The big news for the past month has been the superb performance of the gold market, which, as of today's earlier high print at US$2,009, was ahead 10.17% since the lows of October 6, making it one of the most powerful moves of the year. It has all of my gold bug buddies dancing in the streets, oblivious to the ravaging effect of rising mortgage rates and the horrific events in the Middle East.

Mind you, I cannot tell you how horrified I was to see a pick-up truck full of young people riding around Toronto blaring horns and cheering the actions of Hamas last weekend. However, for this septuagenarian scribe, it is the rattle and din — the cacophony — of noise surrounding the copper market that had me scratching my head.

I cannot pick up a magazine (or click on a website) these days without reading multiple paragraphs on the "new energy economy" that is arriving this decade that excludes ICE's and replaces them with EV's. I have fully embraced the notion of an electrically powered world where the cleanest of all energy sources — nuclear power — boosts global electrical output by many multiples, leaving literally nothing of harm in its wake.

I accept the proposition that the world is going to need to amplify its electrical storage capacity and, in doing so, increase demand and usage of battery elements — cobalt, nickel, and lithium.

The world market for elements such as uranium and lithium has also recognized the oncoming tsunami of demand by re-pricing both of them to multi-year highs as stockpiling has begun in earnest as governments move to re-classify them as "critical metals." The narrative surrounding the "Electrification Movement" and the three main metals constituting the "electrification trilogy" is filled with a plethora of "noise" — scatterbrained snippets of inane opinions and theories both bullish and bearish and always rebutted forcefully by those cretins in the oil and gas industry that sit back and howl with laughter at the legions of "greenies" and "libtards" that actually believe that gas stations will have disappeared by 2030.

Between the Gen-Z-ers gluing themselves to highways and the U.S. government emptying the Strategic Petroleum Reserve in order to teach Vlad the Impaler a lesson, the entire narrative surrounding the move to increase the electricity grid is one giant cacophony of disjointed arguments.

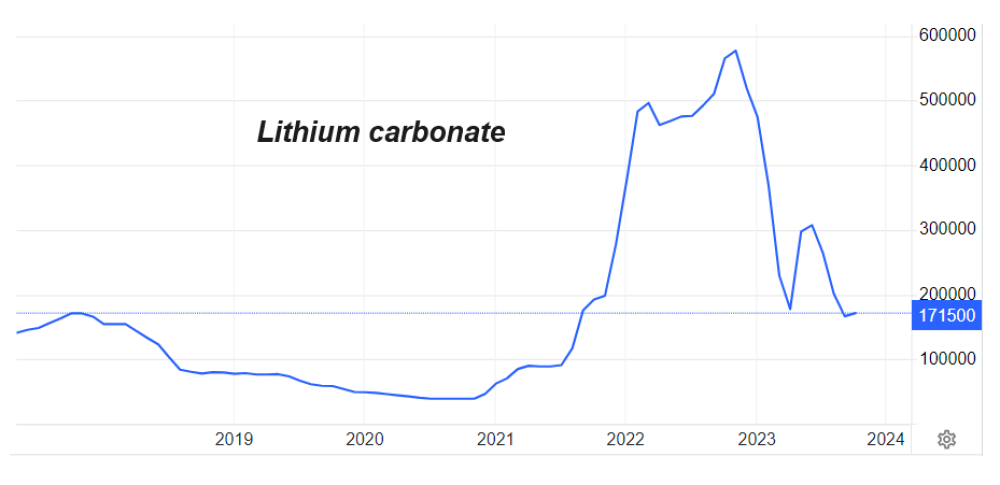

However, if there is one conundrum that baffles me, it is the copper market. Markets pronounced their verdicts on the likelihood of a successful transition to electric by way of a massive move in prices for lithium carbonate, advancing twelvefold from mid-2020 to late 2022.

