Note: Golden Independence Mining Corp. (IGLD:CSE; GIDMF:OTCQB) is earning into a 75% interest in the Independence gold project. It's assumed for the purposes of this article that the company achieves an initial 51% interest later this year. Golden Independence will then have three years to earn up to an additional 24%, by spending a total of US$10 million ($10M) more on exploration/development.

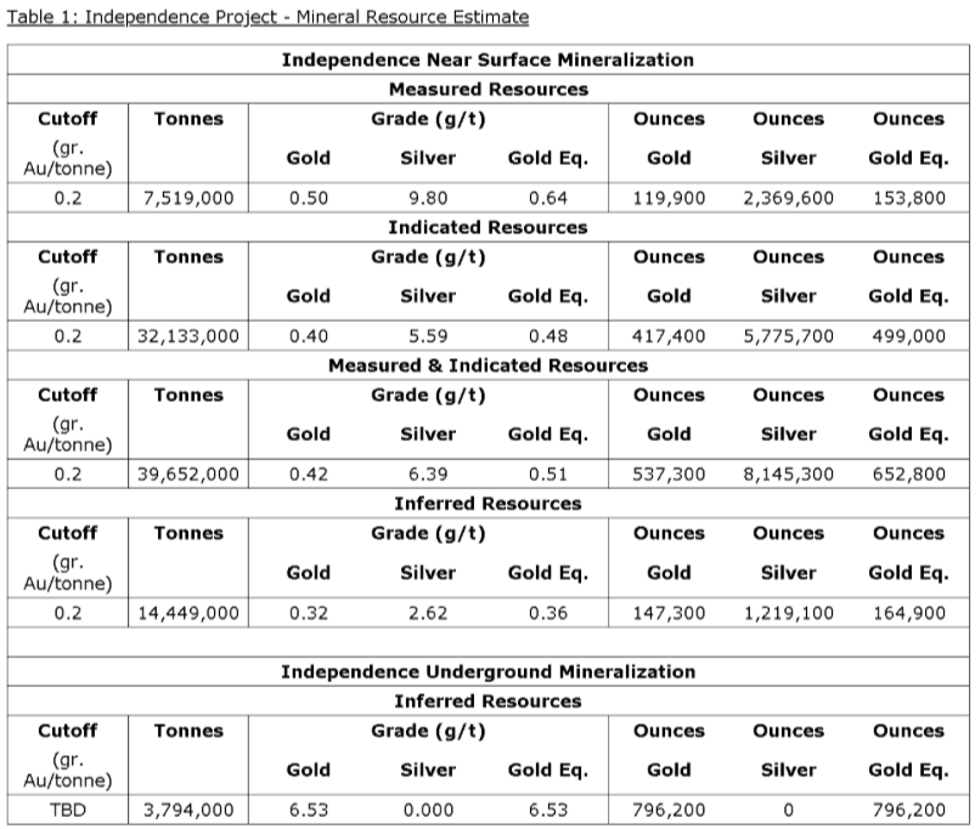

Golden Independence Mining Corp. is well underway in its efforts to earn (up to) a 75% Interest of a brownfields project in Nevada. Last month, management delivered a NI-43-101-compliant mineral resource estimate of 684,600 Measured, Indicated and Inferred ounces gold (plus 9.4 million ounces silver [9.4 Moz]) on a 100% project-level basis. Including silver, that same figure, in gold equivalent ounces, is 817,700.

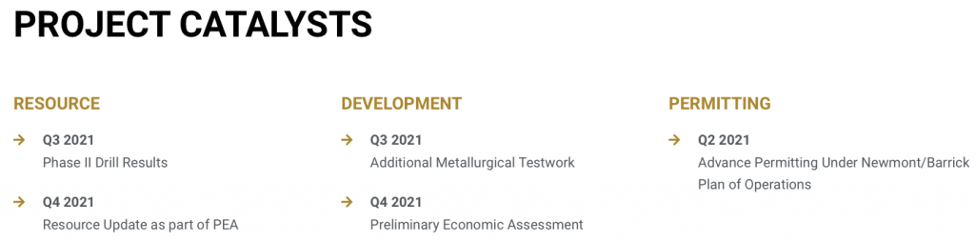

Another resource estimate and a preliminary economic assessment (PEA) are expected by year end. As a reminder, the project's 796,200 (Inferred) deep underground ounces, (grading 6.53 g/t gold) will not be incorporated into the mine plan of the upcoming PEA.

