I have followed Tesla since the early days, suggesting to buy or sell the stock numerous times. My last suggestion was a buy In January around $113. See my January Seeking Alpha article here, called "A Perfect Storm Hits Tesla in 2022." I think the stock will test $300 so around $295 I will probably suggest selling.

The battery driven EVs have been all the rage with the "climate change" narrative; however, they are not a good enough solution. They are fine for commuters and those driving low daily mileage, but where they fail big time is higher mileage like the transport industry, as an example. A friend had a recent discussion with an Uber driver in Vancouver, Canada, about why he was not driving an EV. He said they are not practical because of battery charge life and long wait and charge times, especially in the colder months when the efficiency of the EVs drops -50% and more.

I did an in-depth article on the charging of EVs, the costs and efficiency. You will be surprised, so here a few tidbits from that analysis.

-

The average price to charge a 60-kilowatt-hour Tesla Model 3 at home is US$6.83, while it's $8.88 for Volvo XC40 Recharge with a a 78-kWh battery pack and $14.92 for a Ford F-150 Lightning with its larger 131 kWh battery;

-

A big catch is that price is based on US$0.11 per-KWh. Where I am in Ontario the average is around Cdn $0.20. California is high at US$0.29 and the U.S. state average is US$0.16;

-

It will take a week to charge your EV at home unless you fork out about $2,000 to install a level 2 charger in your garage that will charge overnight in 8 to 12 hours, depending on battery size;

-

High-speed charging at Electrify America, meanwhile, costs something on the order of US$0.41 per kWh. Some Tesla Superchargers are charging as much as US$0.50 per kWh. That would mean your $6.83 at- home Tesla Model 3 charge would instead cost US$30, while that $14.92 Lightning fill-up jumps to $53.71;

-

The EVs mileage sucks big time in cold weather, so for almost half the year in Canada and northern US. Car.com did a road test with a Tesla Model Y and the range dropped over 50% at 0 to 5 degrees Fahrenheit.

I compared the fueling costs of a Tesla Model 3 with two other comparable luxury sedans, BMW 3 and the Jaguar XE. I used the EPA [Environmental Protection Agency] ratings on these cars. Plus you will pay a higher price for the Tesla and I did not include the cost of a Level 2 charger, so charging cost is at charging stations. I used $3 per gallon gasoline as that is about the current going rate where I am in Florida at that time.

Car Summer Winter

Tesla Model 3 11.2 cents/mile 15.8 cents/mile

BMW 3 Series (gas) 10.4 cents/mile 10.4 cents/mile

Jaguar XE (gas) 10.4 cents/mile 10.4 cents/mile

The battery technology has a long way to go yet. Weight of the batteries is another issue. I have seen estimates that one-third of the payload of a transport truck would have to be the batteries to move it. Hydrogen is going to be a much better solution in many cases and it is in it's infancy like Tesla and EVs in the early days. There are numerous hydrogen test vehicles doing trials and there are few hydrogen filling stations like there were few charging stations six or seven years ago. The U.S. had about 3,000 charging stations in 2016 and 22,000 in 2021.

There are very few hydrogen stations, but they are coming. I saw news this week that a new one is being built at Toronto Airport. Geazone, a British Columbia courier company, recently ordered 40 Toyota Mirais because they are well served by four strategically located hydrogen refueling stations. The British Columbia government has committed $10 million to build more. Meanwhile, there are now some 47 hydrogen refueling stations in California.

Let's compare hydrogen to batteries.

A modern car battery can store 250 watt-hours of energy for every kilogram of lithium-ion. A kilogram of hydrogen, meanwhile, has 33,200 of those watt-hour things per kilo. Yes, hydrogen is more than 100 times as energy-dense as a li-ion battery. The batteries will improve some but that won't be much of a factor in this regard. Hydrogen vehicles will be far lighter than the battery-loaded EVs as well.

Hydrogen is only about 38% efficient versus 80% for lithium batteries The difference is in how the two process electricity. For hydrogen to be as emissions-free as a battery-powered car, you need to electrolyze the water — splitting H2O into, well, H2 and O — with clean wind, solar, or nuclear power. This electrolysis is not nearly as efficient as simply charging a battery. Similarly, in the fuel cell itself, the H2 and O must be recombined to generate electricity. This process, again, is not nearly as efficient as a battery dumping its electrons.

