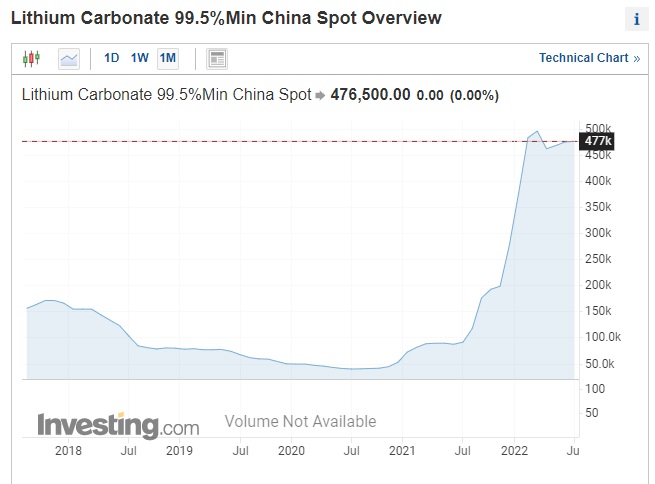

In a time with record inflation, the Russia-Ukraine conflict advancing into a decisive phase as the Ukraine is almost completely shut off from the Black Sea now, with even Odessa under missile attack despite a transport/trading agreement on grain exports, the lithium product prices keep hovering at staggering heights, with spot pricing for lithium carbonate still near the 500,000 yuan per tonne, or US$75,000 per tonne. The chart below is from Investing.com:

Unfortunately negative stock market sentiment, caused by worries about the U.S. Federal Reserve interest rate hike policies (recently acting with a forecasted 0.75% hike, and a promise of more to come) and related recession fears don’t have the most positive effect on junior mining stocks at the moment, lithium juniors included. Notwithstanding, the paradigm shift to renewable energy is in full swing and can’t be stopped, causing increasing demand for everything battery-related including metals like lithium and nickel. Argentina Lithium & Energy Corp. (LIT:TSX.V; PNXLF:OTC; OAY3:FSE) doesn’t seem to wait until the tide turns, and after raising almost CA$6M in an oversubscribed financing at the beginning of this year, it is proceeding with drilling its new flagship Rincon West Project, and expanding its claim holdings. Rincon is an interesting area, as not too long ago Rincon Mining, a private company constructing an adjacent brine project at the same salar, and owned by Sentient Equity Partners, was acquired for US$825M by Rio Tinto Plc (RIO:NYSE: RIO:LSE; RIO:ASX; RTPPF:OTCPK).

