, "Consumers not only ceased incurring additional debt, they also began reducing it, which is referred to as 'deleveraging' but in reality is liquidation of capital resulting in reduction of consumer spending."

Kress says that recent earnings gains have been mainly from cost savings realized from deleveraging and employee downsizing, with revenue gains being only a token rate reflection of low consumer spending. He believes that corporate cost savings have nearly run their course. "If [consumer] spending continues to decline," he writes, "corporations might have to close plants which would complete liquidation of the three assets comprising our economyhuman, capital, physicaland the USA [will] effectively be in liquidation." He adds that if oil and food prices continue to rise it will further curtail consumer spending, and that an additional "red flag" would be an increase in the unemployment rate.

The most provocative aspect of Kress' latest Special Edition is the discussion of how low the S&P 500 could decline by the time the "revolutionary low" is reached in 2014. Prior to addressing this Kress writes, "Hundreds of equity mutual funds manage trillions of dollars of equities with positions in increments of 100,000 shares. What happens if and when these managers decide to selland to whom?" Accordingly, Kress believes that capital preservation is the watchword for the years 20122014 as opposed to capital gains.

Concerning the outlook for gold, Kress points out that two opportunities exist to buy gold during the 60-year Super Cycle. The first is during the hyperinflationary period of the cycle, in which gold is the ultimate hedge against the ravages of inflation. This period occurred during the inflationary period of 19661981 when the gold price increased approximately 23x measured in price per ounce. Gold then entered a bear market until 2000. "If gold increases the same amount during the same 15-year period of economic contraction from 20002014," writes Kress, "gold would achieve over $5,000 per ounce."

Cycles

Over the years I've been asked by many readers what I consider to be the best books on stock market cycles that I can recommend. While there are many excellent works out there on the subject of technical and fundamental analysis, chart reading, etc., precious few have addressed the subject of market cycles. Of the relatively few books on cycles that are available, most don't even merit mentioning. I've read only one book in the genre that I can recommendThe K Wave by David Knox Barkerbut even that one doesn't deal directly with stock market cycles but rather with the economic long wave. I'm pleased to announce, however, that after nearly 10 years of research and one year of writing, I've completed a book on the subject that I believe will meet the critical demands of most cycle students. Click The Stock Market Cycles to purchase the book.

Clif Droke is the editor of the three times weekly Momentum Strategies Report newsletter, published since 1997, which covers U.S. equity markets and various stock sectors, natural resources, money supply and bank credit trends, the dollar and the U.S. economy. The forecasts are made using a unique proprietary blend of analytical methods involving cycles, internal momentum and moving average systems, as well as investor sentiment. He is also the author of numerous books, including most recently The Stock Market Cycles. For more information, visit www.clifdroke.com.