Many precious metal stocks that are known or perhaps remembered as silver stocks, actually can have a substantial amount or around half of their production from gold and many have been ignored in the gold bull market. One of the reasons I picked Pan American Silver Corp. (PAAS:TSX; PAAS:NASDAQ) and Coeur Mining Inc. (CDE:NYSE) and both are lagging our gold picks in performance. However, they are still up 73% and 27% respectively. Pan American has performed among the best with the silver stocks.

To make my case, let's have a closer examination of my recent pick, Hecla Mining Co. (HL:NYSE).

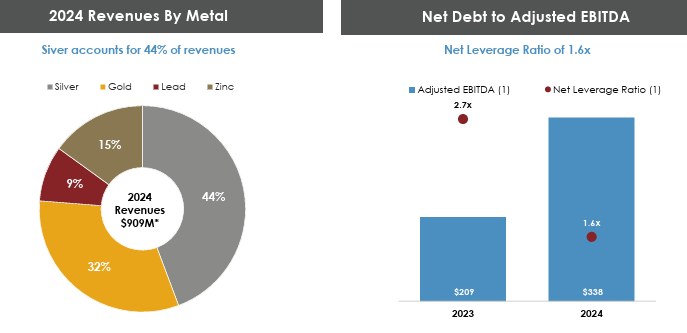

As you can see in their presentation, 32% of revenue in 2024 was from gold. In 2024 Hecla sold 132,442 ounces of gold at an AISC of $1,990 and their realized price in 2024 was $2,403 per ounce.

Their realized silver price in 2024 was $28.58 per ounce.

In 2025 Hecla could easily realize $3,100 per ounce gold sold and probably higher. That is a 29% increase and all that will go to the bottom line. Costs per ounce are expected to be around the same in 2025 as 2024. Cash flow from operations for the year 2024 was $186.5 million and increased 19% over the prior year due to higher revenues.

At $3,100 gold, I calculate it could add an additional $75 million in cash flow from just the increase in the gold price. We can also count on higher cash flow from silver sales over their $28.58.ounce realized price in 2024.

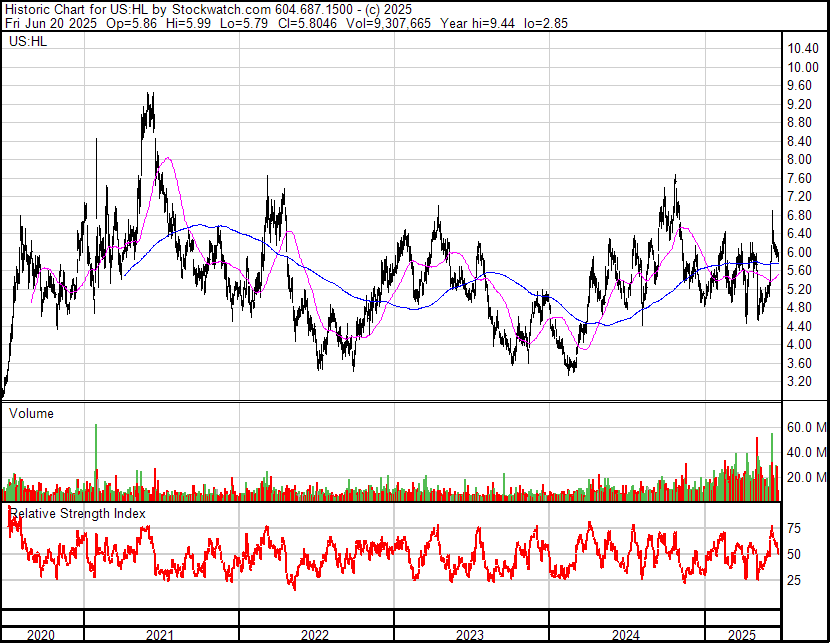

Hecla stock ended 2024 on a down slope around $5.20 and at current prices around $6.00, the stock is not reflecting much if any higher cash flows from rising gold and silver prices. A move to $7.60 will just get the stock back to the 2024 high.

Looking at a 4 year chart, the stock just seems to be confused and undecided. As I pointed out on the chart in my original article on Hecla, there is a triple bottom and a break above the down trend channel since 2024.There is quite a pick up in volume as investors are starting to take notice of Hecla. The next major move is up.

What is Wrong? The Risks

Basically all the risks and impediments to growth reside with their Canadian operations, all because of slow permitting. Permitting has slowed to expand Keno Hills in the Yukon from 440 tpd to 600 tpd. Since Victoria Gold Corp.'s (VGCX:TSX; VITFF:OTCMKTS) heap leach pad incident, the First Nation of Na-Cho Nyak Dun have concerns. Keno Hill is in their territory so this has slowed the permitting process to increase to 600 tpd. In Quebec the permit timing of the Principal and West Mine Crown Pillar expansion pits at their Casa Berardi mine is unknown. None of these issues affect current production and cash flows and higher projections for 2025, but they are slowing substantial improvements at both mines.