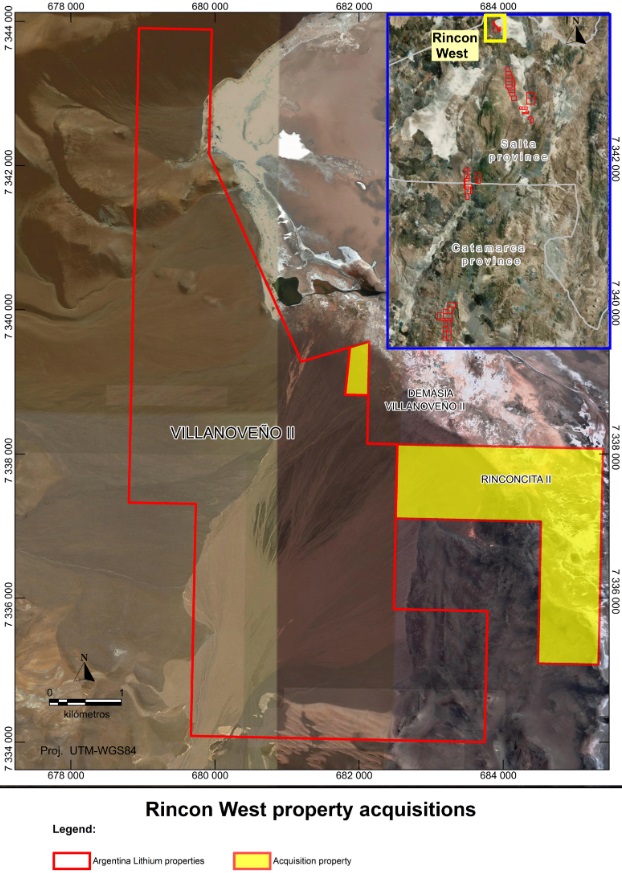

On July 21, 2022, Argentina Lithium announced that it won the public tender to purchase the Rinconcita II mining concession, located on the Salar de Rincon in Salta Province, Argentina. With the concession, the company has added another 460.5 hectares of salt flat properties, adjacent to not just the already owned 2,470-hectare Rincon West project, but also next to the aforementioned Rincon project acquired by Rio Tinto. The new claims can be seen on the following map:

No exploration work has been done at Rinconcita II in the past. Argentina Lithium also mentioned the acquisition of the 20.5-hectare Demasia Villanoveno II concession, through applications presented at the Salta mining authority, representing part of the original Rincon West claim package.

As part of the Rinconcita II acquisition, Argentina Lithium will make an initial payment of US$2.5 million (US$2.5M) upon signing the agreement. It also grants a 3% NSR to the vendor when it advances to the production stage, and the company must present a proposed exploration program for approval.

Argentina Lithium already owned 15,857 hectares of properties on the west side of the Pocitos Salar, and it acquired 10,364 hectares of new properties at Pocitos in January. The total cash consideration was US$2.6M — with US$285k in mandatory payments for the first year — and about CA$850k in shares.

As a reminder, the two main lithium properties, Rincon West and Pocitos, with a combined footprint of 18,227 hectares, were acquired in October 2021. At that time, the company issued 750,000 shares to the vendor on signing, plus CA$500,000 worth of shares over a 12-month period; and cash payments totalling US$4.2M over 36 months, but limited to only US$1.05M in the first 18 months, US$800,000 of which are firm commitments over the first year. Therefore, total commitments for the first year for Rincon West and Pocitos increase to US$1.085M.

I recently asked Argentina Lithium CEO Nikolaos Cacos about how permitting was advancing at Pocitos and what kind of exploration programs, including drilling, should be expected.

“With our recent acquisitions, we have reassigned project priorities. Our primary focus is to define high-grade resources adjacent to major players on the proven salars of Rincon and Antofalla. Pocitos is a huge, underexplored lithium salar. We like the setting and the huge up-side potential, but Pocitos is an early stage exploration project. It will take its place lower in our project pipeline,” Cacos answered.

Since the nearby Rincon Lithium Project of Argosy Minerals Ltd. (AGY:ASX) in eastern Rincon has an average grade of 321milligrams per liter lithium (mg/l Li), and the grade of the part of the Salar de Rincon that hosts Rio Tinto's Rincon Mining is 397 mg/l Li, I expected the assay grades for Argentina Lithium's new drill program at Rincon West (which started in late May and is expected to last 5 months) to be over 300 mg/l Li.

As the company announced the results of the first drill hole on July 13, this was a good opportunity to verify expectations. It turned out that a 70-meter-thick drilled interval returned lithium grades varying from 225 to 380 mg/l Li, so on average the 300 mg/l Li threshold seems to be met here. It was good to see Argentina Lithium assaying economic lithium grades right away, as indicated aquifers don’t automatically mean sufficient lithium mineralization.

Vice-President of Exploration Miles Rideout was also pleased with the results.

"The first hole at Rincon West has revealed a permeable 70-meter interval with moderate to high-grade lithium values. This validates our belief that the concentrated lithium brines mapped in the adjacent resources does extend beneath our property. We are continuing our exploration drilling to delineate this mineralization with the aim of defining a mineral resource," Rideout said.

