The current run has been strong enough to start bringing the bears out of their short hibernation with warnings about near term collapse of markets and especially resource markets. We don't see the backdrop for that sort of event though we do acknowledge the juniors have had it all their way for few months now. There is growing room for consolidation. On that basis alone it makes sense to be looking for opportunities to harvest some profits. Things could still move higher for a while but it's rarely a bad idea to bring down your average costs and position yourself to do some yearend shopping.

All that said, our view that the Yukon play will if anything be even larger next year has not changed. For that reason, we have included a longer review of a company we have mentioned at the SD level a couple of times recently. It makes a good "Yukon portfolio" holding in its own right and will be generating strong exploration news flow next year which will add discovery leverage to the mix.

Well, a few things actually, but let's start with the fun stuff.

Precious metals had a VERY good month, with gold hitting a number of all-time nominal highs and silver reaching prices not seen since the Hunt Brothers. A glance at the chart above highlights several points about the current gold market.

Viewed on a three-year timeframe the gains are impressive but it doesn't look much like a bubble. The advances have been measured and interspersed with consolidations. If the chart was laid over an S&P graph the strong inverse correlation of 2008 and early 2009 would be seen to have diminished and ultimately reversed. Gold has traded with the equity markets as often as against them lately. Clearly there is something other than just "insurance" driving the buying.

The most obvious and obviously correct answer is the dollar trade. The USD topped just about when the major markets bottomed this summer and the pullback since then has been impressive. The USD Index is off almost 14% in four months, a huge move for the world's reserve currency.

Some of that move was re-risking, though renewed bullishness about the markets is a very recent event. Mainly, the move is vote on the continued lack of progress in fixing the US economy combined with the US Fed talking the dollar down.

Weak economic stats have kept money flowing into the bond market, cutting yields and making US0-denominated holdings less attractive. Bernanke is again talking openly about QEII which is pushing rates down even more. Falling bond yields and lending rates still isn't having much impact on bank lending to industry and consumers but the same can't be said for Wall St. There is little doubt that large traders are taking advantage of rock bottom rates to leverage trades. After months of being too bearish and offside, institutions seem to be piling back into the equity market. We've never be accused of considering those funds to be the "smart money" so we admit this move gives us pause.

In fairness however, it's worth noting that the levels major indices are trading at are not really that bullish. The S&P is only up a couple of percent for the year and is still several percent off its April highs. Much better than the levels in midsummer but hardly levels to be viewed as irrational exuberance.

One market that definitely is exuberant is the venture exchange, our proxy for exploration stocks. As the chart below shows, it's been a heck of a run for the past three months. Unlike most indices it has seen new highs and is up over 15% for the year. An impressive performance but the venture is the exchange most likely to be moved by metal prices and they have very much gone the right way. It's also worth noting that so far at least the Venture has been moving up on strong volumes, something that can't be said for larger markets.

While the move is rational, it's also, admittedly, large. The Yukon gold play can take much of the credit for this. Area plays have an outsized impact on the junior market. Indeed, area plays have singlehandedly pulled that market out of the doldrums before which is one reason we've been focused on it.

So what can go wrong? Metal prices could top out near term. We don't think the gold bull is over, but this is a pretty long run of luck. We're most comfortable with gold when it is backing and filling. Precious metals are due for consolidation which would cool off the juniors, too.

A falling dollar and falling yields is helping the large indices. Those who view gold as a bubble don't see the bond market that way even though it has drawn in50 times as much money this year. That doesn't mean the Fed won't try and push rates even lower if it feels compelled to.

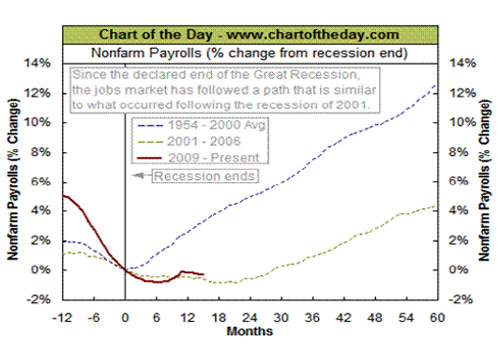

The chart below shows a good reason the Fed feels pressured to act. It compares the changes in nonfarm payrolls to the last recession in 2001 and a number of previous ones. So far the change in nonfarm payrolls is matching the 2001 curve very closely. That is not great news. It took a housing bubble to move employment last time and we know that's not imminent. The bottom for the unemployment cycle came seven quarters after the official recession end last time. Alas, there are few reasons to think that record can be bested this time around though we continue to hope. Lower rates and a cheaper dollar are good for stocks. Many big names in the S&P have international brand franchises and a cheaper dollar expands their bottom line and helps to expand offshore sales too.

None other than Alan Greenspan commented recently that better markets are good for the economy. While the irony in those comments isn't lost on us that doesn't mean "the Artist formerly known as Maestro" is wrong, either. It's possible Bernanke is hoping zero rates will fluff the markets enough to improve animal spirits on their own. The correlation isn't direct but it definitely wouldn't hurt. We know hard money friends horrified by this concept but many in Washington and other G7 capitals are looking at charts like the one above and feeling plenty horrified already and afraid to look at their poll numbers. With fiscal measures seeming to have little impact it is understandable that central banks are falling back on a "whatever works" attitude.

Not healthy, admittedly, but supportive of the market for a while longer if earnings hold up.

It's a secular bull market for metals and resources. We've been saying that for nine years. And we've been right. Another thing we've been right about is the growing importance of the Yukon as an exploration destination and, more recently, Area Play. HRA was there early and continues to follow several of the biggest winners in the play and is tracking dozens of others for potential inclusion in HRA.

CLICK HERE to access your FREE Yukon Report from HRA now! HRA initiated coverage on 15 companies since early 2009the average gain to Oct. 10th, 2010 is 278%!

The HRA Journal, HRA Dispatch and HRA Special Delivery are independent publications produced and distributed by Stockwork Consulting Ltd, which is committed to providing timely and factual analysis of junior mining, resource, and other venture capital companies. Companies are chosen on the basis of a speculative potential for significant upside gains resulting from asset-base expansion. These are generally high-risk securities, and opinions contained herein are time and market sensitive. No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer, solicitation or recommendation to buy or sell any securities mentioned. While we believe all sources of information to be factual and reliable we in no way represent or guarantee the accuracy thereof, nor of the statements made herein. We do not receive or request compensation in any form in order to feature companies in these publications. We may, or may not, own securities and/or options to acquire securities of the companies mentioned herein. This document is protected by the copyright laws of Canada and the U.S. and may not be reproduced in any form for other than for personal use without the prior written consent of the publisher. This document may be quoted, in context, provided proper credit is given.

©2010 Stockwork Consulting Ltd. All Rights Reserved.

Published by Stockwork Consulting Ltd.

Box 85909, Phoenix AZ , 85071

Toll Free: 1-877-528-3958

[email protected]

http://www.hraadvisory.com