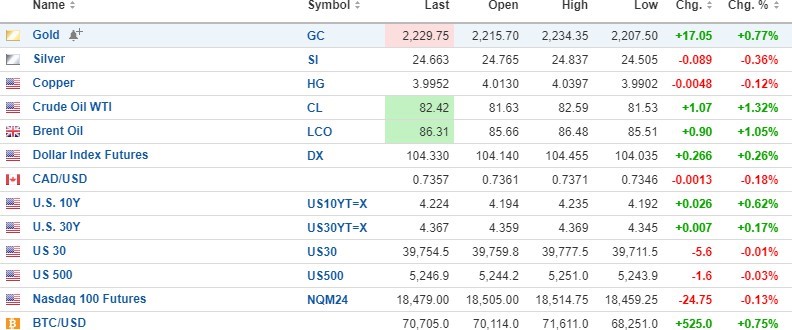

The big news this morning is the $20 move in gold (+.92%) against a stronger USD Index and weak silver (-.19%) and copper (-.26%).

Oil has resumed its uptrend and is the clear winner so far up $1.21/bbl. (+1.49%).

Stock futures are mixed.

Yesterday, I took a 25 contract position in the puts on the assumption that weak oil, copper, and silver would drag gold lower. Well, that did happen briefly, but ended the day marginally higher.

- Ø Bought 25 GLD June $200 puts at $2.40

Yesterday, I wrote: "If they trade down through $2.00, then I am wrong, and I will throw them overboard in a flash," but since silver and copper are not confirming the move in gold, I want to give this trade until this afternoon to see if the sellers knock it back.

To repeat again, I have rarely seen a gold advance that lasted against a rising USD and weak silver, copper, and oil.

Getchell Gold Corp.

There has been no announcement yet, but it is my understanding that Getchell Gold Corp.'s (GTCH:CSE; GGLDF:OTCQB) metallurgical study designed to clarify the recovery rates for the Fondaway Canyon ore is well in progress.

This will put to rest any of the rumors regarding "refractory gold" or "metallurgical issues" that were thrown at me by a few of the investment bankers and analysts who use "bar talk" as an excuse for "due diligence."

I knew that Barrick Gold Corp. (ABX:TSX; GOLD:NYSE) conducted a metallurgical assessment back in 1980 and had arrived at 90%-plus recovery rates, but since that is old news and not 43101-compliant, it was never included in any of the marketing materials.

Once completed, they will produce a Preliminary Economic Assessment that will include an updated Mineral Resource Estimate that will include twelve drill holes that were excluded from the Q1/2023 MRE due to their late arrival in 2022. With the new data, I see an increase in the indicated and inferred resource to something north of 2,500,000 ounces. (That is my estimate, not Getchell's.)

It has been my opinion since late 2022 that the only event that needed to happen to propel GTCH to higher prices was a breakout in the price of gold above $2,100. From August 2020, when gold and the HUI peaked about a month ago, nothing could move the needle for junior gold developer/explorer issuers. The portfolio managers avoided the seniors and the juniors like the plague, with particular revulsion for penny stock developers and explorers.

I surmised that there was no sense in blowing the treasury apart by drilling holes if the market was going to yawn at spectacular results, such as Getchell's 25 meters of 10.4 g/t Au from the North Fork Zone. In any other market environment prior to the 2020-2024 period, the stock price would have moved sharply higher. With the recent breakout in gold, markets are once again moving ever-so-slowly to what I call a "gold-friendly" environment where spectacular drill results will be rewarded with rising share prices and ample funding offers.

With the PEA set to arrive by June along with the new Mineral Resource Estimate, Getchell's share price will be directly correlated to the direction and amplitude of the gold price. It is my opinion that 2024 will be a year when gold will top $2,500, and with that event, the generalist portfolio managers will be forced to begin to allocate portions of their assets under management to the precious metals sector.

When all of those investment dollars begin to migrate to gold miners, it will be akin to forcing the water behind the Hoover Dam out through a garden hose. As the rules of economics dictate, rising demand running into finite supply can only create rising prices. There will be a trickle-down effect where they bid the Barricks and Newmonts up into the rafters, then turn to the Alamos' and Fortuna's and as these large capital flows cascade down the valuation waterfall, they will ultimately find the junior developers with large resources that can be expanded through drilling. That is precisely the point where value-per-ounce for Getchell moves from $14.33/ounce to $50-100/ounce as jurisdiction and expandability take precedence.

This is why one can reflect back on the timeliness of the Getchell debenture offering. To be sure, there were 43 million shares of dilution through the 10-cent warrants, but that also puts CA$4.3 million into Getchell's treasury as they get exercised, which paves the way for an aggressive drill program to expand Fondaway to Tier Two status (3mm ounces).

With gold trading above $2,200 this morning, I wanted all subscribers to understand just how ridiculously cheap the junior gold developers are and why Getchell is an ideal proxy for rising gold prices.

| Want to be the first to know about interesting Gold investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Getchell Gold Corp.

- Michael Ballanger: I, or members of my immediate household or family, own securities of: All. My company has a financial relationship with Getchell Gold Corp. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Michael Ballanger Disclosures

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.