The newer electric cars are capable of achieving an 80% charge in around 30 minutes. However a fuel cell EV (FCEV) is like filling a gasoline car being fueled in under four minutes and can travel around 300 miles on a single tank. Hydrogen is a big winner here!

There are longer term environmental problems with EVs. Thousands of new mines will have to be built for battery metals. ln the Salar de Uyuni – the world’s largest salt flat and an enormous lithium reserve located in southwest Bolivia – mining is threatening to destroy the ecosystem and drain the water supply. Indeed, extracting just a tonne of lithium requires up to 2 million liters of water.

The sourcing of metals for lithium batteries can result in profound environmental damage and can produce as much as 16 tons of carbon emissions. For hydrogen it will be a matter of building green electrical plants to make the hydrogen. A lot of these will have to be built.

Currently less than 5% of EV batteries are being recycled; there is a substantial risk of environmental contamination relating to spent battery disposal. According to recent estimates, by 2030, the number of EV batteries requiring disposal will roughly equal the number currently produced annually. Most EV batteries have a 10-year warranty so that is an approximate lifespan. A hydrogen fuel cell will typically last the life of the vehicle and only require one small battery.

Summary

The biggest advantage for EVs is a lot more infrastructure is available while FCEV infrastructure is in its infancy. The EV electrical use is more efficient than FCEV but the recharging/fueling is a clear winner for FCEV. EVs have a lot of excess weight with batteries so the lighter FCEV could make up on its comparable electrical deficiency. The long-term environmental aspects of EVs have not been considered or have been ignored. FCEVs will play a big part in long haul transportation, taxis, service fleets, and last mile delivery.

The green hydrogen market was valued at US$676 million in 2022 and is projected to reach US$7,314 million by 2027, growing at a compound annual growth rate of 61% from 2022 to 2027. The market's growth is attributed to the lowering cost of producing renewable energy by all sources, the development of electrolysis technologies, and high demand from FCEVs.

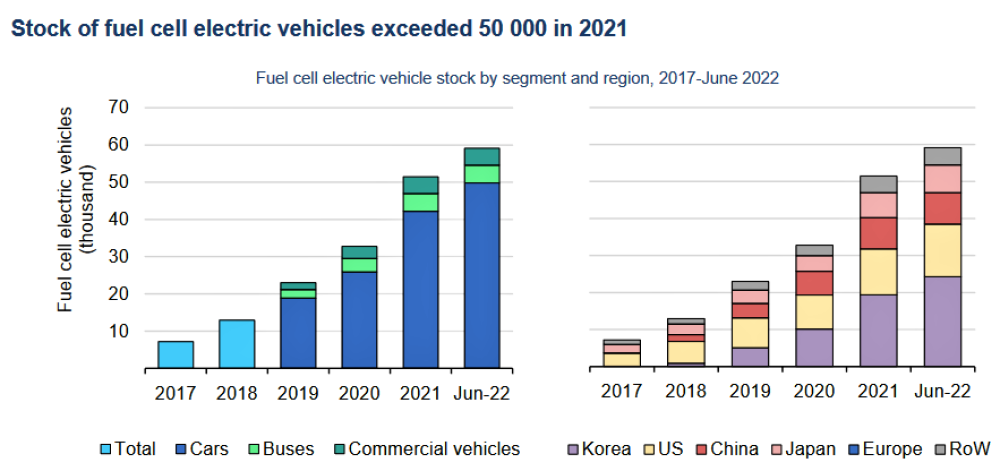

A recent report from the EIA [Energy Information Agency] shows very strong growth for hydrogen in FCEVs. Currently they are consuming less than 1% of the hydrogen market with the current big users being ammonia production and the others being methanol and steel production.

