So what is risk? In investing, it is the uncertainty of return on capital. So, all investment strategies are risky, whether it is money invested in government bonds, the shares of so-called blue chip companies or start-up companies. In investing, as in life, there are no guarantees.

As an ex-stockbroker, I've always been amused by the so-called risk profiles that clients must complete when opening their brokerage accounts. You know the ones, where you tick the box that guides your broker into suggesting the appropriate investments as per your desired risk tolerance level. The regulators think that by this means they can pigeon-hole risk. That's a joke, but I suppose it saves them from lawsuits based upon inappropriate investment advice contrary to a client's desired risk tolerance level. I repeat that all investing is risky. Three years ago, the sovereign debt obligations of countries like Greece, Portugal, Ireland and Spain were, I am sure, afforded the highest of credit ratings. So there you have it, even countries can declare bankruptcy and before all this Kondratieff Winter is over, I'm sure many will do just that.

In 2000, one of the darling stocks in Canada and certainly one afforded a low risk profile was Nortel Networks. I remember when Nortel's stock price peaked at (CAD) $124.50 per share, it was still being snapped up by investors who categorized it as a low risk. When the dot-com bubble burst, Nortel's share price collapsed as well, falling, if I remember correctly, all the way down to (CAD)$0.67 and with that drop taking a lot of the wealth of the low-risk investors out of their brokerage accounts. Eventually, that blue chip of all blue chip companies expired, but only after its share price had rebounded beyond $4.00 on the promise of a turn around.

Certainly, the highest risk designation at most brokerage firms is afforded to 'speculative stocks.' Please, can someone explain to me what are speculative stocks and what are not speculative stocks? Since all investing is risky, it stands to reason, therefore, that all investing is speculative.

One investment phrase, often used by brokerage firms as a risk criterion is 'Preservation of Capital.' There is absolutely no way and under no circumstances can anyone provide a 100% guarantee for the preservation of capital. Even if you were to hide your cash under your mattress, you wouldn't be able to preserve its value, because of the insidious nature of inflation that our central banks have been foisting upon us for all our lives. Since its inception in 1913, the U.S. Federal Reserve has been responsible for a 95% depreciation in the value of the U.S. dollar.

However, let me tell you why in 2000, I invested all my money in junior precious metals stocks (highly speculative according to the 'Risk Tolerance' criteria at my brokerage firm, and I suspect, at just about every other brokerage firm, as well) ) and in so doing I was extremely confident that I had minimized my exposure to risk. By the way, my investment account has averaged an annual rate of return of about 75% over the past ten years.

It boiled down to the fact that I was absolutely confident that I knew exactly where we were positioned in The Kondratieff Cycle. I knew that we were at the end of the great autumn bull market in stocks (19822000). This determination would herald the onset of winter. This is the deflationary/depression season of the cycle, when debt is virtually expunged from the economy. That process of debt elimination, I knew, would be very painful to debtors and creditors alike and would cause severe problems within the banking system. This, I also knew, would be very bullish for gold. Moreover, I knew that following the peak of the great autumn bull market in stocks, we would experience a vicious winter bear market in equities. So, in early 2000 the risk criteria should have been changed to reflect a gold bull market and a stock bear market. Hence, investing in any gold shares should now have been evaluated as 'low risk' and investing in 'blue chip' stocks should have been considered very high risk. As it turned out, these evaluations would have been appropriate. Because of my understanding of the Kondratieff Cycle, that is how I saw the markets unfolding and that is why I invested accordingly. This considered 'High Risk' strategy was actually, for me, very low risk. It has afforded me significant capital gains since 2000, despite the 2008 stock market debacle.