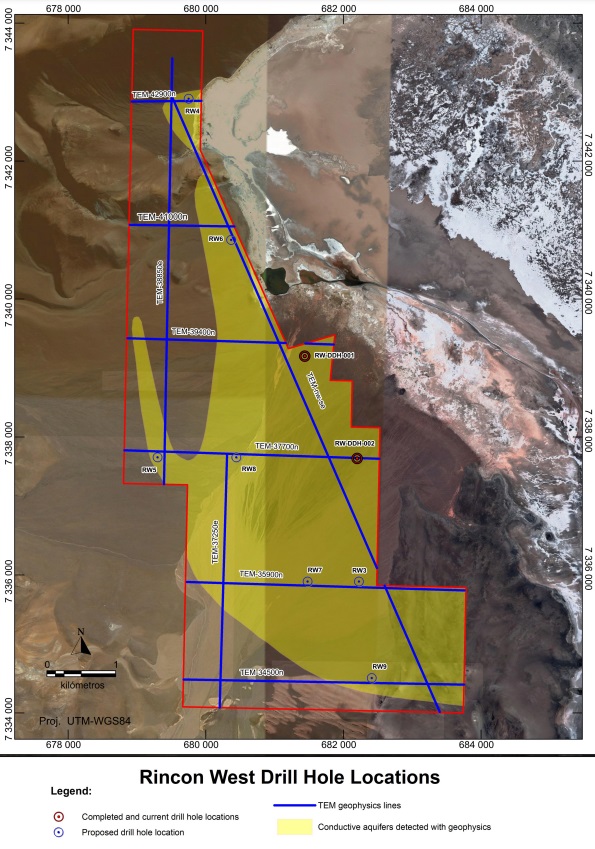

A second drill hole is in progress, and up to seven others are planned with at least four more being drilled this summer, all of them can be seen on the following map:

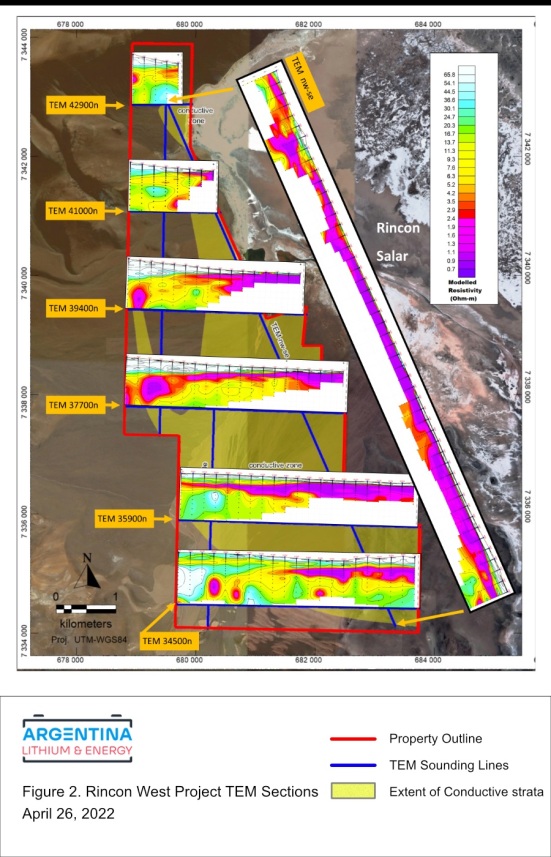

The yellow zones on the map above indicate conductive aquifers, defined by the TEM surveys completed in March and April this year. These conductive aquifers are targets for drilling as they could contain concentrated lithium brines. Cross-sections based on the TEM survey can be seen here, with the purple zones indicating conductive zones (potential brines):

As can be seen, the conductive zone extends for about 12 kilometers representing significant potential brine volume.

All diamond drill holes will be drilled vertically, and the first drill hole was stopped in basement rocks at 300 meters depth below surface. Looking for brines you ideally hope for aquifers stretching 200-300 meters deep, but since the strike-length appears to be 12 kilometers, sheer size could provide sufficient volume here. So I wondered about the average thickness of the adjacent Salar de Rincon project, now owned by Rio Tinto.

“More than 90% of the historic drilling by neighbouring companies has tested to 100 meters depth or less. High-grade resource at shallow levels is an attractive feature of this basin, but we believe continued exploration will also produce positive results from deeper levels,” Cacos explained.

