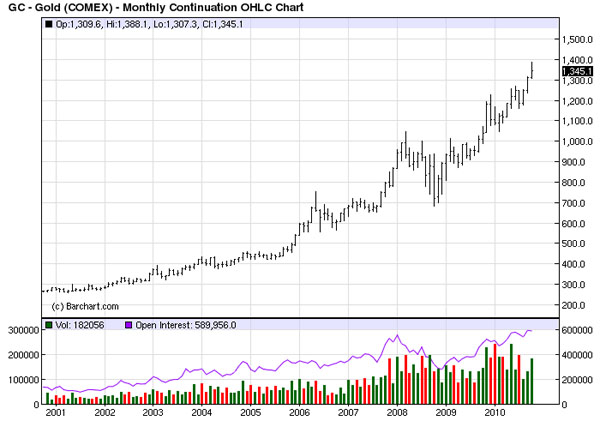

A momentum bull market in gold lasting several months is driven by something more than fear, however. Gold's current rally is also being driven by demandindustrial, consumer discretionary (jewelry) and growing affluence among people in emerging countries. It's also being pursued as a key asset among hedge funds that are always on the lookout for an asset with strong fundamentals, which can be pushed steadily higher with minimum risk of a drastic price reversal. These are all factors one sees in a strengthening economy. Thus, the gold rally can be viewed as another reason to expect more recovery in the global economy.

In a recent issue of Barron's, Michael Santoli tackled the question that some investors are starting to ask themselves: "Is gold in a speculative bubble?" Recently, numerous investment analysts have asserted that when John Q. Public becomes aware of a bull market, that market's days are numbered. Well, the public is definitely aware of gold's recent success. Does this mean the gold bull market is doomed to an inglorious end soon?

To answer this question we need only to go back to the 1980s, at a time when the U.S. stock market was at a point similar to gold's 10-year bull market. Everyone was aware that stocks were a hot investment, and upper-middleclass and wealthy investors definitely had exposure to stocks. Yet, the working middleclass didn't directly participate in the '80s bull market by and large. Not until about 15 years into the bull market did the average Joe became involved with the stock market boom. And, by that point, an asset bubble had definitely developed.

If you look around at the current investor makeup of the gold market, you won't see much evidence that the public is participating in this bull market. Instead, you'll see well-to-do investors participating; though the public hasn't really bought into this gold bull run yet. Even silver, which is the traditional "poor man's gold," isn't exactly a hot commodity with the small investor (notwithstanding the mini-mania in owning silver coins a couple of years ago). Until we see broad participation from an overly enthused public, there is no reason to expect gold's bull market to end anytime soon.

I second Santoli's conclusion on the gold bull market: "But there are just too many sound reasons for people of wealth to continue pushing money toward gold. And there is too much of a discount being placed on gold reserves in the ground based on the valuations of gold mining stocks for this trend to fall apart with any drama anytime soon."

One of the reasons behind gold's most recent rally involves a shift of assets among conservative investors from low-yielding bonds into gold. In a recent issue of his Current Market Update, Jack Ablin of Harris Private Bank observes, "Historically, the opportunity cost for owning gold was considerable. However, now that three-month Treasury Bills offer yields of a quarter of a percentage point, investors feel they are leaving less on the table." Ablin points out that gold's year-over-year gains are typically consistent with a 2%3% inflation rate. "Measured against other commodities, like crude oil, its gains are well within expectations," he concludes.

Gold's impressive rally in September was fueled in part by seasonal demand from jewelry makers and by news that European central banks had sold only 6 tons of gold this year (of the allowed 400 tons to sell from their reserves as part of a five-year European agreement). This represents more than 90% from their sales a year ago. Instead of selling gold, central banks purchased 222 tons from the IMF, which has played a role in increasing gold demand, as well as the price per ounce.

Another factor behind the latest rise has been the currency component of the gold price. Once again, the U.S. dollar has taken center stage as the Dollar Index has been in a downtrend of late and the weak-dollar trend has provided additional fuel for the rally in gold and gold stocks. Friday, the front page of The Wall Street Journal drew attention to the dollar's weakness and served as a podium for discussion of the favorite political strategy of leaders around the globeexporting their countries out of recession. The current U.S. presidential administration has broadcast its intent to boost U.S. exports to help further the recovery in the business sector.