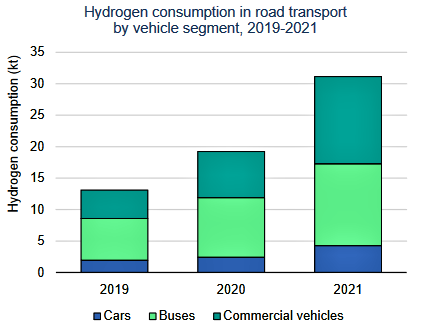

Hydrogen demand in road transport increases 60% in 2021 from 2020.

Heavy-duty hydrogen trucks increased significantly in 2021 (up over 60-fold from 2020).

I have talked about the technology "S curve" numerous times in the past. Once a technology reaches acceptance, and that is where FCEVs have just arrived, you have the strongest growth in the market. For example if the new technology has 5% of the market, the growth to 50% is a 1,000% increase. Currently FCEVs have less than 5% of the EV market.

A company I see as very well positioned for the development of hydrogen and FCEVs is:

First Hydrogen Corp. (FHYD:TSX; FHYDF:OTC; FIT:FSE) TSXV:FHYD OTC:FHYDF

Shares outstanding - 70 million approx.

First Hydrogen is based in Vancouver and London, UK, focused on zero-emission vehicles, green hydrogen production and distribution, and super-critical carbon dioxide extractor systems. The company has designed and built hydrogen-fuel-cell-powered light commercial demonstrator vehicles (LCV) under two agreements with AML Powertrain and Ballard Power Systems Inc. This graphic on their home page shows the FCEV and some bullet points.

These vehicles are currently being trialed with an initial 16 fleet operators in the United Kingdom.

On June 26, First Hydrogen's FCEV was delivered to U.K. utility SSE PLC. The FCEV will begin real-world trials at SSE's operational site at Aberdeen, Scotland, and surrounding areas, which features some of the U.K.'s best hydrogen infrastructure. This infrastructure will enable SSE to experience easy and fast refuelling within five to seven minutes, showcasing a significant advantage of the company's FCEV over battery electric vehicles (BEV), which typically take hours to recharge.

The FCEV has some good reviews/praise such as in May from award-winning fleet management provider Rivus for its smooth and pleasant driving experience. Rivus drivers noted the capability to manage greater ranges and refuel much faster than battery electric vehicles, which will help fleets using this vehicle class to switch to meet zero emissions targets. Following initial journeys on roads in Birmingham, the West Midlands, and South Yorkshire, Rivus' drivers have complimented the vehicle for its "effortless" and "comfortable" driving. Drivers were particularly impressed with the automatic transmission, which they appraised as "easier than a petrol or diesel van to operate" as it does not require gear changes and the vehicle is much quieter to run. Rivus, which manages approximately 120,000 vehicles, including approximately 85,000 LCVs, is the first fleet management company to test drive the first-of-its-kind hydrogen vehicle on U.K. roads.

The company has a very experienced and strong management team. FHYD is led by Malraj Mann, chairman and CEO, who has 40+ years of experience in corporate finance, acquisitions, and financial reporting for both private and public companies.

Rob Campbell is CEO-Energy with 40+ years engineering, commercial, and executive experience, including Chief Commercial Officer at Ballard Power Systems. He has held various previous leadership roles in energy and technology space (including solar and hydrogen).

Steve Gill is CEO- Automotive with 30+ years in automotive, with 20 years with Ford Motor Company (final role: Director, Powertrain Engineering at Ford of Europe); Board Director Ford Technologies; 11 years with Perkins Engines; (final role: Chief Engineer).

Allan Rushforth is CCO-Mobility with 30+ years in automotive and mobility. He has held senior leadership roles in automotive sales, distribution and service, including Marque Group, Lookers, Nissan, Hyundai and Volkswagen/Audi. International experience includes Japan, Korea, and Germany.

First Hydrogen is also active in Canada and has finalized land option agreements with the City of Shawinigan, Quebec. Next they signed a feasibility study agreement with Sacre-Davey for the development of a 35-megawatt green hydrogen production facility and vehicle assembly factory in Shawinigan. The purpose of the feasibility study is to establish the technical and market analysis, engineering review, analysis of grid and water constraints, permitting requirements, environmental constraints, and a review of distribution and operations. The overarching theme throughout the study is to recognize the combined aim to create a zero-emission hydrogen ecosystem.

