Graphite has long been a key ingredient in steel, castings, lubricants, vehicle brakes, golf clubs, tennis rackets andno surprisepencils. But this polymer of carbona chemically identical sibling of both diamonds and coalwill become increasingly important in coming years due to its chemical, electrical and thermal properties. Its ability to remain stable in ordinary corrosive environments, conduct electricity and resist heat allow it to serve as a key component in applications like the storage batteries and nuclear-electricity generation stations that will power us into the future.

Coal powered the Industrial Revolution; its chemical twin, graphite, will be of great value in constructing the components of the clean-energy economy, making graphite a true diamond in the rough!

While one may assume that it is as common as the dirt that it somewhat resembles, the supply of graphite is far from infinite. Natural graphite comes in several forms: Flake, amorphous and lump. Of the one million tons of graphite that are processed each year, just 40% is of the most desirable flake type. Only flake and synthetic graphite (made through an expensive process from petroleum coke) can be used in lithium-ion batteries. Graphite mining and processing are limited to a relatively small handful of countries, with China currently producing 70% of the total global supply.

Demand for lithium-ion batteries will increase rapidly as battery-power (electricity) supplements, and will even replace gasoline- and diesel-fueled internal-combustion engines in vehicles as "green energy" expands. While hybrid automobiles such as the Toyota Prius have used nickel-metal-hydride batteries for more than a decade, newer hybrid models like the Chevy Volt, as well as battery-only electric-drive vehicles like the Tesla Roadster and the Nissan Leaf, rely upon the more-efficient lithium-ion batteries that will almost certainly be employed in all hybrid or fully electric vehicles in just a few short years. Large-flake graphite will be very much in demand to produce the hundreds of millions of lithium-ion batteries required for these automobiles.

Governmental bodies are taking notice of just how crucial secure supplies of graphite are. Graphite prices have been increasing in recent months, and investors' interest in this industry is almost certain to climb as word spreads about the impending boom in demand and the companies that will be making moves to meet it.

A Slippery Supply

Global graphite production has held steady at approximately 1 million tons per year over the past decade. The weak demand in the first half of the 2000s, combined with relatively low prices, led to little investment and development of graphite mining and processing capabilities over this time span. Many graphite-producing countries saw a steady drop in annual production between 2001 and 2008, including the Czech Republic, Russia, Madagascar, Zimbabwe, Canada and Mexico. Taking up the slack over this period were the Ukraine, Brazil, India and North Korea. China saw some peaks and valleys in production during this time, but currently produces nearly four-fifths of the world's total supply of graphite, keeping 60% of this output for its own manufacturing requirements.

Japan, the U.S., Europe, South Korea and Taiwaneach of which has an economically significant and well-developed steel industryimport significant quantities of graphite from China. While China is the dominant player in the graphite game, 70% of its production is of the amorphous and lower-value small-flake graphite that is used in industrial applications rather than in batteries.

At this point, the fragmented nature and seasonality of its graphite production base raise some doubts that China will be able to increase its output; in fact, China itself currently imports a significant amount of North Korea's graphite production. Producers in other regions of the world will need to step up their efforts to meet demand, which will require significant investment.

Increasing Applications Driving Demand

Graphite has long been a key component for the aviation, automotive, steel and plastic industries, as well as in the manufacture of bearings and lubricants. High-purity, large-flake graphite is essential for the production of the lithium-ion batteries that are crucial to the consumer-electronics industry. Demand for this form of graphite will rise rapidly as production of larger batteries for vehicular propulsion comes online.

Currently, the iron and steel industries are the largest consumers of graphite. But demand for graphite has been rising for other applicationsresearchers in the field of material science continue to find new uses for this durable, heat-resistant, electricity-conducting substance. Graphite will be used in the construction of next-generation nuclear reactors, which are expected to reach temperatures as high as 1,000°C in their corestriple the temperature of today's reactors.

