With silver seemingly unstoppable — we touched $53 yesterday — I want to look at top silver pick, Sierra Madre Gold and Silver.

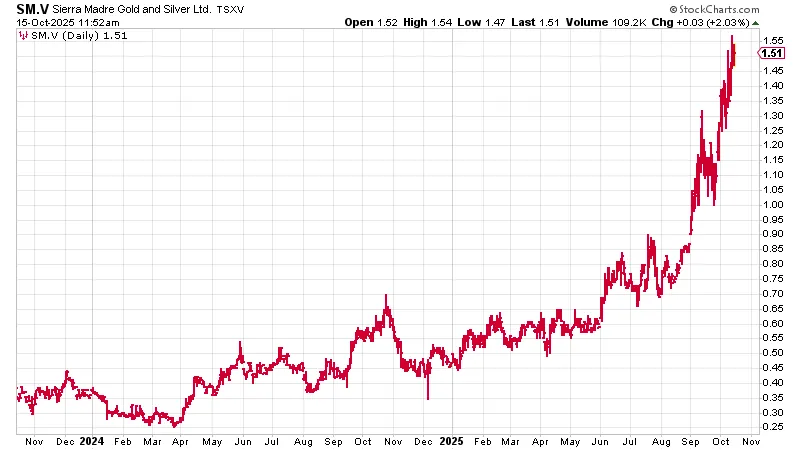

This has been a big win for us, with braver readers picking it up below 30c 18 months ago, when junior mining really was in the doldrums.

Today, we are flying high at $1.50.

What, then, to do? Take profits? Buy more? Hold?

I met with CEO Alex Langer last week, and I'll let you know what I think.

But first. . .

A Word on Silver

Silver fever is in the air once again.

The internet is abuzz. Emails are flying about — "the end of cheap silver is over." The Royal Mint has run out of supply. Physical silver is trading north of $100/oz in China. You can't get silver at $50. The paper markets are going to fall apart.

Supply will catch up. It always does. But for now, with the recent price surge, investment demand has shot up, and it has created a shortage in London, where supply was already tight. Lease rates — the cost of borrowing metal — have jumped above 30% in recent days. Bid — offer spreads have risen from a typical 3c to 20c. The spread between the London spot price and the Comex future price typically sits at -30c/oz.

Suddenly, it's $3/oz and silver has gone into backwardation: the spot price is now higher than the futures price. (That happened in 1980 as well, as silver was rocketing).

This backwardation has led traders to fly 1,000 oz bars from Comex vaults in New York to London. The price gap justifies the transport costs, and remember: silver is bulky compared to gold. It is not cheap to fly.

Silver can carry on rising. It's a bull market. The cup-and-handle pattern that I keep banging on about has come into play.

$100/oz silver is a real possibility. It's true this long-overdue bull market in metals has barely got started. There is more than a decade of mining and metals underinvestment to work through.

But remember this is silver. If it can find a way of letting you down, it will.

Everyone is screaming, "new paradigm" while thinking to themselves, "how long do I wait before I pull the trigger and sell?"

What to do? And when to do it?

$50 is/was a huge line in the sand. There is a lot of price memory there. I thought we would bounce down off it. We haven't. We've gone through. Maybe this is a genuine breakout, maybe it's one of those suck-people-in-before-we-crash-the-price jobs.

But we are now at $53. There is no resistance overhead. Typical action would be for us to rally a bit more, pull back to the breakout level, re-test, then off to new highs. That's when we start heading towards those cup-and-handle highs.

$50 silver in 1980 translates to over $200 today . . . but it's silver. Never forget that.

Sierra Madre Gold and Silver

My favorite silver play, my largest silver position, and one I have covered on these pages before, is Sierra Madre Gold and Silver Ltd. (SM:TSX.V; SMDRF:OTCQX).

It's been a big win.

What to do?

Well, it can be higher. The company is on a really good trajectory: expanding at just the right time.

Here are my thoughts.