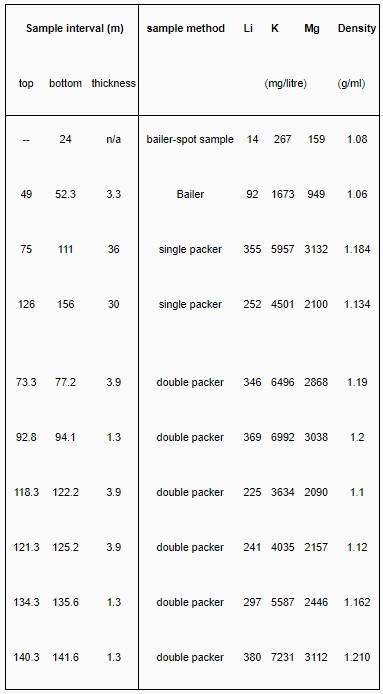

The full results of the first drill hole RW-DDH-001 can be observed in this table:

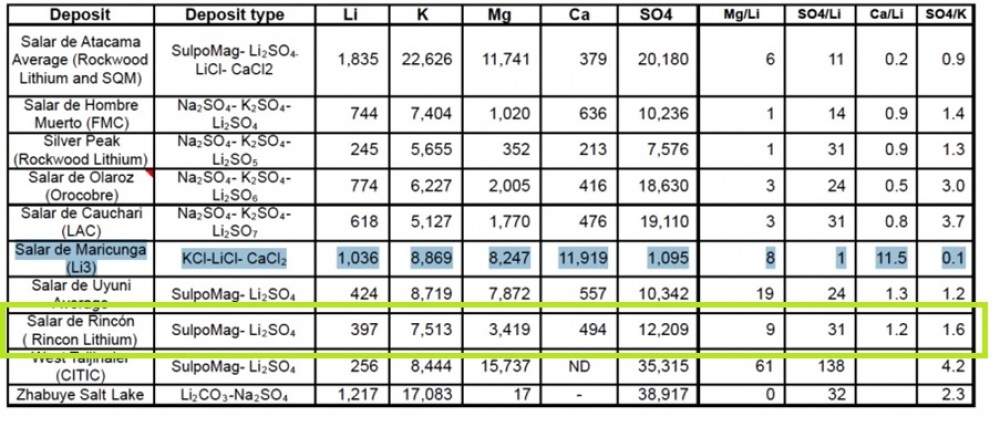

There are more penalty elements in brine than shown above, and the most important ones can be seen in this table, also including the Salar de Rincon:

As can be seen, the average grade of the first drill hole is somewhat lower on all elements tested, compared to the Salar de Rincon itself. I asked CEO Cacos if this is what he expected, what he wanted and what he is looking for in the upcoming drill holes. He answered ”Our first hole produced extremely positive results, demonstrating we have brines that are approximately comparable to the published resources on the salar. This was our expectation. Ongoing drilling is intended to define the property’s potential and to provide the data for our resource calculation. I think the discovery hole was a great beginning.”

Located to the south of Salar de Rincon, the Pocitos Project was acquired together with the Rincon West property. Exploration plans for Pocitos involve 121 kilometers of TEM soundings in Q1, 2023, and as such is a lower priority exploration play for Argentina Lithium. According to Cacos, these exploration plans have been adjusted following recent property acquisitions.

A new high priority for Argentina Lithium is its Antofalla North Project. The company expanded its Antofalla North project by acquiring 5,411ha in April, 2022 for a total of 14,987ha. The project is located approximately 25 km west of Argentina's largest lithium producing operation at Salar de Hombre Muerto. The Salar de Antofalla is over 130 km long and varies between 5 km and 10 km in width, with reported basin depths exceeding 500 m. The terms of the option agreement to own 100% include cash payments totaling US$2.8M over 4 years, C$7M in exploration expenditure commitments, and the vendor retains a 2% NSR, repurchasable for US$3M.

The Antofalla acquisitions are particularly notable since Albemarle, the world’s largest producer of lithium for electric vehicle battery production, has focused its salar property acquisitions in this basin and has a published high-grade resource.

Albemarle’s project begins approximately 500 meters south of Argentina Lithium’s holdings. The current exploration plan for the Antofalla North project involves 110 km of TEM soundings, followed by an estimated six diamond drill holes.