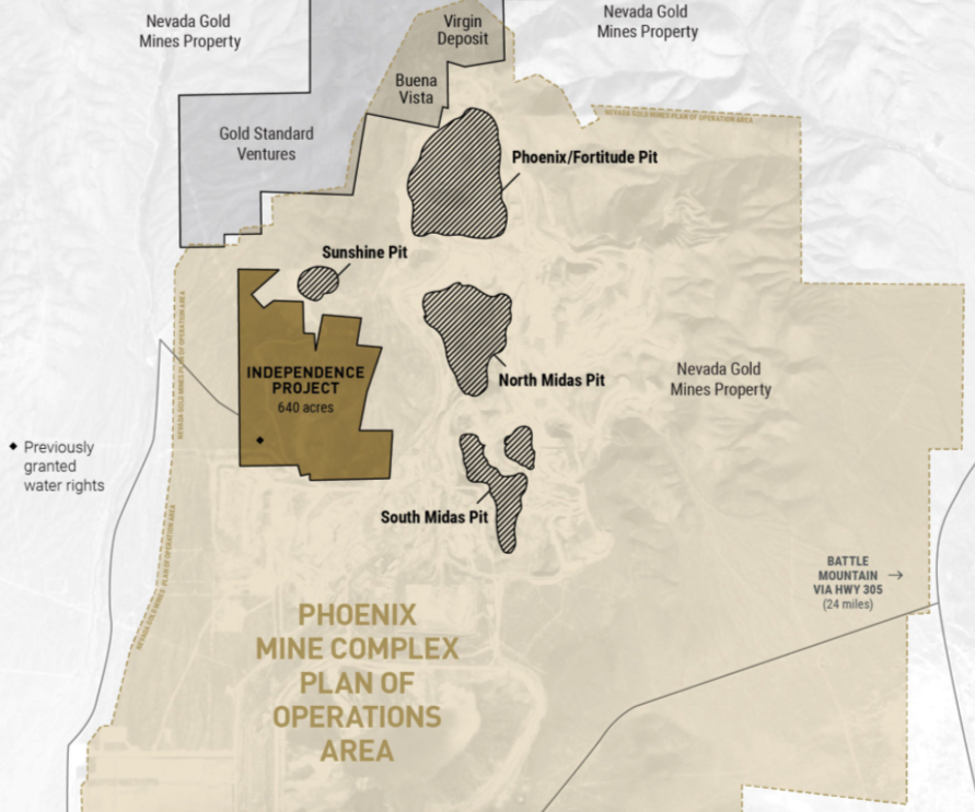

The property benefits from >$34M in past exploration, including over 210 holes drilled. It's adjacent to Nevada Gold Mines' (NGM) Phoenix-Fortitude mining operations, (~180,000 ounces/year at an attractive AISC of ~$1,000/ounces) just 0.5 kilometers (km) to the southwest, on the Battle Mountain-Cortez trend.

In fact, it's more than adjacent, the property sits inside NGM's Environmental Impact Statement and Permitted Plan of Operations. NGM is a 61.5%/38.5% joint venture (JV) owned by Barrick Gold Corp. (ABX:TSX; GOLD:NYSE) and Newmont Corp. (NEM:NYSE). NGM is a major: It will produce ~3.5 Moz of gold this year; it has 12 open-pit mines and 10 heap leach facilities.

This location is ideal, near majors NGM and Kinross Gold Corp. (K:TSX; KGC:NYSE) and mid-tiers Coeur Mining Inc. (CDE:NYSE) and Hecla Mining Co. (HL:NYSE), in a brownfields setting, in the heart of Nevada's incredible gold and silver abundance. Did I mention that Nevada ranked #1 of nearly 80 global jurisdictions in this year's Fraser Institute Mining Survey?