This Canadian-listed company, market cap CA$270 million, has a producing mine in Mexico — La Fortuna — which it acquired from silver mining giant First Majestic Silver Corp. (AG:TSX; AG:NYSE; FMV:FSE), which had put it under care and maintenance during the bear market. While the quality of the asset was not in doubt, it was deemed too small for a company of First Majestic's size to bring back into production, hence the partnership with Sierra Madre.

Sierra Madre spent several years putting it back into production, meeting most targets ahead of schedule, though the cost of production per ounce was higher than anticipated at $30. More on this in a moment.

Full-scale commercial production began in January of this year, and currently stands around 700,000 silver equivalent ounces (it also produces about 4,000 oz of gold) per annum.

Production costs will come down from $30 to about $20/oz over the next two years as it replaces rented equipment with its own equipment ($4/oz), increases efficiency and turnover, and catches up its development ($5-6/oz). Lower production costs will be one of the big catalysts for the stock over the next two years.

At $50 silver, if you slash your costs from $30/oz to $20/oz, your previous profit of $20/oz is now $30/oz. In other words, you have grown your profits by 50%.

The company currently processes about 300-350 tonnes per day (TPD) of rock. Recent investment in the company means improved equipment, and processing will rise to 750-800TPD of rock by Q2 of next year. Production will double in other words. So that is the second catalyst for the stock.

Increased production at a lower cost.

It is aiming to double that 750-800 to 1,500 TPD by Q3 of 2027.

Remember — unusual in mining — this company has a habit of reaching targets

The La Fortuna mine is projected to have at least 15 years of life, by the way.

The blue sky comes from the exploration. This is a district-scale opportunity.

"This is why we bought the property," CEO Alex Langer tells me. It could be "the largest undeveloped silver district in Mexico."

There are many past producing mines on the property (most closed in the early 20th century), which produced over a million ounces of silver annually. One of the mines employed over 10,000 people.

Geologic mapping has identified 60km of mineralized veins. Head grade at one of the properties is 860g/t silver. It has over 1,400 of historic drill holes totaling 236,000 meters, all mapped. It also has multiple historic resource reports, one showing 200 million ounces in the 1990s, which never materialized due to the bear market. There is plenty of metal there, in other words, but it needs proving up to modern standards.

Exploration begins next year.

First Majestic had plans for a 3,000tpd mill at one of the properties in this district. You might wonder why it didn't explore the property itself, and the reason is that they own a huge stake in Sierra Madre — 38% — so they can sit back and let them do the work.

The goal is to grow what was a development play, now a junior producer, into a mid-tier silver producer. The expansion plans are coming just as silver is rising. It feels like just the right point in the cycle.

Production costs are coming down, meaning profits should double. Production itself is doubling, so profits should double again. If the silver price goes to $100 and this thing makes a major discovery — IF! — and turns itself into a district-scale producer, then this becomes an asymmetric bet.

Flying Frisby readers who got into this one at 30c or 50c may be tempted to take some profit. From a risk-management point of view, it makes sense to do this.

But this remains a compelling investment even at $1.50.

Ultimately, this sinks or swims with the silver price, but even if silver just stays where it is, there is still enormous potential for growth.

If you'd like to read more from Dominic, you can sign up for The Flying Frisby here.

| Want to be the first to know about interesting Silver and Gold investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- Sierra Madre Gold and Silver Ltd. is a billboard sponsor of Streetwise Reports and pays SWR a monthly sponsorship fee between US$3,000 and US$6,000.

- As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Sierra Madre Gold and Silver Ltd.

- Dominic Frisby: I, or members of my immediate household or family, own securities of: Sierra Madre Gold and Silver Ltd. My company has a financial relationship with: None. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.

Dominic Frisby Disclosures: This letter is not regulated by the FCA or any other body as a financial advisor, so anything you read above does not constitute regulated financial advice. It is an expression of opinion only. Please do your own due diligence and if in any doubt consult with a financial advisor. Markets go down as well as up, especially junior resource stocks. We do not know your personal financial circumstances, only you do. Never speculate with money you can’t afford to lose.