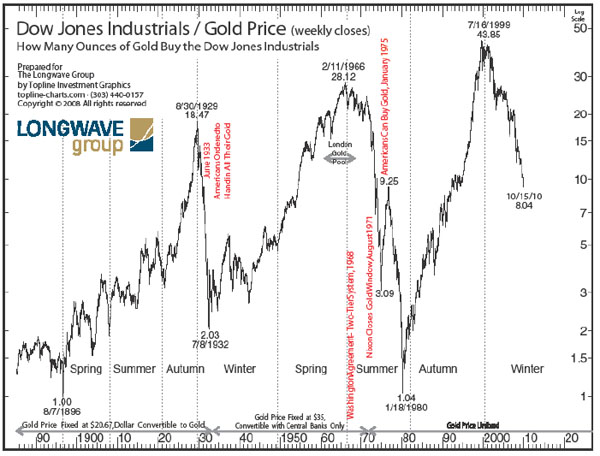

Reinforcing my conviction, there was another metric that I was watching, which signaled we were at the beginning of a huge bull market for gold and a devastating bear market for stocks; that was the dow to gold ratio. (The Dow Jones Industrial Average divided by the price of an ounce of gold). This ratio has always reached an extreme high, when stocks performed well and gold performed poorly, such as in the Kondratieff spring and autumn. Correspondingly, this ratio has always reached an extreme low when the price of gold performs well, and stock prices perform poorly, as in winter and summer. This ratio reached a peak, much higher than any previous peak, as in 1929 and 1966, at 43.85 in July 1999. That peak also, was a signal that stock prices and the gold price were about to reverse direction; stocks to the downside and gold to the upside. (See Ian's Insights Issue 1, Volume 1)

But why junior gold stocks? Wouldn't the senior gold stocks perform just as well? Well, actually not. If you can buy the right juniors at the right time, their price will outperform their senior counterparts. (In an upcoming Winter Warning, available only to subscribers, I will outline how I manage my investment accounts and the criteria I use to select specific junior companies). As the gold bull market got underway you could buy junior gold mining companies with gold in the ground assets for ridiculously low prices. Share prices of companies such as Minefinders, Pelanagio, Nevsun and many others, all with gold in the ground, increased tenfold or more. There are still junior gold companies with significant gold in the ground assets which can be purchased very cheaply today.

What now? I am still almost 100% fully invested in junior gold mining shares. I have included a few short positions in the portfolio through inverse ETFs because the real monetary, economic and financial chaos brought about by the greatest debt bubble in history still lies in the future. When that chaos unfolds, the worldwide rush to own gold and gold mining shares will take prices far beyond where they are today. Owning these shares in such an environment is still, as I see it, a very low risk. Oh, and another thing, the dow to gold ratio is nowhere near its past lows, which has been 1. It is now about 8 having dropped from that 1999 high of 43.85. However, I think the extreme low on the index will be around a quarter to one; that is a quarter of an ounce of gold will buy the Dow Jones Industrial Average. Investing in anything (stocks, long-term bonds, real estate and commodities), other than gold bullion, gold mining shares and preferably, junior gold mining shares is, at this time, a very high risk investment strategy. Nonetheless, we doubt that equity analysts and investment advisors will agree with us.

Ian Gordon

www.longwavegroup.com

Disclaimer: This information is made available by Long Wave Analytics Inc. for information purposes only. This information is not intended to be and should not to be construed as investment advice, and any recommendations that may be contained herein have not been based upon a consideration of the investment objectives, financial situation or particular needs of any specific reader. All readers must obtain expert investment advice before making an investment. Readers must understand that statements regarding future prospects may not be achieved. This information should not be construed as an offer to sell, or solicitation for, or an offer to buy, any securities. The opinions and conclusions contained herein are those of Long Wave Analytics Inc. as of the date hereof and are subject to change without notice. Long Wave Analytics Inc. has made every effort to ensure that the contents have been compiled or derived from sources believed reliable and contain information and opinions, which are accurate and complete. However, Long Wave Analytics Inc. makes no representation or warranty, express or implied, in respect thereof, takes no responsibility for any errors and omissions which may be contained herein, and accepts no liability whatsoever for any loss arising from any use of or reliance on this information. Long Wave Analytics Inc. is under no obligation to update or keep current the information contained herein. The information presented may not be discussed or reproduced without prior written consent. Long Wave Analytics Inc., its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein. In addition, the companies referred to herein may pay a fee to Long Wave Analytics Inc. to be listed on www.longwavegroup.com. Copyright © Longwave Group 2010. All Rights Reserved.