This is the third article I’ve written on Arianne Phosphate Inc. (DAN:TSX.V; DRRSF:OTCQB; JE9N:FSE). I believe this story has near-term catalysts and key investment attributes that investors may not be appreciating.

A significant corporate development was recently announced. It was revealed that, “several battery industry participants” have been working with Arianne (for months) on high-purity concentrate derived from phosphate rock sourced at its 100%-owned Lac à Paul project in Québec, Canada.

In the press release, it said test work on its phosphate concentrate is being done under the auspices of an agreement with a “major battery producer.” This could mean that a top battery maker valued in CA$10s to CA$100s of billions is considering signing a major off-take agreement.

“Arianne’s high-purity phosphate is ideal for meeting growing demand for phosphate as it’s ideally suited for applications of all kinds; from fertilizers to advanced energy applications,“ the company said. “As the project is located in Québec, it responds to the concerns of buyers regarding security of supply; a problem that continues to affect the world’s phosphate markets.”

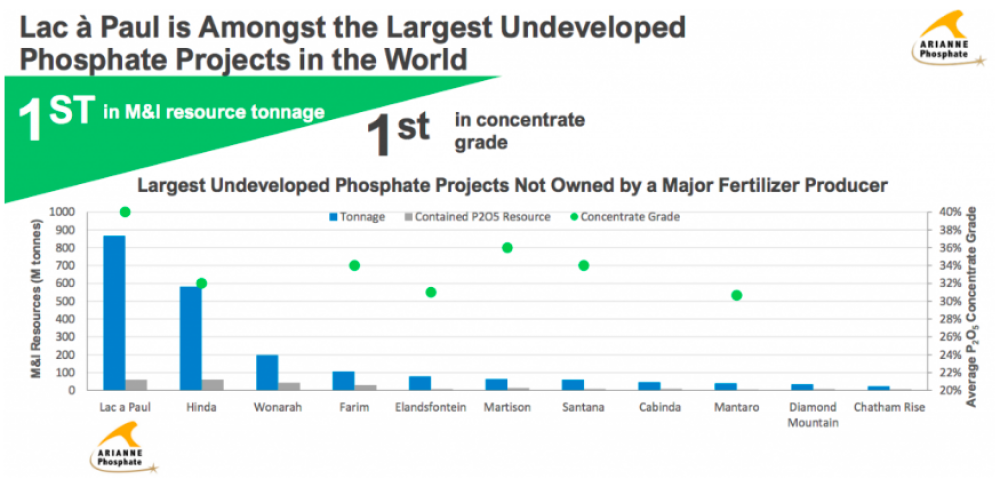

This announcement alerted every battery industry participant and fertilizer end user that a very substantial source of the phosphate is up for grabs. There are few (if any) phosphate rock projects with the combination of size plus concentrate grade of Lac à Paul.

Instead of six or eight global fertilizer/Ag companies potentially interested in partnering with, obtaining off-take from, or acquiring all of Lac à Paul, there are now a handful of battery firms and perhaps auto OEMs in the hunt. Talk about competitive tension, it just went through the roof.

Arianne has two off-take arrangements, a fully permitted project, and a signed Cooperation Agreement with the Innu First Nations. This is a shovel-ready project that could be in production within three years.

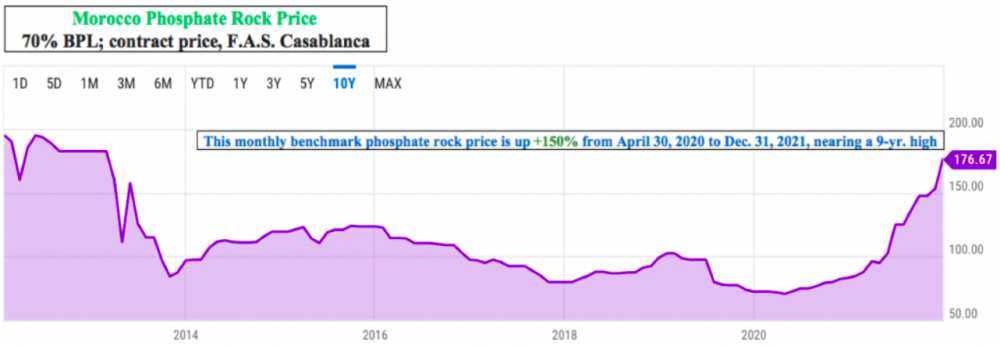

Readers might be wondering why Arianne’s project has been slow to advance since its 2013 Feasibility Study. A big part of the answer is that the study was done soon after multiple years of elevated phosphate rock prices. In 2011-2012, the average month-end price was $174 a ton. Thereafter, the average price fell every year from 2013-2019.

By the Spring of 2020, phosphate rock (along with many other commodities) began marching higher. Now it’s near a nine-yr. high, up 150% to $176.67 a ton on Dec. 31, 2021, from $70.75 a ton on April 30, 2020.

For six months (October 2008 to March 02009), the Moroccan phosphate price was $450 a ton. Adjusted for inflation, that’s $585 a ton today.

