Maurice Jackson: Joining us for a conversation is David Cole, the CEO of EMX Royalty Corp. (EMX:TSX.V; EMX:NYSE.American), the Royalty Generator.

It's always a pleasure to speak with you, sir, to get the latest exciting developments from EMX Royalty. Before we begin, Mr. Cole, please introduce us to EMX Royalty and the opportunity the company presents to shareholders.

David Cole: EMX Royalty, we're the most prolific royalty generator on the planet. We acquire prospective mineral rights around the world, utilizing our alpha which is economic geologic talent. We add value by building geologic models illustrating prospectiveness, and sell those assets to an industry hungry for discovery opportunity for a combination of cash, shares, annual payments, work commitments, and, always, a royalty on the back end.

We've been doing this business model successfully now for nearly 18 years, accumulating a large portfolio of mineral real estate assets around the world. To augment the portfolio, we grow organically through that bread and butter process. We also buy royalties, which is a difficult business, which speaks to the value of royalties. They're phenomenal financial instruments, but we do occasionally find royalties to buy, to add to our portfolio.

And the third thing that we've done very successfully is make strategic investments; those are share placements into public and/or private companies where we commonly follow that investment with intellectual talent as well that adds value and then liquidate it over time. And our strategic investing track record throughout the history of the company is fantastic, and that's why we're in a very strong cash position today.

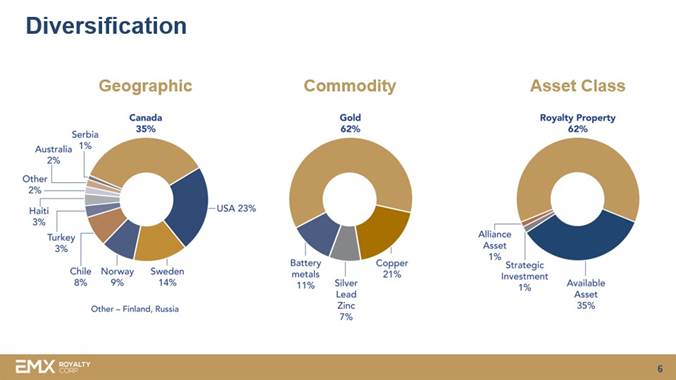

So we're sitting here today with nearly 300 mineral property assets worldwide, close to US$40 million in cash, close to $20 million or perhaps a tad more in tradable securities and long-term investments within the portfolio, giving us nearly as much cash and investments and tradable securities as we have raised in the entire history of the company, in addition to our mineral property assets that span the globe, and, of course, we have no debt.

Maurice Jackson: For all of the virtues that you've just conveyed here today, I'm on record. I've said it in previous interviews, I plan to match my bullion purchases with the shares in EMX Royalty.

David Cole: We appreciate that.

Maurice Jackson: I believe that the stock has the potential to melt up, and that's not just my opinion. I have a Rolodex of names, some of those are the most respected names in the industry, and we are all aligned with the value proposition of EMX Royalty in that regard.

Sir, EMX Royalty has some important updates for shareholders. Let's begin in Serbia. Mr. Cole, take us along the Bor mining district and the Timok property, which is owned by Zijin Mining, which is quickly becoming one of the world's biggest ongoing copper-gold discoveries in the past decade. Last week, Zijin provided some exciting news on the upper zone. What are the latest developments that you can share with us?

David Cole: So, this is an excellent example of how our business model has worked over the long term for EMX. It was one of our first business units in the company when we were a private company operating in Serbia, originally called Southern European Exploration. We were focused on this business model and acquiring assets in Serbia. We ended up adding value to those and selling them off part and parcel to our business model for cash shares and royalties and that company, which we sold to Reservoir Minerals, made a huge discovery with our joint venture partner Freeport, and as luck would have it, it was just off the boundary of our royalty.

But we had our ear to the railroad track. We knew what was going on there. And so we were able to quickly go out and buy the royalty that did exist that was held by another company over that discovery for a price of $200,000 Canadian early on in the discovery history before it was fully understood what the minimal potential was there.

Keep in mind that the Bor District is Europe's largest historical copper and gold producing region and has some incredible geology. It's a magmatic complex with copper and gold deposits spread along the strike length of that complex.