Lithium

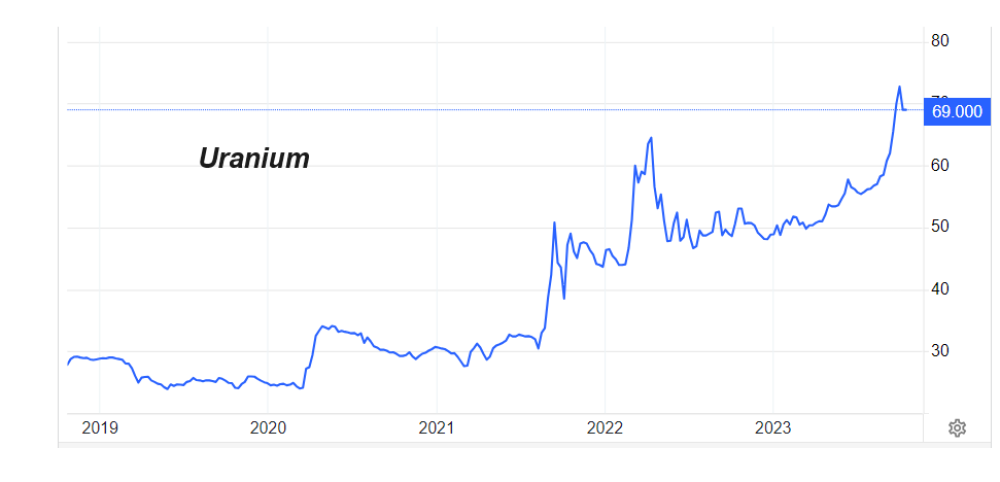

Likewise, markets seem to buy into the prospect of attitudes toward nuclear energy changing for the better as uranium prices have moved from sub-US$20/lb. to over US$73/lb. Between late 2017 and late 2022, but nowhere near the highs of 2009 at almost US$135/lb.

Likewise, markets seem to buy into the prospect of attitudes toward nuclear energy changing for the better as uranium prices have moved from sub-US$20/lb. to over US$73/lb. Between late 2017 and late 2022, but nowhere near the highs of 2009 at almost US$135/lb.

Uranium

Glancing at the charts of two of the three critical materials required for the electrification transition to occur, you would conclude that those markets have reacted to the certainty of accelerated demand and probable shortage conditions to boot.

A take-it-to-the-bank lay-up, you say?

Not so fast when you look at the chart of the one metal that makes it all possible — copper.

Copper

I ask myself a critical question: "How can investors take the new clean energy source metal (uranium) and the energy storage metal (lithium) to record highs and leave the metal necessary in the transmission of electricity (copper) behind and in a bear market?"

They say copper is responding to the prospect of lower growth brought about by higher interest rates. They point to debt-ridden property giants in China curtailing purchases typically intended for new construction projects as the reason that there was a 50% increase in LME inventories last month. Yet, looming behind all of this short-term noise are reports from the IEA and the International Copper Association that project a 26% increase in supply by 2035, which is sharply below the 50% increase in anticipated demand.

From my vantage point, you cannot have large sovereigns stockpiling uranium and lithium today while ignoring copper because of the short-term cacophony of possible price restraints. If the world fails to revise the permitting process allowing the unimpeded construction of new, high-capacity copper mines, there is going to be a problem. More importantly, if the capital markets continue to treat copper like the freckle-faced, misbehaving brat in the corner of the classroom, investors will continue to be wary of making new investments in junior exploration and development companies that are always the originators of the world's new "discoveries of merit" that grow to supply the world with the ores so critical to the human condition.

This is precisely why it all must change, and that change will begin with a turn in the price trend for copper. I have never been able to hear the crack of a starter's pistol at the beginning of a bull market, and I doubt that there will be anything closely resembling one this time around. However, it seems to me, as plain as the nose on one's face, that copper will be in shortage conditions between now and 2025 with the severity growing exponentially as the fifty-seven nuclear reactors currently under construction around the world are fired up.

Gold (and Silver)!

