Inflation is driven by low interest rates and lax credit conditions. Severe inflation is driven by the inability to finance or grow out of debt.

Commodity bull markets are primarily driven by monetary factors. Secondarily, a lack of production eventually leads to much higher prices. Commodity industries are cyclical in the long term. They go from periods of oversupply to f underproduction, which then creates a lack of supply and a need for higher prices to stimulate new production. The big moves in individual commodities or sectors are driven not from demand but from a lack of supply. There are numerous examples.

Let's start with the rare earth elements (REEs). China accounts for 95% of the world's supply and it's projected that within a few years China won't be able to supply its own demand, hence the export quota reductions, and may form its own OPEC-like group to control the REE market. Sure, their demand is strong but the real problem is that there's no production outside of China. Molycorp owns the only rare earths mine in the U.S. (Mountain Pass in California) and it hasn't been in production for years.

Does this industry have too much demand or too little production? Again, it's a rhetorical question.

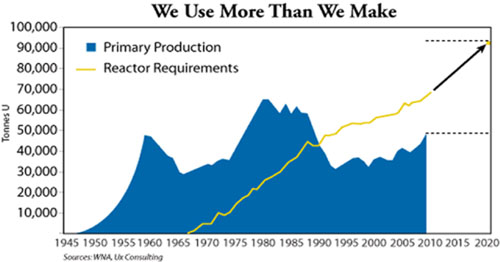

Consider uranium. Most know the story. It's an industry that has lived off of stockpiles for a long time. That is going to end in 2013 with the end of the Russia/HEU agreement, so more production will be desperately needed in the coming years. Look at the picture below. Reactor requirements (demand) has risen consistently for decades. Obviously, it's the supply/production picture that moves the market.

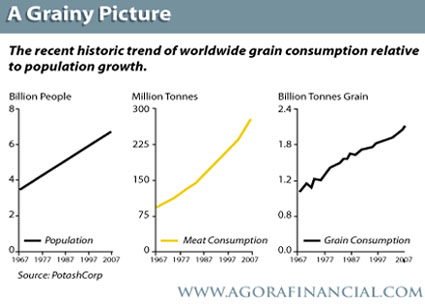

Precious metals are actually the outlier; investment demand moves the market. Some analysts like to mention global growth and more jewelry buying but that has little impact on major bull and bear cycles. The most absurd theory is that food prices are rising due to rising demand. Did millions more Chinese people suddenly begin eating now relative to 510 years ago? Take a look at the following graph from Agora Financial.

Growth in population, meat consumption and grain consumption is reliably steady. Food prices don't rise because there is more demand. That is asinine. Food prices rise primarily because of supply and inventory factors along with monetary factors.

Monetary inflation creates artificial demand, which triggers higher prices. Our monetary inflation is exported to China. China takes the incoming U.S. dollars and prints yuan to maintain the currency peg. That causes inflation. China then spends money domestically and abroad, triggering inflation in other nations. Furthermore, inflation raises the cost of production and bringing that supply to the market.

In the big picture, inflation is a major driving force for the commodity sector as a whole. In regards to specific commodities, the real commodities gurus like Jim Rogers and Rick Rule always look first at supply factors because they know that is the number one driving force behind the biggest runs. Presently, the uranium market is in a very large deficit and a surge in production is required over the next 510 years. Growing demand is just icing on the cake.

Jordan Roy-Byrne, CMT

[email protected]

Subscription Service

Monetary Inflation and Supply Concerns Drive Commodities More than Demand