Reservoir Minerals ended up making a very large discovery there. That discovery was ultimately sold to Zijing Mining, which is advancing the Timok Project very quickly, part and parcel to a half a billion-dollar investment into the ground there and a letter of understanding with the Serbian government. And my understanding is that mine will be commissioned within the coming days.

We've been told they're throwing a party there for the commissioning. We're very excited about that. We do hold ½ of 1% royalty over that deposit. The combined reserve and resource there is approaching 2 billion tonnes at close to 1% copper equivalent. That's contained within a higher grade upper zone and then a bigger porphyry zone at depth. And the high-grade upper zone is what's going into production first, which will facilitate the development of underground infrastructure for the development of the lower zone, ultimately.

Maurice Jackson: You've stated in the past that royalties are powerful financial instruments allowing for embedded optionality. Put that into some kind of context for us on how powerful EMX's 0.5% NSR will be on the Timok Property?

David Cole: Well, it's a good example of the optionality of royalties and one of the reasons why royalties trade at what sometimes seem like absurd premiums. And this concept of optionality is worth touching upon. A great example is the royalty that Franco-Nevada bought on the Goldstrike Mine for a little over a million dollars decades ago. And that royalty has now paid close to a billion dollars, but when they first bought it, on a very modest deposit hosted in poor host rocks hosted on the Carlin Trend. And as luck would have it, they ended up finding a huge deposit at depths. New metallurgical techniques were invented to be able to extract the gold from the more metallurgically complex ores. Greater infrastructure continued to be built on the Carlin Trend, making things more and more economic with time.

So we're sitting here today with nearly 300 mineral property assets worldwide, close to 40 million US dollars in cash, close to 20 million or perhaps a tad more in tradable securities and long-term investments within the portfolio, giving us nearly as much cash and investments and tradable securities as we have raised in the entire history of the company, in addition to our mineral property assets that span the globe, and, of course, we have no debt.

And all of these aspects of optionality, metallurgical advancements, engineering advancements, discovery, most importantly, and of course, commodity price optionality because the price of gold has moved substantially since they bought that royalty, is multiplicative. And so it creates a situation where a royalty that they paid a little over $1 million has paid close to $1 billion now over the life of the royalty, and it's still paying.

And so, of course, not every royalty is going to turn out that nicely, but it does speak to this concept of optionality. And we believe that our royalty on Timok has that kind of potential. Certainly, since we've purchased that royalty, it's turned into a discovery that is measured in billions of copper tonnes. And the price of copper and gold have done very well.

So these aspects of optionality can play in and be very powerful. And that's why you want to own royalties, and that's why I often say that royalties are phenomenal financial instruments.

Maurice Jackson: Speaking of royalties, let's go to Turkey to the Balya lead-zinc-silver mine where EMX Royalty retains a 4% NSR. Are there any updates you can provide shareholders?

David Cole: That's rapidly advancing towards full-scale commercial production. It's already been in small-scale commercial production. We have received production royalty payments in a fairly modest amount as they've done test mining to work on the metallurgy, etc. Metallurgy works out excellently.

There is a commingling agreement which we've signed because the district is divided in half where we have a 4% royalty to the north and the 5,000 ton per day mill is one kilometer from the headframe. They're advancing a spiral decline into the deposit as well. My understanding is that they're at greater than 200 meters depth in that spiral decline, and they're getting close to reaching the first big ore pod to be able to mine with rubber-tired vehicles. Previously, they were mining with a railroad track, and now they're going to mine in a more advanced way, which will facilitate greater tonnage using rubber-tired vehicles, LHD load haul dumps from underground, and running through the 5,000 tonne per day mill.

We're very excited about the ramp-up of production here. Another great example of optionality on a royalty property. Keep in mind, we bought this project originally for US$17,000 from the Turkish government, put together the geology illustrating the potential, and sold it for $100,000 and a 4% royalty. And that 4% royalty will pay us back in spades.

Readers need to understand that it takes a long time for these things to mature. We created that royalty organically more than a decade ago, but it takes a long time for these things to bubble up, work their way up the pyramid, and become cash flowing. But the opportunity for this to happen multiple times within our pyramid is very high.

Maurice Jackson: Speaks volumes for the business acumen and the geologic acumen that the EMX team has here. Let's move north to Finland where EMX holds a 2% NSR on Palladium One's copper-nickel-gold-platinum group project, where they continue to drill more and more well-mineralized intercepts. How do you think this will play out for EMX shareholders?

