Just under a year ago, I predicted a short-term correction in the price of copper based on analysis of supply and demand (Mercenary Musing, January 18, 2010; Mercenary Musings Radio, January 28, 2010). My prediction quickly came to pass but was of shorter duration than I expected.

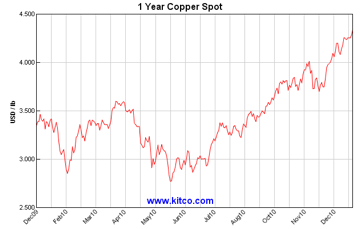

My radio partner Rob Graham and I re-visited the copper market twice in 2010. In our second interview (Mercenary Musings Radio, May 6, 2010), I was bearish on the short-term prospects for copper. The price went on a downtrend that lasted until financial markets righted themselves in early July after a short summer doldrums. By late July, I became bullish on the red metal (Mercenary Musings Radio, July 27, 2010). The price was going up, I felt it would continue, and since then the robust copper market has seldom paused for a respite:

The record copper price is being driven by speculators, hedge fund buying, and Chinese stockpiling and hoarding. Although copper is up 55% since its low of $2.77 in late June, the supply and demand fundamentals simply do not support all-time record prices.

I currently see several reasons why the copper market is overbought and a correction is in order:

- Projected world supply deficits for 2011 have been promulgated as extremely bullish for the copper price. However, these predictions are only 8-11 days worth of current yearly consumption. This is insignificant. Whether there's an actual surplus or deficit in 2011 is primarily dependent on the health of the world's economy and supply factors. One of the estimates factors in an annual supply disruption at 4% of projected world demand. If that fudge factor is removed, the projected 11 day deficit turns into a 3 day surplus. Projected estimates of 2011 supply or deficit are certainly with the margins of error of the predictions.

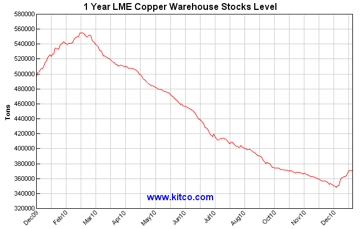

- Worldwide copper warehouse inventories are trending up. The current LME, Comex, and Shanghai warehouse stockpiles, although down 30% from highs in March, are still over two to three times the average for five years preceding 2008's global financial crisis. Inventories are now equal to 10 days of global consumption; this is down from 12 days in March, but is still high compared to the average of 3-4 day stockpiles from 2002 to 2007. LME warehouse inventories have gone up for 12 consecutive days.

- The Baltic Dry Index global freight rates are at a four-month low suggesting that underlying real commodities demand is weakening.

- Copper is in contango and no longer in backwardation as it was from early November until early December. This indicates a lessening of current demand.

- This is the season of low consumption: Northern Hemisphere winter and slow construction season; Western World holidays; and Chinese New Year for 15 days in early February.

- The Chinese, with an interest rate increase on Christmas Day, are attempting to contain inflation. Food inflation is a major concern in developing Asian countries, particularly China, India, and Indonesia where it is the poor's major expense, constituting nearly 50% of income. Significant interest rate increases will cause commodities prices to drop with hedge fund divesture into attractive income-producing sectors.

- Hard commodities, with exception of gold and to a lesser extent hybrid metals (platinum, palladium, and silver), are bulk industrial materials with prices largely controlled by supply and fundamentals. Growth of consumption in the BIIC (Brazil, India, Indonesia, and China) countries is continuing for all base metals but especially copper as the developing world demands electricity. "Dr. Copper, the only metal with a PhD in Economics" is reflecting strong consumption from worldwide emerging markets.

- Countries in the world are depreciating their fiat currencies because of overwhelming debt obligations, huge budget deficits, and overall slow global economic growth. The across-the-board currency devaluation is especially important for the United States dollar since all commodities are priced in the world's reserve currency. Commodity prices naturally will appreciate as the dollar depreciates.

- Speculative money has been pouring into the copper sector and most other hard and soft commodities for the past six months. The main driver is low interest rates and a weak dollar. High risk money will always flow into the sector where short term return is perceived as highest.

- At the present time, commodities are the preferred sector for speculators and hedge funds. This is a similar situation to the first half of 2008, which was the last time we saw across the board record commodities prices.

- Copper is in record territory and the price could continue to go up with no resistance points to the upside.