At the IMF/World Bank meeting on October 10th, global finance leaders failed to resolve differences in policy that threaten to drive a full-blown currency war. Martin Crutsinger writing in the Associated Press reports, "Various nations are seeking to devalue their currencies in a way to boost exports and jobs during hard economic times. The concern is that such efforts could trigger a repeat of the trade wars that contributed to The Great Depression of the 1930s, as country after country raises protectionist barriers to imported goods."

A U.S. policy that focuses on exports is conducive to a weak dollar. This policy is also conducive to rising gold prices, which is yet another fundamental factor bolstering gold's long-term uptrend.

The yellow metal continues to garner publicity in the editorial pages of mainstream newspapers and magazines at a rate not seen since before the credit collapse two years ago. Newsweek recently ran an editorial piece entitled, All That Glitters by Nick Summers, who pointed to the conflicting currents of opinion among financial analysts on the metal's near-term future. Summers quoted Paul Christopher, a Wells Fargo strategist, who opined, "Gold up to $1,300 is a rise that's tantalizing, but is risky. We think it has further to run." In contrast, Vanguard's Chris Philips sees the mainstream attention that gold's rise is attracting as a red flag. He warns that gold ETFs may have gotten too big and, therefore, vulnerable to a rapid decline.

Summers himself made this observation: "If gold is a good bet for inflationary times, its performance in the low-growth years since 2002 doesn't add up." He has hit on the essential truth of the matter in that gold's best performance occurs when deflationary risks are the primary economic threatnot inflation. There are two times along the economic long wave that gold's price is most likely to rise: 1.) In the final hyperinflationary period (e.g., the 1970s); and 2.) The final "hard down" phase of the deflationary end of the long wave. This is the part of the long wave we've experienced for almost 10 years. By the time gold's current long-term bull market is over, I think it's safe to assume that financial journalists like Summers will generally agree that gold is the ultimate safe haven for deflationary times.

ETFs

An excellent proxy for tracking and trading the gold price is the SPDR Gold Trust (ETF) (NYSE:GLD). For silver, we use the iShares Silver Trust (ETF) (NYSE:SLV). Quite a few useful ETF products have been introduced and are a great benefit to individual traders who want to participate in the trending moves of precious metals without the hassle of owning the physical metal.

To that end, the ETFs are invaluable and you can be assured of finding one for just about all the precious and industrial metals. For instance, ETF Securities has launched four precious metals funds in the past 14 months, including its flagship ETFS Physical Swiss Gold Shares (NYSE:SGOL), which is the first ETF in the U.S. to invest directly in gold bullion housed in Switzerland. Its ETF for silver is the ETFS Silver Trust (NYSE:SIVR). ETF Securities has also recently introduced a platinum ETF, ETFS Physical Platinum Shares (NYSE.A:PPLT) and a palladium ETF, ETFS Physical Palladium Shares (NYSE.A:PALL).

Another worthwhile ETF for investors looking to participate in the junior gold mining industry is the Market Vectors Junior Gold Miners ETF (NYSE.A:GDXJ). Market Vectors also has a useful fund for tracking the uranium price, the Market Vectors Nuclear Energy ETF (NYSE:NLR).

Speaking of ETFs, TD Ameritrade announced last week that customers can buy and sell more than 100 ETFs with no commission. The announcement is part of a campaign to drum up interest in ETF trading among retail traders. Understandably, small traders have been reticent to trade stocks and ETFs actively since the credit implosion of 2008not to mention the "flash crash" earlier this year. Investors who want to trade ETFs may wish to look into this attractive offer.

Clif Droke is the editor of Gold Strategies Review, providing forecasts and analysis of the leading North American small-cap, mid-tier and senior mining stocks from a short- and intermediate-term technical standpoint since 1998. He is also the author of numerous books, including most recently, The Stock Market Cycles. For more information visit www.clifdroke.com.

Want to read more exclusive Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Expert Insights page.

DISCLOSURE: From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise