Grassroots opportunities like this rarely emerge in mining exploration. Yet Canary Gold Corp. (BRAZ:CSE; CNYGF:OTC) presents one of the most compelling opportunities I've encountered in recent years.

This prospect is situated in Brazil, near Bolivia's border, where the Andes' gentle foothills intersect with the Amazon Basin's flat periphery.

For approximately 15 million years, the Madeira River — a tributary of the Amazon — has been carrying tiny gold particles from the Andean mountains into the level edges of the Amazon Basin.

Just within recent decades, Brazilian government estimates suggest that MILLIONS of gold ounces have been "captured" or extracted as numerous — sometimes hundreds of — river vessels with vacuum systems have extracted the riverbed material for decades — dating back to the 1970s — and then separate the gold particles using traditional placer mining techniques.

Here's the twist: while countless artisanal miners and floating operations have extracted billions in gold directly from the waterway since the 1970s, nobody has ever considered exploring the river's historical pathways.

Canary Gold is pioneering this approach. Visible gold in six initial samples collected across a 2km area confirms their hypothesis. Will sufficient gold be discovered — in commercially viable concentrations — to transform even a small section of their 150,000-hectare property into a productive mine? Exploration will be inexpensive and rapid.

I'm enthusiastic about this narrative, but remember — this remains a preliminary exploration with substantial risk. It's not a flawless story, and I'll outline what I consider several challenges later in this article. HOWEVER. . .

. . . this opportunity revolves around scale, uncomplicated geology, and strategic positioning, centered in an area already proven globally as an alluvial gold producer — Brazil's Madeira River Basin.

Here's the detailed story:

A Generational Concept, Two-and-a-Half Decades in Development

This concept originated many years ago when three geologists were working in Brazil–Australian Jon Hill, British Alan Carter, and Canadian Andrew Lee Smith. These three individuals possess impressive geological credentials.

Hill, a geologist employed by AngloGold Ashanti, was assigned to evaluate Brazil's entire territory for gold potential. While major mining corporations disregarded alluvial-type deposits — considered too brief or unpredictable for multibillion-dollar operations — Hill recognized something different.

He identified scale. He recognized geological reasoning. And from these insights, he envisioned substantial gold potential.

Through eons of winding across the landscape, the Madeira River network has sculpted a 400 km-wide corridor through the Amazon Basin. It ranks among Brazil's most gold-abundant waterways. Approximately 7 million ounces of gold are believed to have been harvested from the Madeira River through artisanal methods. This doesn't account for unreported extraction or quantities lost to smuggling activities.

The Madeira River gold is so renowned that Parker Schnabel from the Discovery Channel's Parker's Trails featured it in an episode:

Now, envision all the locations where this river once flowed throughout the past several million years.

Imagine the gold deposited along those old riverbeds, now concealed beneath shallow layers of clay and soil.