David Cole: Well, I think it's going to be another really good one. We love those commodities. We think that copper and nickel and platinum group elements and gold are a great place to be. Those are some of our favorite commodities, if not our absolute favorite commodities.

Once again, we bought this royalty early on in the discovery cycle. We bought it for CA$250,000. It's 2% royalty where 1% can get bought back at any time prior to production for 1 million euros, leaving us with 1% uncapped on buyable forever on the property. And it's turning into a large discovery there in Finland. We believe that it's very likely that that will eventually go into production, and it continues to get bigger within that ultramafic complex. It's a particular type of geological environment that hosts that style of mineralization.

And we're very pleased. And it's a good example of us buying royalty to augment a portfolio that we were growing organically. We have other royalties in the district that we've grown organically through the acquisition of exploration licenses and then selling on to other companies and keeping the royalty, so we have a big royalty footprint within that district.

But we're most excited about the one at Kaukua by Palladium One, and I will give Palladium One a plug. I think they're a very well run, technically astute company.

Maurice Jackson: We discussed the good. Let's address the not-so-good. EMX acquired a 19.9% interest in the Rawhide Mine in western Nevada. So far, the mine has not performed up to expectations. What is the plan going forward?

David Cole: Well, this is a great example. And I'm excited about this investment, but I know that that we initially expected a strong cash flow from it right out of the gate. That cash flow has not materialized, as there have been problems with the crusher circuit, etc.

But EMX is doing here what we oftentimes do and that follows our investment with intellectual talent. So we have brought in a top-notch engineering team of ex-Newmont people that are dialing things in here. The mine is back operating very nicely. This last week, I believe, we were averaging 85 ounces a day, pouring gold ounces per day, doré on-site, so the mine's operating quite nicely now.

We do have a large debt on that project. It's about a $15 million debt, and that debt is being amortized, is being paid down. So we do expect to see more cash flow once that debt is paid off.

But more importantly, concerning value creation, is now that we've spent more time on this property and put our geologists out there looking at the potential beyond the known deposits, we've gotten very excited about the exploration potential within this large property that's been tightly held for decades and, thus, not seeing much exploration outside the immediate mine area.

We've been so excited about this that we've increased our percentage ownership, and we're moving towards 40% ownership in that now. And I know it didn't produce the cash flow that we expected right out of the gate, but long term, I'm confident this is going to be a good winner for EMX.

Maurice Jackson: Well, certainly, if you're going to double your position in it from 19.9 to 40%.

David Cole: We feel risk adjusted. We're making a good bet.

Maurice Jackson: Last question. What would you like to say to shareholders?

David Cole: Well, I'm a big believer in this business model. I believe that it creates wealth, sometimes slowly, but it accretes wealth over time. And the key to our stock, a lot of junior natural resource stocks, you want to buy pre-discovery and sell on discovery and catch those waves. With EMX, it's a different model. With EMX, you want to buy the dips and hold the stock long-term. That is conducive to how our business will and has added value over time.

Maurice Jackson: Mr. Cole, for someone listening that wants to get more information about EMX Royalty, please share the website address.

David Cole: www.EMXRoyalty.com.

Maurice Jackson: Mr. Cole, it's been a pleasure speaking with you. Wishing you and EMX Royalty the absolute best, sir.

David Cole: Same to you, Maurice. Thank you.

Maurice Jackson: Thank you, sir. And as a reminder, I am a licensed representative to buy and sell precious metals through Miles Franklin Precious Metals Investments, where we have several options to expand your precious metals portfolio, from physical delivery of gold, silver, platinum, palladium, and rhodium, to offshore depositories, and precious metals IRAs. Give me a call at 855.505.1900 or you may email: [email protected]. Finally, please subscribe to www.provenandprobable.com, where we provide Mining Insights and Bullion Sales; subscription is free.

Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world.

[NLINSERT]Disclosure:

1) Maurice Jackson: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: Labrador Gold. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: Labrador Gold is a sponsor of Proven and Probable. Proven and Probable disclosures are listed below.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of EMX Royalty, a company mentioned in this article.

Disclosures for Proven and Probable: Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.

Images provided by the author.