After major rallies in gold or stocks or Bitcoin or anything, for that matter, the Twitterverse is always littered with thousands of tweets by individuals taking credit for calling the exact bottom. Well, for gold, here is the chart I posted on October 3, the day before VanEck Gold Miners ETF (GDX:NYSEARCA:) bottomed into an RSI of 26.79 and a price of US$25.62. Thirteen days later, and at 11:29 this morning, it hit US$30.16.

It was a superb call but one that has been very rare in this bear market year.

As the saying goes: "You have to be good to be lucky (and vice-versa)…"

SPDR Gold Shares ETF (GLD:NYSE) was bought at US$172.50 on Canadian Thanksgiving Monday with the GLD December US$170 calls bought on a scale-in order during the week of October 9-12.

I backed away from the Friday gap and instead filled the final 20% into the Monday pullback resulting in an average price of CA$7.78 per contract. This morning, the GLD:US exploded up into overhead resistance with a print up to US$185.23 but I established a target price of US$184.00 and told subscribers that only a move through that level — the July highs — would take the RSI into "overbought" conditions, which it did, on a move to 71.52 before backing off.

The Twitterverse was inundated with words like "shenanigans," "slammies," and "manipulations," but the reality was that gold was simply overbought this morning, and because of that, I put out "Sell" on the remaining 50% at US$16.00 which when added to the US$14.75 I got yesterday, gave me an average sell price of US$15.375 versus the average cost of US$7.78 resulting in a 97.6% return in under two weeks.

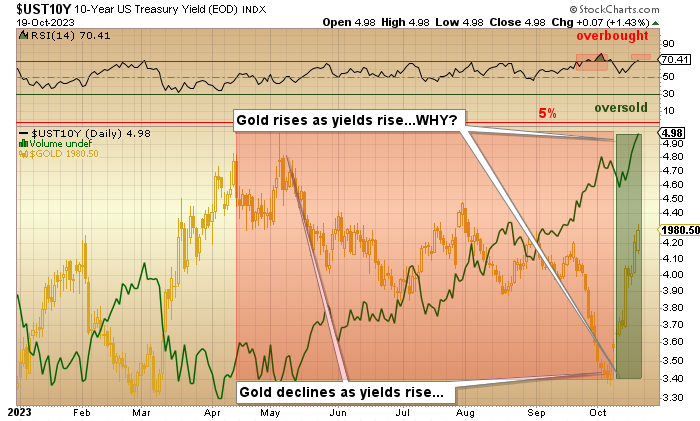

I put out a note this morning that showed this chart:

You will notice that gold moves in an inverse direction to interest rates, and that is not really much of a surprise to anyone who follows the gold market. You can see how gold went into a prolonged decline at the exact point where the 10-year yield started its ascent from the 3.30% level back in April, but in and around the start of October, that negative correlation ended, and gold and yields have been rising in tandem ever since.

Now, everybody with a keyboard and a Twitter membership has been explaining in torrid detail the reasons for gold's explosive move, but if there is one thing about gold that the "younguns" do not seem to grasp, it is that gold, unlike everything else on the planet, has an uncanny predictive ability. The reasons it goes up or down are usually only revealed later and are never the reasons given on Kitco or anywhere else in the mainstream media, for that matter.

Gold moved up US$60 per ounce on Friday, October 6, giving rise to speculation that someone was "front-running" knowledge of the impeding Hamas invasion. When gold bottomed in mid-March 2020, neither the global central bankers nor the elected leaders had said anything about trillion-dollar bailouts or helicopter cash drops to households around the world.

Gold sniffed it out and it was only months later, after it had rallied from US$1,450 to US$2,089 that the world learned of the sheer magnitude of the monetary and fiscal stimulus packages that were thrown with reckless abandon at what turned out to be a nasty little flu bug and not the second coming of Ebola or the Bubonic Plague.

Something has changed in the gold market, and I am the first to admit that I know not of its origin. All I know is that when gold moves in a manner that is unorthodox, all I can do is apply my rudimentary knowledge of technical analysis coupled with ample doses of prayer, rabbit's feet, four-leaf clovers, and Haitian Death Chants and hope to hell that I am on the right side.

