I see strong medium and long-term potential in energy companies focused on oil, natural gas, uranium, and essential industrial metals like copper, nickel, zinc, platinum, and palladium, driven by both fundamental and technical factors. What stands out most prominently, though, is the significant disconnect between precious metals equity valuations and the performance of their underlying commodities. The market currently offers numerous undervalued opportunities across gold and silver companies, spanning from established producers to early-stage exploration ventures.

During my recent morning analysis of resource sector trends and evaluation of my portfolio's prospects for 2025, I found silver, gold, and uranium junior stocks particularly compelling. However, I'm struck by the puzzling disparity between current market valuations and the underlying strength of these companies, especially those demonstrating consistent value creation and positive development catalysts. After recent productive conversations with various management teams and thorough analysis, I continue to find the current valuations of junior gold, silver, and uranium stocks difficult to reconcile with their fundamentals.

Applying fundamental analysis to investments can be deeply frustrating when market prices move contrary to logical expectations. While this disconnect creates opportunities for profit through market inefficiencies, I'm mindful of Keynes's warning, "Markets can remain irrational longer than you can remain solvent.”

Unlike many investors who struggle to buy during market downturns, I consistently embrace opportunities to acquire high-quality companies at substantial discounts. If anything, my tendency is to build positions too early during market corrections.

The recent tax loss selling season has presented compelling opportunities in gold, silver, and uranium stocks, which have paradoxically declined even amid positive company developments. During my year-end portfolio rebalancing, I sold positions in underperforming companies where management failed to deliver on promises. These strategic sales offset my year's trading gains while generating capital for reinvestment in either existing holdings showing strong execution but lacking market recognition or turnaround stories still being judged by their past rather than their future potential.

As we often emphasize, past performance doesn't dictate future results, or, as Wayne Gretzky wisely noted, "Skate to where the puck is going, not where it has been."

Though I began drafting pieces on gold producers, copper developers, and uranium stocks, my attention kept returning to silver equities, particularly following my recent company interviews for the KE Report. I've learned to trust these intuitive pulls, which is why I'm focusing on silver stock opportunities now, despite plans to cover other sectors soon. The dramatic correction in silver stocks over the past two months presents a compelling investment case that demands immediate attention.

Let's examine the details. . .

Optimistic Despite Price

Industry experts across the energy, uranium, and copper sectors have been highlighting severe undervaluation in their respective stocks. Energy stocks have seen sharp declines, uranium stocks have corrected significantly over recent months, and copper juniors are particularly despondent about their second-half 2024 performance despite strong supply-demand fundamentals.

Interestingly, gold and silver junior company executives display notable resilience to the current downturn, having endured prolonged undervaluation. Their optimism is remarkable given the limited leverage they've seen despite strong precious metals performance through most of 2024.

While precious metals outperformed the elevated U.S. equity markets for much of the year, they retreated in the final two months. Though quality precious metals stocks saw substantial gains earlier, they relinquished much of these advances from October through December. Junior precious metals sentiment has deteriorated during tax loss season despite an overall positive year — typically an excellent accumulation opportunity.

In my discussions with junior silver producers and developers, they acknowledge recent poor share price performance with a mix of frustration and puzzlement at the intense selling pressure. However, they remain confident about their operational progress and upcoming 2025 catalysts. Their optimism at current $30 silver prices is notable, with widespread expectations of mid-to-high $30s or low $40s in the coming year.

The current $30 silver price, while down from October's $35 peak, remains significantly above the 2020 pandemic low of $11.77 or September 2022's $17.40. This represents a healthy price environment, despite retail investor pessimism. While management teams' optimism could be biased, fundamental and technical factors support silver spending more time in the $30s than $20s next year, with potential moves into the $40s.

Dolly Varden

I recently spoke with Shawn Khunkhun, President and CEO of Dolly Varden Silver Corp. (DV:TSX.V; DOLLF:OTCQX), about their 2024 achievements and upcoming 2025 catalysts at their Kitsault Valley Project in British Columbia's Golden Triangle.

During our pre-recording conversation, Shaun expressed genuine enthusiasm for 2025 and satisfaction with their 2024 achievements despite their stock's dramatic decline from $1.46 in mid-October (when silver peaked above $35) to $0.86 last week (as silver dipped below $30) - a 41% drop since our last meeting in Fort Lauderdale.

As a Dolly Varden shareholder sitting on healthy gains, I hadn't fully grasped the severity of this recent correction until he mentioned it. The magnitude was particularly shocking given their consistent stream of positive news.