The production facility will use advanced electrolysis and supply the company's hydrogen-fuel-cell-powered vehicles (FCEV), as well as support other hydrogen-fueled vehicles and applications in the Montreal-Quebec City region. The company's planned FCEV assembly factory will be designed for annual production of 25,000 vehicles per year when at full capacity and will represent a major boost to green technology jobs in the region. The distribution of First Hydrogen's FCEV, throughout North America, will be in combination with the company's hydrogen-as-a-service product offering.

It is very early days for First Hydrogen but it will have a far easier path than Tesla did. Tesla was met with much skepticism and doubt as North America's first EV producer. Now governments and large investment funds are pouring oodles of money into the EV and hydrogen markets.

So far First Hydrogen's FCEV has accumulated 6,000 kilometers on United Kingdom roads, including mileage around London's M25 motorway. The data logging supports vehicle range simulations, which exceed a 500-kilometer range. The vehicle is currently performing with excellent efficiency, including both urban, extraurban (which includes driving at higher speeds), and highway operations. First Hydrogen's LCV fuel consumption figures seen in many driving scenarios are under two kilograms per 100 km, and in mostly urban driving this is 1.5 kg/100 km.

Conclusion

First Hydrogen is at the very beginning of its growth cycle. It will have revenues from selling FCEVs that have now reached acceptance and I expect will soon see major purchase orders. The company has partnered with the Quebec University and numerous other government, investor, and industry partners in the sector. It is not doing this alone. First Hydrogen will also make revenues producing and selling hydrogen.

There is enormous government support for hydrogen in Western countries. In Canada's recent budget, programs supporting First Hydrogen include investment tax credits for clean hydrogen ($17.7 billion) and zero-emission technology manufacturing ($11.1 billion), as well as lower tax rates for zero-emission technology manufactures ($1.3 billion). The federal incentives are in addition to incentive programs offered by the province of Quebec, which the company has picked for its first green hydrogen eco-system.

The stock ran up last year with good news from the company and Canada officially getting behind hydrogen. PM Justin Trudeau and German Chancellor Olaf Scholz met in Newfoundland, Canada, creating an alliance between Canada and Germany. The joint declaration of intent to invest in hydrogen and establish a transatlantic Canada-Germany supply corridor will be the start of establishing Canada as a significant hydrogen producer and advancing on its decarbonization path.

The stock has come down after what now looks like too much hype in the sector, but has put in a bottom and current prices look like an attractive entry point. There is not much resistance until around $3.40 and the the $4.00 area.

| Want to be the first to know about interesting Clean Energy and Alternative - Cleantech investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- First Hydrogen has a consulting relationship with an affiliate of Streetwise Reports, and pays a monthly consulting fee between US$8,000 and US$20,000.

- As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of First Hydrogen.

- Ron Struthers: I, or members of my immediate household or family, does not own securities of First Hydrogen. My company does not have a financial relationship with First Hydrogen. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Struthers Resource Stock Report Disclosures

All forecasts and recommendations are based on opinion. Markets change direction with consensus beliefs, which may change at any time and without notice. The author/publisher of this publication has taken every precaution to provide the most accurate information possible. The information & data were obtained from sources believed to be reliable, but because the information & data source are beyond the author's control, no representation or guarantee is made that it is complete or accurate. The reader accepts information on the condition that errors or omissions shall not be made the basis for any claim, demand or cause for action. Because of the ever-changing nature of information & statistics the author/publisher strongly encourages the reader to communicate directly with the company and/or with their personal investment adviser to obtain up to date information. Past results are not necessarily indicative of future results. Any statements non-factual in nature constitute only current opinions, which are subject to change. The author/publisher may or may not have a position in the securities and/or options relating thereto, & may make purchases and/or sales of these securities relating thereto from time to time in the open market or otherwise. Neither the information, nor opinions expressed, shall be construed as a solicitation to buy or sell any stock, futures or options contract mentioned herein. The author/publisher of this letter is not a qualified financial adviser & is not acting as such in this publication.