Graphite is one of the few substances that can resist such heat. It has already replaced asbestos as a health-risk improvement in automotive brake linings and pads. As the standard of living rises in developing nations like Brazil, Russia, India and China, many more vehicles of all types will be added to the world's roadways, increasing demand. Few people realize that 84% of the world's total population lives in emerging-market countries.

Of course, it is expected that a rapidly growing number of automobiles will utilize extensive lithium-ion battery systems to assist with or singlehandedly provide propulsion, which is where the single-greatest increase in graphite demand is anticipated. At present, 2% of all new vehicles sold are gas-electric hybrids, plug-in hybrids or battery-only full-electric drivemost of which still use nickel-metal hydride batteries. It is projected that by 2020, these types of automobiles will represent 5-18% of all sales and almost exclusively be powered by lithium-ion batteries, which are both lighter and more powerful than nickel-metal hydride ones. With 70 million vehicles forecast to be sold in 2020, vast amounts of graphite will be required to manufacture the lithium-ion batteries that will power many of them.

Emerging fuel cell technologies also rely heavily on graphite. One of the more promising types under development, the proton-exchange-membrane fuel cell, requires 100 pounds of graphite per vehicle. Fuel cells will also be used for stationary power generation, as utility providers seek to overcome the inherent inefficiencies around electricity transmission to remote locations.

Perhaps the single greatest testimony to graphite's importance is the concern that governmental bodies have shown about its important role in security. A 2010 European Commission study regarding the criticality of 41 different materials to the European economy included graphite among the 14 materials high in both economic importance and supply risk. A recent WikiLeaks posting revealed that a list known as the Critical Foreign Dependencies Initiative developed by the U.S. Department of Homeland Security and the State Department included graphite mines in China among those overseas sites that could damage American interests if terrorists were to disable them. The U.S. military will also increasingly rely on graphite for battery and fuel cell applications, as the armed forces lessen their dependence on petroleum.

Intriguing Prospects

Top Stock Pick

China Carbon Graphite Group Inc. (CHGI.OB), through its affiliate Xingyong Carbon Co. Ltd., manufactures graphite electrodes, fine-grain graphite, high-purity graphite and other carbon-derived products at its Inner Mongolia facility. The company believes that it is the largest wholesale supplier of fine-grain graphite and high-purity graphite in China. The company reported dramatically higher sales and earnings for the quarter ending Sept. 30, 2010.

Additionally, China Carbon Graphite has started building new forming and baking plants in order to meet the growing demand for high-purity (and higher gross margin) products in the global market. Construction of the new forming plant, which will produce large-size ultra-high graphite electrodes, as well as high-purity and fine-grain graphite, is slated for completion in June 2011. The new baking plant will have 36 furnaces and include 30,000 tons of annual capacity, making it the largest baking plant in China's graphite industry.

The company noted in its recently-filed 10-Q that steel plants in China have been upgrading their electric-arc furnace facilities, which has boosted demand for large-size ultra-high graphite electrodes, a unique and specialized product. China's steel industry, far and away the world's largest, is today rapidly evolving into an industry, like that of the U.S., where electric-arc furnaces requiring graphite electrodes in huge quantities will ultimately be the dominant type of steel furnace used. This is inevitable, as the Chinese steel industry begins to utilize not only imported scrap steel and iron but, soon, domestically produced scrap as well. Shortages have developed and are expected to continue. Earnings could rise materially once these new plants are brought online.

The company's long-term strategy is to diversify and expand its product offering by manufacturing graphite that would be used as a reflector or moderator in nuclear reactors in Chinaa product that would have significantly higher profit margins than its current offerings. At present, there are 11 nuclear power plants in China; 15 more plants are currently under constructionand only one other manufacturer of nuclear graphite pure enough for use in these plants. The company works with Hunan University and Qinghua University to research and develop nuclear-grade graphite.

China Carbon Graphite has approximately 550 full-time employees and a market capitalization of $24 million, and the shares trade at just over a dollar. This price could easily triple once the company begins to sell nuclear-grade graphite.