Gold goes wherever it wants to go. If we are lucky, we find out the reason weeks or months later.

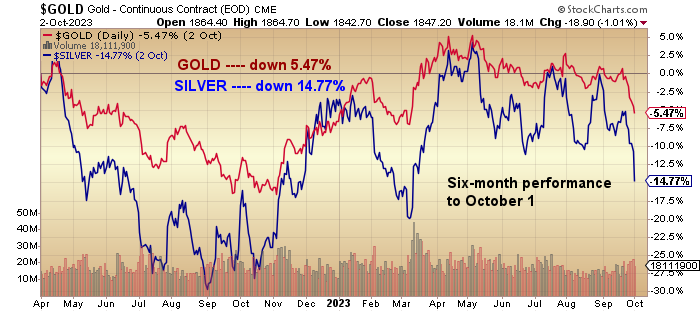

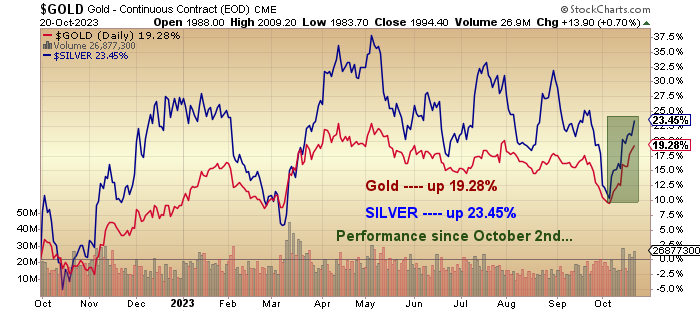

Notice how silver was lagging gold through the last six months, down 14.77% to gold's 5.47% decline.

Suddenly and with little warning, silver started to outperform gold, and as one of my most reliable indications of the health (or frailty) of any bull market in the precious metals, the silver market is now officially ahead of gold for the October monthly performance.

If this continues into month-end and on into November, I expect to see gold at new all-time highs and silver well into the US$30s. I am not yet adding to my silver miners, having added Norseman Silver Ltd. (NOC:TSX.V; NOCSF:OTCQB) earlier in the month, but they are now officially on my radar screen, starting with Pan American Silver Corp. (PAAS:TSX; PAAS:NASDAQ) as a possible option play.

Stocks

I own a modest position in the SPDR S&P 500 ETF (SPY:NYSE) and told everyone this week that while I am betting on a year-end rally to take the SPY:US to between US$452 and US$457, my abort button is programmed to activate the moment the U.S. 10-year prints 5.25%.

It went out at 4.917% after trading up to 4.999% this morning. If this spike in long rates does not soon abate, I cannot see stocks mounting an advance into year-end and fear a 2018-type decline instead, which would not be fun.

The week ended with me enjoying something that has been annoyingly elusive in 2023. It is called a "capital gain". If it were not for some fortuitous trades in the SPDR S&P 500 ETF (SPY:NYSE) and GLD:US markets this year, I would be lamenting a pitiable performance in many of the junior miners I own.

To be absolutely clear, I do not need to hear that I should not worry "because everyone else has been demolished, too," as a panacea for my junior gold and silver portfolio. The next time I hear that insincere babble, I am reaching for my Louisville Slugger that stays at all times beside my Hockey-Night-in-Canada chair with the vibrating backrest.

Forewarned is forearmed…

| Want to be the first to know about interesting Critical Metals, Base Metals, Cobalt / Lithium / Manganese, Gold and Silver investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- Norseman Silver Ltd. is a billboard sponsor of Streetwise Reports and pays SWR a monthly sponsorship fee between US$4,000 and US$5,000.

- As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Norseman Silver Ltd. and Pan American Silver Corp.

- Michael Ballanger: I, or members of my immediate household or family, own securities of: All. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Michael Ballanger Disclosures

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.