WHAT WOULD the world look like if, as a handful of economists, investors and politicians hope, gold really was money again?

In a word, cheapish. Cheaper, at least, than much of it was a decade ago.

Long used (together with silver) as a means of exchange and unit of account, gold had already lost those functions by the time it ceased backing the world's currency system in 1971. But gold retains the third function of moneyas a store of valuenow beating, now lagging the unbacked fiat money (i.e., created at will), which replaced it.

Since then, gold's value has also varied more widely against other competing stores of wealth, as well as cash, amplifying the swings in its relative worth against equities, real estate, commodities and government bonds.

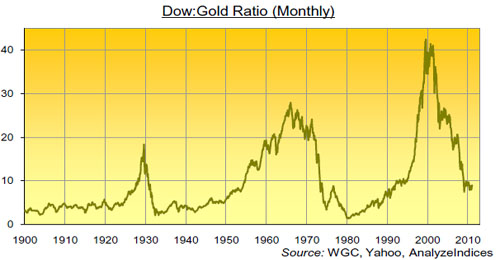

Perhaps you've seen the above chart before, for instance. Simply dividing the Dow Jones Industrial Average by the dollar-price of gold per ounce, the Dow:Gold ratio might sound an arbitrary yardstick. But it tracks the relative worth of U.S. equities against an increasingly popular, if still minority store of wealth, gold bullion. Dividends are excluded, leaving just the market pricerather than income or earnings potentialof business assets in the world's largest economy, measured by a lump of dumb metal.

Why? Unlike corporate equity, gold doesn't do much. It can't even rust, much less grow (or shrink) its return on capital employed. And from the recent low (7.2 ounces per Dow unit, hit in Feb.2009), U.S. stocks have gained 20% vs. gold. (Priced in nominal dollars, they've risen 73% in the last two years.) The historic low stands beneath 2 oz. gold, the all-time high above 40. Today, the Dow:Gold ratio sits just shy of 9a little beneath its 12-decade average of 10.

Note those two lowsor rather, peaks for goldhit in the mid-1930s and early 1980s because they show up elsewhere, as well.

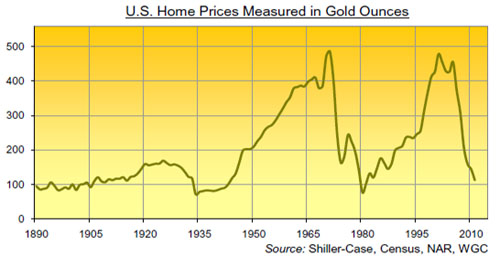

The average U.S. homea term so broad, it's quite possibly worthless beyond the very broadest historical sweephas averaged 202 oz. gold over the last 120 years, at least on the data we've constructed from a collection of sources to cover more than a century's worth of different housing, styles, sizes, locations and amenities.

Let's put the methodological doubts to one side, though. Currently priced around 112 oz., U.S. housing hasn't been this cheap in three decadesdropping more than 75% from the 2001 high (478 oz.; the 1971 peak was 485 oz.). Returning to the very lowest prices on BullionVault's series would see residential property lose another third. It hit 77 oz. in 1980, just above the 1934 low of 71 oz. Whatever the national U.S. housing stock gained in utility or comfort over that time (in short, non-rusting gold) priced it just as lowly amid first a deflationary, and then an inflationary depression.

Commodities are a separate matter because they have never been cheaper in terms of goldslumping by more than 70% since 2001even as the much-touted "commodity super-cycle" took energy, base metals and now food prices to record highs in terms of the dollar.

Buying commodities in the hope of growing your capital means you're "selling human ingenuity" reckons SocGen strategist Dylan Grice and, over the last 300-odd years, he's got a point. That's because raw materials are "generally cheaper to produce over time [as] human innovation has lowered the cost of production." Yet ironically, Grice's point is best made in gold, that least ingenious, least human of all pricing yardsticks. Indeed, the difference between gold-priced commodities and gold-priced stocks or housing is that raw materials failed to surge and recover their previous highs after the 1970s bear market. For the last six decades and more, gold has grown consistently more valuable in terms of the world economy's natural resource inputs.