While some investors are wary of investing in Chinese companies due to the risks and volatility in China's economy, CHGI represents a compelling speculation in the rapidly expanding global graphite industry. It is reassuring to know that internationally recognized accounting firm BDO is the company's auditor of record.

Lower-Risk Pick

GrafTech International Limited (GTI), based in Parma, Ohio, is another strong graphite stock pick. Founded in 1886, GrafTech is one of the world's largest manufacturers and providers of high-quality synthetic and natural graphite and carbon-based products. It has four major product categoriesgraphite electrodes, refractory products, advanced graphite materials and natural graphitethat it manufactures in 11 facilities on four continents, with customers in about 65 countries.< br>

This low-cost global producer has a reputation for product quality, value and service excellence. It is one of the world's largest manufacturers and providers of advanced graphite and carbon materials for the transportation, solar, and oil and gas industries. Approximately 70% of the graphite electrodes that it sells are consumed in the EAF steel melting process, the steelmaking technology used by "mini-mills." According to the company's most recent annual report, it operates "one of the world's most technologically sophisticated advanced natural graphite production lines."

The company's share price has been hovering near $20 recently, and the current market capitalization is $2.4 billion. The stock is very heavily held by institutions such as The Vanguard Group, William Blair & Co. and Calamos Advisors. GrafTech appears to be very well positioned to fully capitalize on the favorable outlook for the graphite industry and the recovering global economy. Indeed, several analysts are projecting robust long-term sales and earnings growth for GrafTech.

Quality Speculation

Northern Graphite Corporation (not yet trading) is a mineral exploration and development company based in Ontario, Canada, that holds a 100% interest in mining claims for the Bissett Creek Project. The Bissett Creek Project consists of approximately 1,343 hectares near Mattawa, Ontario, that contain large crystal graphite flakes in a graphitic gneiss deposit.

The company is about to complete a multimillion-dollar public offering of common stock and plans to use the proceeds to conduct metallurgical testing, prepare a pre-feasibility project report, and continue drilling and bulk sampling onsite. This project is unique in that almost 90% of the anticipated production is expected to be large-flake, very high-purity graphite that should command a premium price on the market.

Moreover, the company's prospectus indicates that the mine's assumed life should exceed 40 years, making Bissett Creek the only significant North American high-purity graphite producer. The deposit is near surface and only 10% of the property has been drilled to date. The project is ideally situated near the Trans-Canada Highway, with rail and power lines close by. Major graphite users in the steel and automotive sectors are in close proximity. These shares could quickly climb from the $0.50 IPO offering price once it begins trading in January 2011.

The Drive Is On

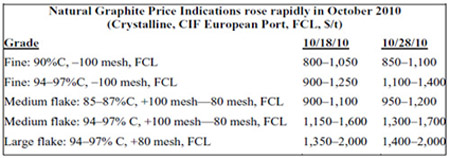

Graphite is one of the quintessential wonder materials of today that will only become more important moving forward. While the supply has proven adequate over the past decade, demand will increase significantly across all sectors of the industry in the years ahead. Already, prices are on the rise, with the best quality large-flake graphite rising in price from a low of $1,350/t to more than $2,000/t during the fourth quarter of 2010 alone. New supply sources will be needed to meet this uptick in demandexisting mining, processing companies and startups alike will require investment. The prudent investor will not want to miss out on this overlooked opportunity. The demand for metals and minerals is now fed by the insatiable economies of Southeast Asia and Brazil. The lag between increasing supply and demand leads to long-term price growth for producers of such natural resources.

Jack Lifton is a leading authority on the sourcing and end use trends of rare and strategic metals. He is a founding principal of Technology Metals Research LLC and president of Jack Lifton LLC, consulting for institutional investors doing due diligence on metal-related opportunities.

Disclosure: I have no positions in any of the stocks mentioned above.