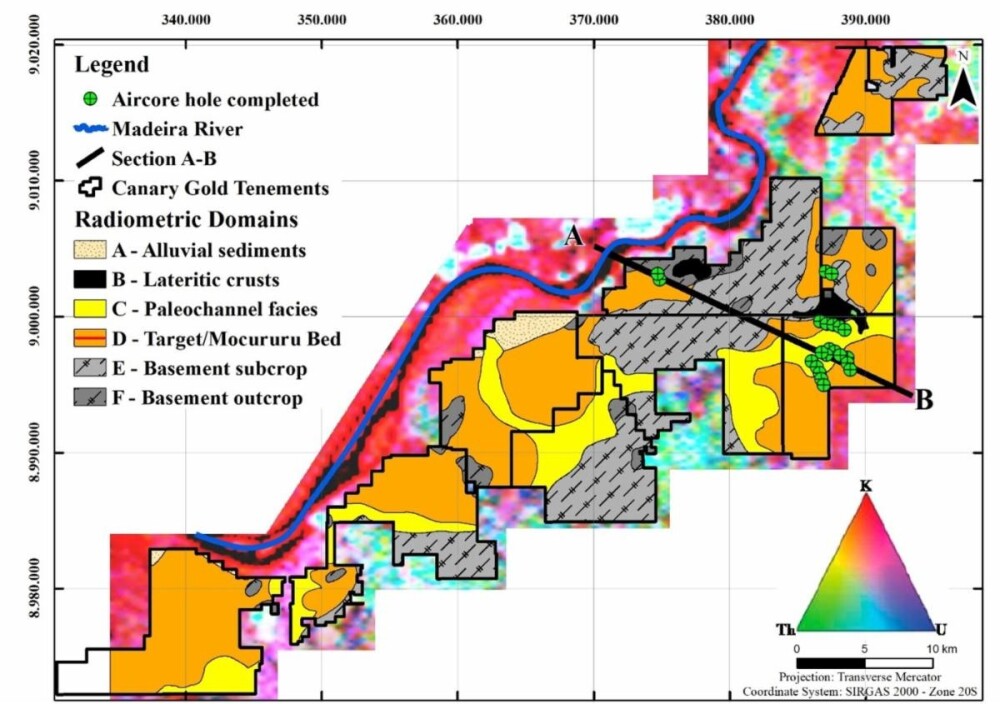

That's precisely what Canary Gold initially secured options on: nearly 700 square kilometers (69,000 hectares) across an 80 km stretch south of Porto Velho, Rondonia's capital city. This territory lies beyond the current riverbed but could overlay former gold-bearing channels — areas where the river previously flowed. That's the straightforward proposition here. They've subsequently added 90,000 hectares.

This isn't a Yukon-style, pan-and-sluice venture for placer gold. This represents placer gold at an industrial scale, utilizing advanced geophysics, proper permitting, and contemporary exploration technologies.

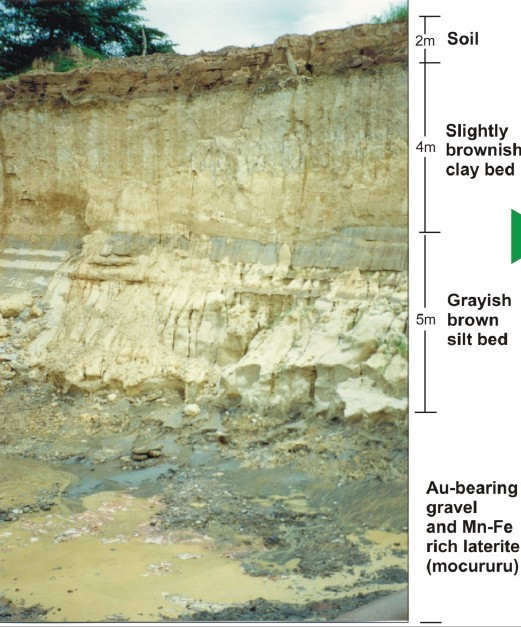

Canary's fundamental thesis centers on a consistent layer of mineralized laterite, locally termed Mocururu, which sits beneath 20–50 meters of overburden and contains visible gold and heavy minerals. This Mocururu horizon extends across substantial portions of their claims, verified through 15 km of tomography lines and GPR (ground-penetrating radar). The overburden itself — essentially compacted mud — frequently contains gold as well.

The Mocururu isn't solid rock. It's a consolidated sedimentary stratum, 2–5 meters thick, that would be comparatively simple to extract . . . if economically viable.

If Canary's hypothesis proves accurate and this layer consistently shows 0.5–1.0 g/t Au mineralization, they could potentially uncover a world-class deposit — at shallow depths of merely 30–60 meters.

They've discovered visible gold in six samples from their properties through basic manual panning. That's significant — powerful validation of their theory.

Straightforward Geology. Enormous Potential.

Canary's narrative excited me because of the team, and because it's founded on clear logic:

- Gold originated in the Andes.

- Rivers transported it eastward for millions of years.

- It was repeatedly deposited as the river shifted position over time–evidenced by over 7 million reported ounces recovered by Madeira River dredging operations over decades

- Most riverbed areas beyond current banks remain unexplored.

- Advanced technology now allows visualization of those ancient pathways using radar and resistivity equipment.

Additionally, it's near-surface.

These aren't deep, expensive drilling targets. Holes will likely average just 50 to 70 meters, sufficient for initial assessment. Drilling will utilize sonic equipment, which preserves sediment structure and enables complete recovery — crucial for gold contained in loose or partially consolidated layers.

This represents placer mining with contemporary tools — and potentially district-scale significance.

Scale: The Critical Differentiator

Canary has already mapped 30 kilometers of preserved paleo-channel features throughout its property — each potentially representing a corridor of ancient gold. The company believes an additional 20–30 kilometers of prospective channels await permit approvals.

While I wouldn't directly equate mining the Mocururu with conventional placer operations, certain placer technologies like gravity separators will be employed for testing and possibly extraction if economically viable gold concentrations are discovered.

Canary Gold's venture more accurately represents a paleo-placer deposit. Several significant and straightforward paleo-placer deposits exist, similar to Canary Gold's target.