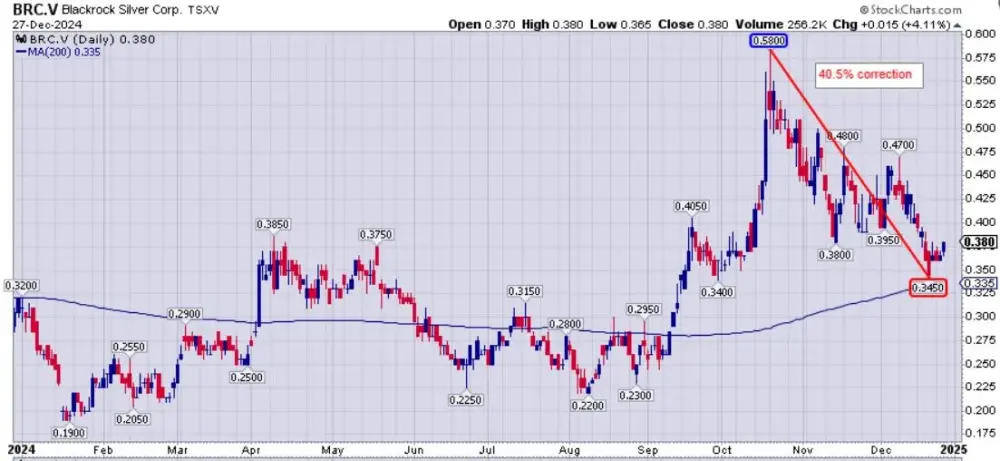

Blackrock Silver

After this revelation, I began reviewing other silver stocks in my portfolio to assess the extent of the recent downturn.

In this context, I also recently spoke with Andrew Pollard, President and CEO of Blackrock Silver Corp. (BRC:TSX.V; BKRRF:OTCQX), who shared their 2024 accomplishments and upcoming growth initiatives for their wholly-owned Tonopah West Project in Nevada.

Blackrock Silver reported positive developments in recent months, including high-grade results from their extensive 22,000-meter M&I conversion and expansion drilling program in 2024, showing both resource growth and grade improvements.

Yet their stock price plummeted by over 40%, dropping from October's peak of $0.58 to $0.345 last week. This severe decline, mirroring the pattern in other silver stocks, seems disconnected from their strong operational performance. While silver's 14% decrease from $35 to $30 during this period is significant, the magnitude of these share price declines appears excessive for advanced explorers successfully executing their development plans.

AbraSilver

Looking to see if this pattern extended beyond a few cases, I examined AbraSilver Resource Corp. (ABRA: TSX.V; ABBRF:OTCQX) another prominent advanced silver explorer.

In my December 3 conversation with John Miniotis, President and CEO, and Jeremy Weyland, Senior VP of Projects and Development of AbraSilver Resource Corp, we discussed their updated Pre-Feasibility Study for the Diablillos silver-gold project in Argentina's Salta Province. The study showed markedly improved economics after incorporating the new RIGI law incentives - undoubtedly positive news for the company.

As a long-term AbraSilver shareholder, I hadn't fully registered the extent of the recent decline, as my position remained profitable, just less so. The revelation that their stock had plunged 37.4% from October's peak of $3.58 to last week's low of $2.24 was startling, especially considering their recent positive drill results and enhanced PFS economics. This continued the worrying pattern emerging across the silver sector.

Silver Tiger

Reviewing my portfolio and past conversations, I recalled my early November KE Report discussion with Glenn Jessome, CEO of Silver Tiger Metals Inc. (SLVR:TSX.V; SLVTF:OTCMKTS), about their El Tigre Project's open-pit PFS. Our conversation covered their upcoming underground PEA targeted for H1 2025 and Mexico's recent positive political shifts that could streamline mining permits.

Their positive open-pit PFS, upcoming underground drilling program for the PEA, and Mexico's improving political climate for mining permits should have supported the stock price. Instead, Silver Tiger plunged 43.6% from $0.355 in October to $0.20 last week — a decline far exceeding silver's 14% pullback. This disconnect between fundamentals and market reaction defies logic but reflects our current market environment.

Santacruz Silver

Similar excessive declines are evident across other quality silver explorers like Discovery Silver Corp. (OTCMKTS:DSVSF), Vizsla Silver Corp. (VZLA:TSX.V; VZLA:NYSE), GoGold Resources Inc. (GGD:TSX), Aftermath Silver Ltd. (AAG:TSX.V; AAGFF:OTCQX; FLM1:FRA), and Defiance Silver Corp. (DEF:TSX.V; DNCVF:OTCBB) — all experiencing sharp selloffs despite positive developments.

Initially, I wondered if this selling pressure was limited to pre-revenue companies. However, examining producing companies revealed equally severe declines. This became clear in my late November discussion with Arturo Préstamo Elizondo, CEO of Santacruz Silver Mining Ltd. (SCZ:TSX.V; SZSMF:OTCQX; 1SZ:FSE), reviewing their Q3 2024 results from their Mexican mine and substantial Bolivian operations, including five mines, three mills, and their metals trading business.

Santacruz's Q3 2024 results showed impressive mid-tier production of 4.64M silver equivalent ounces, with a 2% increase in silver output from Q2. Despite producing more silver equivalent ounces than Silvercrest, Gatos Silver, Aya Gold, and Silver, or Endeavor Silver, Santacruz trades at just 5-10% of their valuations.