“Our drill permitting process is well advanced for Antofalla North, which extends between two provinces, requiring two submissions. We expect to complete our geophysical surveys in the fourth quarter, and to begin drilling early in 2023,” Cacos said.

Looking at it from a distance, the company has a considerable quantity of projects in its portfolio and thus significant annual financial obligations. I wondered why the company acquired and optioned so many projects, as it is draining the treasury of a few million dollars annually just on property acquisitions and obligations, which is money that can’t go in the ground — not to mention diluting the share structure.

There is only so much you can explore and drill each year. Wouldn’t it be better to focus more on one or two best projects, and divest the others asap? The company appears to have burned through almost CA$2M since December 2021, without doing much drilling and just TEM surveys, as it is contemplating a new CA$2.5M at $0.20 financing at the moment.

Cacos answered my questions with the following extensive explanation: “This was a strategic decision, also please note we still have CA$4M in the treasury, but have the opportunity to raise more. We saw the opportunities to acquire the large blocks at Rincon and Antofalla, strategically located beside major resources. We recognized that these opportunities are unlikely to be repeated. Our team has the depth of experience to manage this ambitious portfolio effectively. A point that might not be obvious is that all our properties already have all-weather roads and nearby towns and infrastructure. In each case, we can move quickly to advanced geophysical imaging of brine deposits and drill testing, which will reduce our exploration time and cost. This benefit doesn’t come cheaply, but pays dividends through the entire life of the projects. In short, we prefer to invest in large, high prospectivity projects, rather than conceding property quality to other concerns.”

I like the concept of going for large quality claim blocks, as it increases chances of success. The flip side is you have to finance holding costs and exploration. If funding is no issue, it is indeed the best strategy to follow, at least in my view. So far so good. Investors seem to wait for results, and a turning of the markets:

As usually happens in a bear market, lots of stocks become as cheap or even cheaper compared to the period just before a bear market, although the asset value could have increased nonetheless. In this case Argentina Lithium acquired more claims at the various projects, conducted several surveys and started drilling at Rincon West, with other drilling coming up, and lithium product prices went ballistic again a few months ago, more than doubling since March. Therefore I’m not entirely convinced that the current low share price really displays the intrinsic value of Argentina Lithium at the moment.

Conclusion

Argentina Lithium maintains a buying spree, although it already has an impressive land package, spread over four different lithium salar projects in Argentina, part of the Lithium Triangle. This is done because management places highest priority on property quality and scale. At the same time, the company is executing its exploration plan of geophysical imaging followed by drilling of conductive targets. Initial drill results at Rincon West confirmed grades almost similar to the adjacent Rincon Project, which was recently acquired by Rio Tinto for US$825M. At least four more holes are being drilled this summer, and I’m curious if the upcoming results will show a brine field of economic proportions and grade. With a giant like Rio Tinto owning the adjacent project, there already seems to be a natural suitor with deep pockets at their doorstep.

All pictures are company material, unless stated otherwise.

All currencies are in US Dollars, unless stated otherwise.

Disclaimer

The author is not a registered investment advisor, and currently has a long position in this stock. Gold Terra Resource is a sponsoring company. All facts are to be checked by the reader. For more information go to www.goldterracorp.com and read the company’s profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence and talk to their own licensed investment advisors prior to making any investment decisions.

All pictures are company material, unless stated otherwise.

All currencies are in US Dollars, unless stated otherwise.

Please note: the views, opinions, estimates, forecasts or predictions regarding Gold Terra’s resource potential are those of the author alone and do not represent views, opinions, estimates, forecasts or predictions of Gold Terra or Gold Terra’s management. Gold Terra has not in any way endorsed the views, opinions, estimates, forecasts or predictions provided by the author.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high-quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long-term commodity pricing/market sentiments, and often looking for long-term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

| Want to be the first to know about interesting Cobalt / Lithium / Manganese investment ideas? Sign up to receive the FREE Streetwise Reports' newsletter. | Subscribe |

Streetwise Reports Disclosures

1) The Critical Investor's disclosures are listed above.

2) The following companies mentioned in the article are sponsors of Streetwise Reports: Argentina Lithium and Energy Corp. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Argentina Lithium and Energy Corp., a company mentioned in this article.