Again, paleo-placer designates gold deposits formed through concentration in ancient riverbed systems and conglomerates. The world's largest gold deposit, South Africa's Witwatersrand, exemplifies this deposit type. However, it's older and consequently has fossilized into actual rock, situated much deeper with substantially higher grades.

Even if Canary Gold's Madeira River project realizes its full potential, grades here likely range from half a gram to one gram across 2-5 meters approximately. When discussing risks, this represents a significant consideration.

Investors would probably require results from about 50 drill holes before showing enthusiasm for such dimensions and grades. This approach is highly...unconventional. The market may require time to appreciate its scale. However, if successful, shallow, inexpensive drilling could make discovery costs per gold ounce EXTREMELY economical.

Again, that's the straightforward proposition. Perhaps it succeeds, perhaps not. It's early-stage.

The company has already discovered sufficient gold to validate their thesis — substantial gold exists underground throughout the Madeira River's historical paths across millions of years.

OK, this presents an exciting narrative–now for the (numerous) risks:

- HOWEVER . . . will it prove commercially viable? Yes, they've identified visible gold in several drill holes outlined thus far. But nothing yet demonstrates sufficient gold concentration to be economically feasible.

- They must invest $5 million to secure initial 49% ownership, then complete a PEA to reach 70%. Currently, they OWN NOTHING; they're earning interest through ground exploration expenditures. They'll need substantial capital raises as a high-risk exploration venture to reach 70% ownership. They must also compensate vendors of their recent acquisition with future payments.

- Considerable inexpensive stock exists. Standard founders' shares, vendors' stock, seed rounds (where I purchased $100,000 worth at 10 cents/share), the IPO priced at 17 cents including full warrants at 25 cents, and this latest financing at 25 cents with full warrants as well.

Nevertheless, I appreciate the potential scale here . . . AND . . . testing costs remain modest. I anticipate numerous exploration results between now and December–initially widely-spaced drill patterns across many kilometers–followed by tighter spacing if successful. At 70m depth, holes are inexpensive and quickly completed.

If successful, operations would resemble a moving quarry with concurrent backfilling as they extract the Mocururu, rather than conventional mining.

Finally, I'll leave you with background on these three individuals:

- Alan Carter is credited with involvement in five gold deposits, four located in Brazil; 6 years with BHP and 7 years with Rio Tinto before transitioning to CEO positions with exploration companies

- Andrew Lee Smith received Canada's Mining Entrepreneur of the Year award in 1994 for developing the Beaufor and Sleeping Giant mines

- Jon Hill ranks as Brazil's most sought-after independent exploration geologist, following his assignment to evaluate Brazil's entire territory for gold potential for AngloAshanti Brazil.

A 'Speculative Buy'

My friend John Newell of John Newell & Associates believes Canary Gold is a Speculative Buy. He shared the paragraph and chart below on Canary Gold:

"Canary Gold has recently completed a bullish breakout from a multi-month symmetrical triangle formation, confirming a significant shift in market sentiment. After months of consolidation between roughly CA$0.26 and CA$0.34, the stock pushed decisively through upper resistance in late September on expanding volume, often an early indication of institutional or informed accumulation. Following the breakout, the shares pulled back modestly to test the former resistance zone, now acting as support near CA$0.35, before resuming their advance. This retest strengthens the breakout's validity and sets the stage for a continuation move toward the next resistance levels. Momentum indicators support the bullish outlook. The MACD has crossed firmly into positive territory, and both moving averages are trending upward with increasing separation. The RSI, currently in the low-60s, remains constructive and shows room to advance before reaching overbought levels. Volume patterns reveal clear accumulation, confirming improved investor participation. The measured move from the triangle pattern projects an intermediate-term target near CA$0.60, while the broader structural base suggests a longer-term "big picture" target in the CA$0.75–CA$0.80 range, contingent on sustained volume and favorable sector tailwinds. Overall, the technical picture supports a Speculative Buy for traders and investors seeking exposure to early-stage momentum within the junior gold exploration sector. Continued strength above CA$0.35 would maintain this positive bias, while a close below that level would warrant short-term caution."

| Want to be the first to know about interesting Gold investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- Keith Schaefer: I, or members of my immediate household or family, own securities of: Canary Gold Corp. My company has a financial relationship with: None. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

- John Newell: I, or members of my immediate household or family, own securities of: None. My company has a financial relationship with: None. My company has purchased stocks mentioned in this article for my management clients: None. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

For additional disclosures, please click here.