Their Q3 financials demonstrated remarkable growth: 21% revenue increase, 242% adjusted EBITDA growth, and a 505% increase in cash position year-over-year. CEO Arturo expressed even greater optimism for Q4 results.

Despite these strong fundamentals, the stock plummeted 43% from October's peak of $0.45 to December lows of $0.255.

Avino Silver & Gold

During our mid-November discussion at the New Orleans Investment Conference, Nathan Harte, CFO of Avino Silver & Gold Mines Ltd. (ASM:TSX.V; ASM:NYSE.MKT; GV6:FSE), shared their Q3 2024 results and outlined their strategic plan to become an intermediate Mexican silver producer through the development of the La Preciosa and Tailings Projects over the next five years.

Nathan highlighted their strong financial performance with current commodity prices, reporting a 13% production increase and 19% revenue growth from Q3 2023 while expressing optimism about Q4. Yet despite these positive indicators, ASM's stock dropped 43% from October's $1.56 peak to $0.89 — a puzzling market response to solid fundamentals.

Sierra Madre Gold and Silver

This market reaction defies logic — a 14% drop in silver price doesn't justify halving company valuations in two months. The Q3 results don't even reflect peak silver prices from Q4, making the selloff even more irrational. It appears to be pure sentiment-driven selling.

In my recent conversation with Alex Langer, CEO of Sierra Madre Gold and Silver Ltd. (SM:TSX.V; SMDRF:OTCQX), we discussed their milestone achievement: the start of industrial production at La Guitarra Mine, with commercial production targeted for Q1 2025. Despite this significant news and other positive developments, the market has remained unresponsive.

La Guitarra, a previously producing underground mine with a 500 t/d processing facility operated by First Majestic until 2018, was acquired by Sierra Madre in 2023. After beginning test mining in June 2024, the plant has exceeded commercial production standards by operating at 86% capacity (516 tonnes daily) for two months — well above the 80% threshold needed for industrial production status.

Typically, this pre-production phase brings share price appreciation as companies approach commercial production. Instead, Sierra Madre's stock dropped 27.5% from October's $0.70 to December's $0.425, caught in the broader silver sector decline despite hitting key operational milestones.

Guanajuato Silver

In my December 3 discussion with James Anderson, CEO of Guanajuato Silver Co. (GSVR:TSX.V; GSVRF:OTCQX), we reviewed their Q3 performance and operational updates across their extensive Mexican portfolio of five silver-gold mines and three processing facilities. The conversation covered developments at multiple sites: exploration at Pinguico and Valenciana, new filter presses at Topia, El Cubo's upcoming resource estimate and mill optimization, and the San Ignacio Mine's ore sorter commissioning.

James reported decreasing costs, improved silver production, and loan repayments, with two of their three production loans now cleared. Their El Cubo resource update showed a strategic transition — while measured and indicated resources decreased 23% after three years of mining, inferred resources surged 85% to 35.6M silver-equivalent ounces, with inferred tonnage up 179%. Despite these improvements, the stock followed the sector's pattern of steep declines.

The market's response to Guanajuato's operational improvements—- lower costs, debt reduction, and significant resource expansion -—was a 47.6% decline from October's $0.315 to $0.165 last week. This severe drop contradicts rational market behavior.

From a technical standpoint, silver juniors have declined roughly 40% in two months, breaking below their 200-day moving averages — a bearish signal that may keep conservative and momentum investors sidelined until prices recover above this level. While continued weakness is possible, it seems increasingly unlikely.

Despite waves of positive news and fundamental improvements across companies, valuations have been slashed. However, Q1 historically brings strength to precious metals stocks, particularly January-February, though last year proved an exception.

Eventually, solid operational execution — good drill results, expanding resources, and improving production metrics — should attract sophisticated investors and analysts. This recognition typically leads to price improvements that then draw momentum from traders.

While I can't provide investment advice, I've been accumulating during this disconnect between valuations and fundamentals, and I plan to continue as long as this gap persists.

| Want to be the first to know about interesting Silver investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Important Disclosures:

- [COMPANY] is a billboard sponsor of Streetwise Reports and pays SWR a monthly sponsorship fee between US$4,000 and US$5,000. In addition, [COMPANY] has a consulting relationship with Street Smart an affiliate of Streetwise Reports. Street Smart Clients pay a monthly consulting fee between US$8,000 and US$20,000.

- As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of [COMPANY].

- [PERSON_NAME]: I, or members of my immediate household or family, own securities of: [COMPANY]. I personally am, or members of my immediate household or family are, paid by [COMPANY]. My company has a financial relationship with [COMPANY]. I determined which companies would be included in this article based on my research and understanding of the sector.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports, Street Smart, or their officers. The author is wholly responsible for the accuracy of the statements. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Any disclosures from the author can be found below. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

- This article does not constitute investment advice and is not a solicitation for any investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Each reader is encouraged to consult with his or her personal financial adviser and perform their own comprehensive investment research. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company.

- This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

For additional disclosures, please click here.