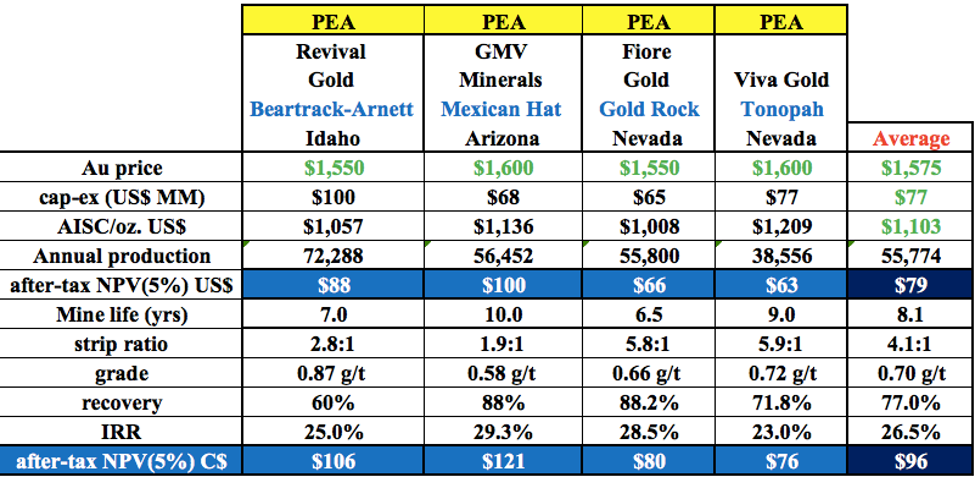

Management is pursuing a simple, low-risk, heap leach project that (subject to a PEA) could produce ~50-70k ounces of gold/year for 79 years. Based on four peer heap leach projects in the western U.S., all at PEA stage, it seems reasonable that Golden Independence's property could develop into a project with an after-tax NPV(5%) of CA$90-$100M.

However, the heap leach approach could be replaced with an entirely different, much more sexy project, if gold prices remain elevated. In addition to soon owning 51% of the shallow open-pittable resource, Golden Independence has a much deeper mineral resource of 796,200 (Inferred) ounces of gold. These ounces carry a grade of 6.53 g/t.

So here's the thing about those high-grade, much deeper ouncesthey're valuable as a starting point to what could become a larger deposit. However, they're worth tremendously more to a mid-tier or major with the cash to drill dozens of very deep holes.

If only there were a large giant gold producer nearby that might be interested in 6.53 g/t gold material Wait! Of course there is, that would be NGM. There's a slight problem though.

It's safe to assume NGM would not want to get involved with the project unless/until it was 100%-owned by IGLD. With that in mind, management will be trying to strike a deal to obtain 100% ownership sooner rather than later. As it stands, IGLD has three years to earn into a 75% Interest.

I said earlier that the heap leach plan could be scrapped. If NGM were to take a keen interest in IGLD's project (after gaining 100% control of it), they would likely want to develop the more profitable high-grade deposit right away.

NGM could perhaps reach production from underground in three or four years. How so soon? NGM is one of the largest gold producers in the world, and IGLD's property is within NGM's existing plan of operations.

To be clear, the immediate focus is on the oxide mineralization amenable to heap leaching. The resource delineated 817,700 gold-equivalent ounces, but that's before recoveries. There will be slippage, as the range of recoveries for gold and silver is 40%85%. A lot will depend on the mix of transitional, sulfide and oxide zones.

Management will learn more about that through the PEA process. I estimate that 500,000 heap leach recoverable, gold equivalent ounces is a reasonable estimate for the project as it stands. That would be a very nice outcome: 79 years at 5671,000 ounces/year.

Finding more higher-grade (still shallow, open-pittable) oxide material has the potential to add tens of thousands of ounces, but it won't be a game-changer unless the high-grade intervals found to date are more widespread than currently understood.

The best intercept was shocking: 9.1 g/t gold over 24.4 meters! While exciting, management does not yet know how extensive this high-grade zone is.

If Golden Independence only had the heap leach project, I think the upside would be attractive, but not exciting. However, one has to access the potential value of the 796,200 ounces of 6.53 g/t gold in the hands of a mid-tier or major.