We hear nice talk from the new Canadian government about speeding up permitting, but above is reality. This news just out from Taseko is bad timing and contradicts government narrative.

10 to Over 15 Years To Develop a Mine in Canada, How About 30 Years and Nothing

The largest copper and gold deposit in Canada has been freed from three decades of conflict.

The province confirmed in a Wednesday, (June 18) release that it will be working with the Tsilhqot'in National Government (TNG) to determine the process for any further mining activity at Teztan Biny (Fish Lake), as part of a deal to end an enduring dispute. In their own release, Taseko said the province has paid the company $75 million as part of the deal. This would only be a fraction of the amount invested to prove the deposit. I wonder if it even covers Taseko's decades of legal costs?

The agreement between the TNG, the B.C. government and Taseko Mines (TSX:TKO) essentially prevents Taseko from doing anything other than selling its holdings in the area if a project were to be ready to go ahead, while ensuring any future mining-related activity will only occur with the consent of the Tŝilhqot’in Nation.

"We fought for decades to protect the Teẑtan Biny area from mining proposals that threatened our Tŝilhqot’in values and way of life," said Otis Guichon, Tribal Chief of the Tŝilhqot’in National Government."(This deal) is something that we can all be proud of."

It also includes a 22.5% equity interest in the New Prosperity mineral tenures, put into a trust for the future benefit of the Tsilhqot'in Nation. Taseko maintains a majority interest with 77.5% which the company can sell at any time. And who is going to buy something that can't be built?

So a No in Canada, Just Go to the US

As the prospect of building its New Prosperity copper mine in B.C. has all but evaporated, the company has turned its focus to Arizona. Taseko plans to spend US$230 million to develop the Florence copper project in Arizona. That’s on top of the US$80 million already spent bringing the project through the permitting process.

"We think we’re going to get permitted and start construction next year," Taseko CEO Stuart McDonald said in an earnings call in November.

I followed Taseko a decade or more back, because Prosperity was no ordinary discovery. It was the largest in Canada and 7th largest copper deposit in the wold. The deposit contains 5.3 billion pounds of copper and 13.3 million ounces of gold. If you want to learn anymore detail, there is a great video from nine years ago on prosperity.

For all the new talk from the Carney government about speeding up mine development, this news is very bad timing and so is this.

Nothing has changed, the Liberal government just talks a nice story.

BC Ferries set off a tidal wave of controversy last Tuesday after announcing a major shipbuilding deal with a Chinese state-owned enterprise (Merchants Industry Weihai Shipyards). Vancouver Island Conservative MP Jeff Kibble raised the issue in Wednesday’s question period, accusing the Liberal government of rewarding the provincial carrier for selling out Canada’s national interest. The Liberals are set to hand over $30 million (in federal subsidies) to BC Ferries while BC Ferries hands over critical jobs, investment and industry to China," said Kibble.

More Economic Woes

Today in the U.S., Philadelphia Fed Manufacturing activity in the region remained weak. The survey’s indicator for current general activity remained slightly negative -4.0, unchanged from May. The firms reported overall decreases in employment, and the employment index fell from 16.5 to -9.8 this month, its lowest reading since May 2020.

The Conference Board Leading Economic Index® (LEI) for the US ticked down by 0.1% in May 2025 to 99.0 (2016=100), after declining by 1.4% in April (revised downward from –1.0% originally reported). The LEI has fallen by 2.7% in the six-month period ending May 2025, a much faster rate of decline than the 1.4% contraction over the previous six months.

Markets are over valued, the economy is sliding so high cash levels are warranted

| Want to be the first to know about interesting Silver investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Pan American Silver Corp.

- [Ron Struthers]: I, or members of my immediate household or family, own securities of: [Hecla Mining]. My company has a financial relationship with [None]. My company has purchased stocks mentioned in this article for my management clients: [None] I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Struthers Resource Stock Report Disclosures

All forecasts and recommendations are based on opinion. Markets change direction with consensus beliefs, which may change at any time and without notice. The author/publisher of this publication has taken every precaution to provide the most accurate information possible. The information & data were obtained from sources believed to be reliable, but because the information & data source are beyond the author's control, no representation or guarantee is made that it is complete or accurate. The reader accepts information on the condition that errors or omissions shall not be made the basis for any claim, demand or cause for action. Because of the ever-changing nature of information & statistics the author/publisher strongly encourages the reader to communicate directly with the company and/or with their personal investment adviser to obtain up to date information. Past results are not necessarily indicative of future results. Any statements non-factual in nature constitute only current opinions, which are subject to change. The author/publisher may or may not have a position in the securities and/or options relating thereto, & may make purchases and/or sales of these securities relating thereto from time to time in the open market or otherwise. Neither the information, nor opinions expressed, shall be construed as a solicitation to buy or sell any stock, futures or options contract mentioned herein. The author/publisher of this letter is not a qualified financial adviser & is not acting as such in this publication.