Some pundits are calling for as much as a 10-20% increase in copper prices if and when physical copper ETFs are trading. They certainly will add near-term volatility, tighten supply markets, and cause price increases. On the other hand, given today's record high price of copper, perhaps the market has already factored in the debut of physical metal ETFs.

If copper prices continue to go higher, we will see a negative impact on major industrial activity with increasing capital and operating costs. This scenario happened previously in early to mid-2008 before commodity prices collapsed in the later part of the year.

At this juncture, it does not appear to me that basic supply and demand fundamentals are strong for the copper market in the short term. There is evidence to indicate that the market is overbought by speculators and hoarders. That said, there are other factors, especially the new copper ETFs that could drive prices substantially higher.

Although I subscribe to Austrian economic theory and disdain Keynes, I will not forget what he said: "The market can remain irrational longer than you can remain solvent." Irrational exuberance for copper could continue at increasing prices.

I also remember the old adage: "The cure for high prices is high prices". Markets always will revert to the supply and demand fundamentals of capitalism.

I get really nervous when the all the experts, pundits, mavens, gurus, savants, and wizards are jumping on board the same bandwagon, whether bull or bear. The current consensus amongst analysts is for a higher copper price.

This is a frothy, risky, volatile market right now. At times like these, I prefer to sit back and wait. I see very high risk in the copper market at present and will watch from the sidelines while the game is played out and winners and losers are determined.

Will the price of copper go up or down in the short term? In the words of former St. Louis Cardinals pitcher and wing nut Joaquin Andujar: "There is one word that says it all: You never know."

I am not buying or selling copper or copper-gold stocks at present. That said, it's always good to take profits when a market reaches all time highs. I will leave that personal decision up to you as a diligent lay investor.

Despite my queasiness about the current state of affairs, I remain a long-term secular bull for copper and other industrial commodities. Simply put, we are not finding and developing enough big copper deposits to satisfy the projected world demand for the next 20 years. I will address this issue at some later date.

Ciao for now,

Mickey Fulp

Mercenary Geologist

Acknowledgements: Jeff Stuart edits my musings; Mark Turner and Gary Tanashian provided thoughtful comments.

The Mercenary Geologist Michael S. "Mickey" Fulp is a Certified Professional Geologist with a B.Sc. Earth Sciences with honor from the University of Tulsa, and M.Sc. Geology from the University of New Mexico. Mickey has 30 years experience as an exploration geologist searching for economic deposits of base and precious metals, industrial minerals, uranium, coal, oil and gas, and water in North and South America, Europe, and Asia.

Mickey has worked for junior explorers, major mining companies, private companies, and investors as a consulting economic geologist for the past 22 years, specializing in geological mapping, property evaluation, and business development. In addition to Mickey's professional credentials and experience, he is high-altitude proficient, and is bilingual in English and Spanish. From 2003 to 2006, he made four outcrop ore discoveries in Peru, Nevada, Chile, and British Columbia.

Mickey is well-known throughout the mining and exploration community due to his ongoing work as an analyst, writer, and speaker.

Contact: [email protected]

Disclaimer: I am not a certified financial analyst, broker, or professional qualified to offer investment advice. Nothing in a report, commentary, this website, interview, and other content constitutes or can be construed as investment advice or an offer or solicitation to buy or sell stock. Information is obtained from research of public documents and content available on the company's website, regulatory filings, various stock exchange websites, and stock information services, through discussions with company representatives, agents, other professionals and investors, and field visits. While the information is believed to be accurate and reliable, it is not guaranteed or implied to be so. The information may not be complete or correct; it is provided in good faith but without any legal responsibility or obligation to provide future updates. I accept no responsibility, or assume any liability, whatsoever, for any direct, indirect or consequential loss arising from the use of the information. The information contained in a report, commentary, this website, interview, and other content is subject to change without notice, may become outdated, and will not be updated. A report, commentary, this website, interview, and other content reflect my personal opinions and views and nothing more. All content of this website is subject to international copyright protection and no part or portion of this website, report, commentary, interview, and other content may be altered, reproduced, copied, emailed, faxed, or distributed in any form without the express written consent of Michael S. (Mickey) Fulp, Mercenary Geologist.com LLC.

Copyright © 2010 MercenaryGeologist.com. LLC All Rights Reserved.