Our chart takes the Reuters-Jefferies CRB Indexa weighted basket of the 19 most heavily traded raw materials, including aluminium, crude oil, live cattle, orange juice and gold itselfand divides it by the dollar-price of gold. As with housing and stocks, gold's most dramatic gains and highest valuations came during economic turmoil, outpacing the price of industrially useful natural resources even amid the severe cost inflation of the 1970s, as well as during the last four years of global financial crisis. Further back, once again, the Great Depression also saw gold's relative worth rise sharply against raw materials as commodity prices sank, but gold was revalued higher by governments, whothen tied to its physical limits as moneywere desperate to devalue currency and so reduce debt burdens in a bid to reflate the economy.

Last in our little survey of gold's relative worth, therefore, come government bonds. There's a problem here because governments are constantly paying old and raising new debt, issuing bonds with a vast range of maturity dates, which unless they default, all revert in the end to par value, redeeming $100 (or £100, 100 and so forth) for every $100 originally lent by investors.

In other words, a broad price basket is hard to construct with the various indicessuch as those offered by S&P and Dow Jonesalso including annual yields to give "total returns," and only running back a few years at best.

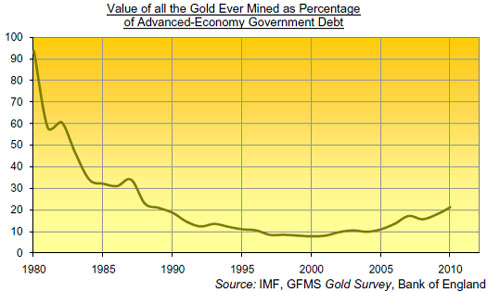

One solution is to weigh gold's total value against the sum total of debt outstandingthe par value of government bonds in issue. Data from the International Monetary Fund, running from 1980, at least, enables us to cover the world's "advanced" economies. And here, based on what we may as well call the "market capitalization" of goldand in contrast to stocks, housing and industrially useful resourcesgovernment debt looks very highly priced, albeit on a mere 30-year horizon.

All the aboveground goldswelling to some 165,000 tons or more today, and including central bank reserves and that mass of jewelry used to store wealth in Asia, as well as the coins and gold bars more typically favored by Western investorshas been swamped, in terms of relative value, by advanced-economy government debt. Back in 1980, their nominal cash values were pretty much identical. Yet the doubling of gold's dollar price from that year's then-record high, plus the two-thirds increase in aboveground gold stockpiles over the last 30 years, has still left the metal worth less than one quarter of what it was at the start of the '80s in terms of rich-world government debt.

That debt, now 18x larger in dollar terms at $36 trillion, has swollen from 25% of those rich world economies' GDP to more than 87% of their annual output. There's very much more of it around in 2011 than in 1980. On a relative basisand given that the par value of debt outstanding cannot fall without default or "restructuring"gold's steady appreciation against equities, U.S. housing and raw materials has barely begun to play out against government bonds.

Adrian Ash

BullionVault

Gold price chart, no delay | Buy gold online at live prices

Formerly City correspondent for The Daily Reckoning in London and head of editorial at the UK's leading financial advisory for private investors, Adrian Ash is the editor of Gold News and head of research at BullionVaultwinner of the Queen's Award for Enterprise Innovation, 2009 and now backed by the mining sector's World Gold Council research bodywhere you can buy gold today vaulted in Zurich on $3 spreads and 0.8% dealing fees.

(c) BullionVault 2011

Please Note: This article is to inform your thinking, not lead it. Only you can decide the best place for your money, and any decision you make will put your money at risk. Information or data included here may have already been overtaken by eventsand must be verified elsewhereshould you choose to act on it.