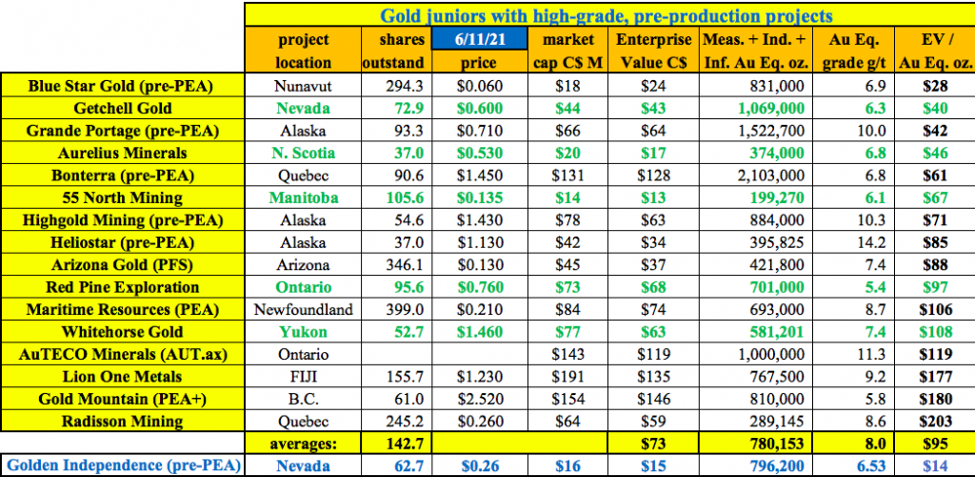

One way to do that is to compare the size and grade to peer North American gold juniors. In the chart below, one can see a number of examples.

The five highlighted names (in green, all pre-PEA) have an average enterprise value (EV; market cap + debt cash) to ounce of gold in the ground (EV/oz) ratio of ~$72/oz. The average resource size and grade is 585,000 ounces at an average 6.4 g/t, figures that are very close to IGLD's high-grade, underground resource.

Since IGLD's resource is 100% Inferred, (peers are a mix of Measured + Indicated + Inferred), I ascribe a $50/oz valuation estimate to IGLD's 796,200 ounces. That's a 30% haircut to the $72/oz average mentioned above. At $50/oz, IGLD shares have an implied value of CA$0.65. (Note: this is not a price target, merely a thought experiment). The current share price is CA$0.26.

I believe that if the gold price remains elevated, a rising tide will lift all boats. Consider that a year ago, PEA and feasibility reports were using $1,400-$1,450/oz long-term gold assumptions. In recent weeks I've seen three with $1,600/oz and two with $1,650/oz gold price assumptions. A year from now, I suspect the price might be $1,750/oz.

A heap leach operation of say 60,000 ounces/year, for 78 years, would be very profitable at today's spot price! Sixty thousand ounces x US$800/oz operating margin = CA$58M/year in operating cash flow. Add merger and acquisition (M&A) to the picture and valuations of near-term operating mines could soar.

Regarding the deep high-grade scenario (funded by NGM or another mid-tier or major), the sky's the limit on how that could potentially unfold. I imagine Golden Independence being free carried through a Bank Feasibility Study, while maintaining significant ownership in the project, (say 30%).

Owning 30% of a high-grade underground mine operated by a major would be quite valuable. NGM, in particular, has the experience, deep pockets and mining infrastructure in place to significantly grow and exploit the current 796,200-ounce resource.

While it's impossible to say if NGM will ever build a mine (or develop a satellite deposit) from Golden Independence's high-grade resource, if it's meant to be, I imagine the operation could be 150,000+ ounces/year. NGM's adjoining Phoenix mine is operating at ~180,000 ounces/year, and is now processing lower grade material than it has in the past.

Therefore, 30% ownership of 150,000 = 45,000 ounces/year attributable to IGLD, with perhaps a US$1,000/oz profit marginthat would be CA$54M in free cash flow per year, for possibly 10+ years, starting in 2024 or 2025, with far less equity dilution, and far less operating risk.

In conclusion, Golden Independence is highly tied to a strong gold price. It benefits very nicely from increases, but below $1,650/oz, robust profitability would start to wane. The company is undervalued in an open pit, heap leach mining scenario, and very undervalued if management can partner with a major to develop its high-grade underground gold ounces.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University's Stern School of Business.

[NLINSERT]Disclosures/disclaimers: The content of this article / interview is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Golden Independence Mining, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Golden Independence Mining are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed / registered financial advisors before making investment decisions.

At the time this article/interview was posted, Peter Epstein owned stock options in Golden Independence Mining, and the company was an advertiser on [ER].

While [ER] believes it is diligent in screening out companies that, for any reason whatsoever, are unattractive investment opportunities, [ER] cannot guarantee that its efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of any article or future content. [ER] is not expected or required to subsequently follow or cover any specific events or news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure:

1) Peter Epstein's disclosures are listed above.

2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.