Until a few years ago, the paradigm shift to LFP batteries barely existed. Imagine the possibilities for Arianne’s phosphate concentrate pricing. Not only are benchmark prices soaring due to growing fertilizer demand, global inflation and high energy prices — add to that 25% long-term annual growth for LFP batteries.

Compare phosphate prices at $235 a ton to lithium, nickel and cobalt prices in the $10,000s/t. Battery companies, especially those with plants in North America, can easily afford to pay a 5% to 10% premium to lock in reliable, high-purity phosphate concentrate from Canada. (Note: There’s no indication yet that a premium price would be received)

Astute readers may be thinking that demand for phosphate in electric vehicles will not move the needle on price because the phosphate rock market is ~222 million tonnes per year. Phosphate tonnage earmarked for LPF batteries is estimated to be ~5% of the overall market by 2031; ~13 million tonnes per year.

However, not all phosphate rock is amenable to the high-purity standards of EV batteries. Only a fraction of the 222 million tonnes per year market will qualify. Arianne states in the press release, “A very significant amount of its projected 3 million tonnes of annual output” could potentially be sold into higher-value applications.

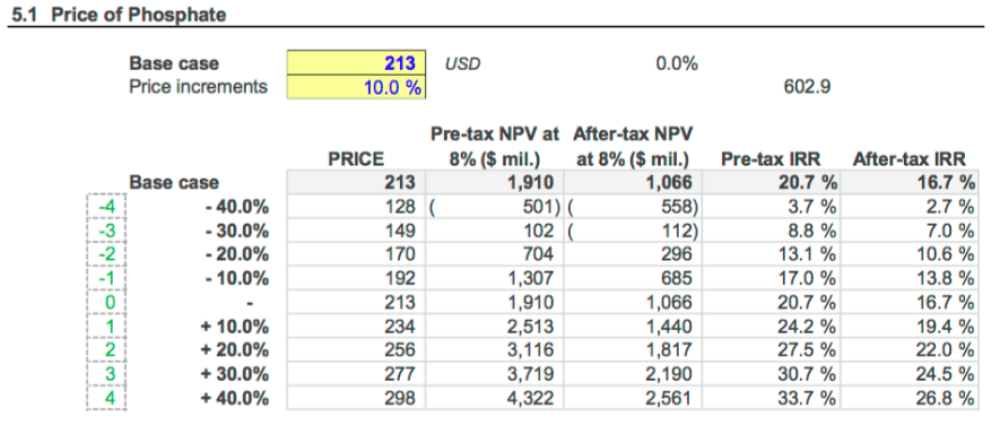

Readers are reminded that the 2013 FS used a $213 per ton price for 100% fertilizer-grade material. Today, management believes its high-grade phosphate rock might fetch ~$235 per ton.

Each $1.00 per ton change in the phosphate price equals ~$17.5 million in after-tax NPV (8%), so a $235 per ton price adds $385 million to the NPV.

Over a 12-month period in 2011-2012, the average benchmark price was ~$230 per ton (adjusted for inflation), ~30% higher than the current price of $176.67 per ton. If the benchmark index returns to $230 per ton, that would imply a price for Arianne’s product of ~$300 per ton.

In the chart of NPV and IRR sensitivities from Arianne’s FS, one can see that at a realized price of $298 per ton, the after-tax NPV = $2.561 billion = CA$3.27 billion. Compare that to the company’s Enterprise Value (market cap + debt – cash) of ~CA$118 million.

Arianne is trading at ~4% of its pro forma after-tax NPV (8%) — at today’s phosphate prices — and ~11% of the base case NPV. This is absurdly cheap compared to similar-stage, world-class natural resource projects.

For example, Skeena Resources’ (PFS-stage) gold project, Nexgen Energy’s (PFS) uranium project, Nouveau Monde’s (BFS/DFS) graphite project, and Neo Lithium’s (BFS/DFS) lithium project trade at between ~62% to ~78% of their after-tax NPV (8%).

It should be noted that since 2013, the CA$/US$ exchange rate has moved ~15% in favor of Arianne’s project AND work done subsequent to the BFS/DFS shows op-ex can potentially be lowered by ~15%. These considerable enhancements are not included in the comparisons.

I argue that Arianne Phosphate is more advanced than its peers because it already has 1) two off-takes in place, 2) a signed agreement with First Nations, 3) ALL permits issued — the project is shovel-ready, and 4) ample regional infrastructure available in a Tier-1 jurisdiction.

Québec Canada is one of the best locations in the world to develop and operate a mine. Management is having discussions with banks, equity providers, equipment financing lenders, and royalty/streaming parties to provide up to 75% to 80% of the upfront capital needed to reach commercial production.

Securing new off-takes, and/or landing a strategic partner could happen at any time, but this year seems reasonable to me. Arranging a funding package should be this year’s business as well. These major achievements could propel the share price much higher, especially if the phosphate rock price continues to climb.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University's Stern School of Business.

Disclosures / Disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Arianne Phosphate, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Arianne Phosphate are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Arianne Phosphate was an advertiser on [ER] and Peter Epstein owned shares in the Company.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure:

1) Peter Epstein's disclosures are listed above.

2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.