1. Introduction

Kenorland Minerals Ltd. (KLD:TSX.V) was mentioned to me at the end of 2019 by mining legend Rick Rule, departing CEO of Sprott US Holdings, and more specifically he extensively expressed his admiration for the young CEO of Kenorland, Zach Flood. According to Rule, who recently announced his retirement, Flood is a top category prodigy, who is probably destined to go places. Such an endorsement is pretty rare, so I kept this in the back of my head, as Kenorland wasn't trading at the time. I had to wait until after the RTO in January of this year. After a few weeks of trading the share price started to come down, also caused by headwinds for gold as interest rates for bonds were steadily rising:

Share price 3 month period; Source: tmxmoney.com

Now at a more convenient share price and valuation, seemingly bottoming out, but also cashed up with almost C$10 million in the treasury, and their first drill program of 2021 just commencing, it seemed to be a good time to research the company and hear from CEO Flood himself what could make Kenorland Minerals an interesting investing opportunity.

All presented tables are my own material, unless stated otherwise.

All pictures are company material, unless stated otherwise.

All currencies are in US Dollars, unless stated otherwise.

2. The company

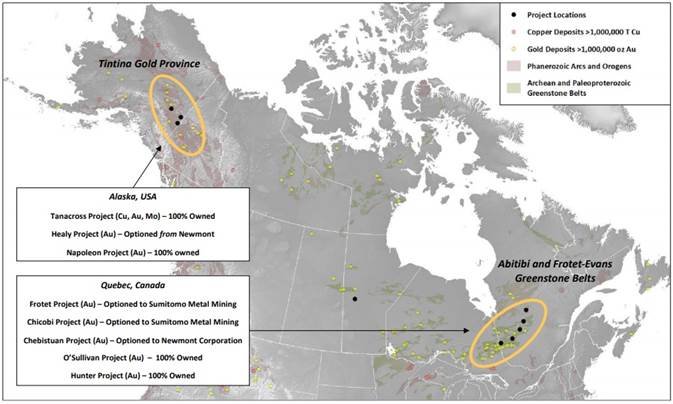

Kenorland Minerals is a prospect generator with a hybrid business model of joint venture funding and self-funded projects to maximize opportunity for exploration success. The company has been named after one of the earliest known supercontinents on earth, thought to have formed 2.7 billion years ago. The company currently has gold and copper projects in Quebec and Alaska. The flagship project of Kenorland is the Frotet project in Quebec, and other important projects are the Tanacross and Healy projects in Alaska. I will elaborate a bit more on prospect generators later on.

These are all pretty good jurisdictions for mining projects according to the Policy Perception Index (PPI) of the most recent Fraser Institute Survey of Mining Companies (version 2020). Quebec can be found at position 17 out of 77, and Alaska at 13 out of 77. The PPI is the most important figure of this survey, as it indicates the mining friendliness of a jurisdiction, which encompasses corruption, permitting, speed of administrative processing, politics, local sentiment, etc. The Survey is usually published in the last week of February, for your information. I find it useful as it is by far the most comprehensive of its kind, but it isn't perfect as it is based on a questionnaire sent to mining companies. Most of the companies don't even bother to answer, or others could have agendas when answering the questions, being aware of, for example, governments and investors studying the Survey as well. Notwithstanding this, I found most of the jurisdictions except a few European countries, where, for example, permitting takes forever or could even be overturned after granted, or local resistance significant, fairly ranked.

The management team is led by geologist President and CEO Zach Flood. Despite his relatively young age (35) he has been president and CEO since 2016 of Kenorland, and has been traveling the world since he was 18 as a geologic technician, at the well-known Oyu Tolgoi mega project in Mongolia. He was trained for many years at the Ivanhoe Group, and finetuned his geologist crafts under the guidance of legends like David Broughton, and entrepreneurial thinking in mining by the likes of Robert Friedland.

Another geologist talent already recognized by the industry is EVP Exploration Francis MacDonald, having worked for Newmont for most of his career, and is a specialist in orogenic and VMS deposits, exactly the type Kenorland is looking for. Among others he worked at several projects in Africa, but also at the Hope Bay project in Nunavut, Canada.

Kenorland Minerals has its main listing on the TSX Venture, where it's trading with KLD.V as its ticker symbol. With an average volume of about 47,632 shares per day, the company's trading pattern is not very liquid at the moment, but I expect this to improve when drilling results will start to come in during April/May 2021 and management will hit the road marketing the story.

The company currently has a tight 45.57 million shares outstanding (fully diluted 55.499 million), 1.87 million warrants (the majority at @C$0.70 expiring in 2023) and several option series to the tune of 7.05 million options in total, the majority priced at C$0.25 or more and expiring from 2024 to 2025 onwards. Kenorland sports a market capitalization of C$36 million based on the March 5 share price of C$0.79. The company is basically controlled by management, as 51% is held closely by management, Board of Directors and insiders. There is decent institutional ownership, among them Commodity Capital and Exploration Capital Partners (a Sprott fund), and together they own 11% of the company, and close associates like hold 15%, meaning 77% is in tight hands.

As a reminder: the hybrid prospect generator model has been described extensively in one of my articles about Avrupa Minerals with the pros and cons. The main characteristic is that such a company forms JVs with other, larger companies who finance the joint exploration efforts for the majority of the project in return. The hybrid part consists of the junior self-financing by raising money in the markets (or selling royalties on their projects) one or more of their projects, but also not having to hand over large parts of their projects.

Advantages of a prospect generator are limited dilution of share structures, strong partners and spread out risks and increase chances for success as usually more than one project is explored at the same time, with different partners. Disadvantages are that the value proposition for investors isn't always clear, the junior loses the majority of project ownership, and the agenda of the JV partners isn't always the same as those of the junior. Especially when large majors are involved, investors need to beware of how the JV deal is structured, regularly resulting in the major running away after first drill holes don't immediately indicate Tier I potential, despite still being a pretty good prospect for an intermediate producer. When talking to Rick Rule about prospect generators, it turned out they were one of his favorite categories to invest in because percentage-wise he had the most success with this category, although the wins weren't as extreme as other higher risk categories for the obvious reasons.

Being asked about this, CEO Flood had this to say about consciously choosing a hybrid model: "Mineral exploration is a very high risk business, the more ground you can cover and the more targets you can test, the better your odds of success are. With a very large portfolio, currently over 1,000,000 acres of ground, it makes sense to bring in partners to help advance a portion of this portfolio otherwise there is a risk of spreading ourselves too thin."

3. Projects

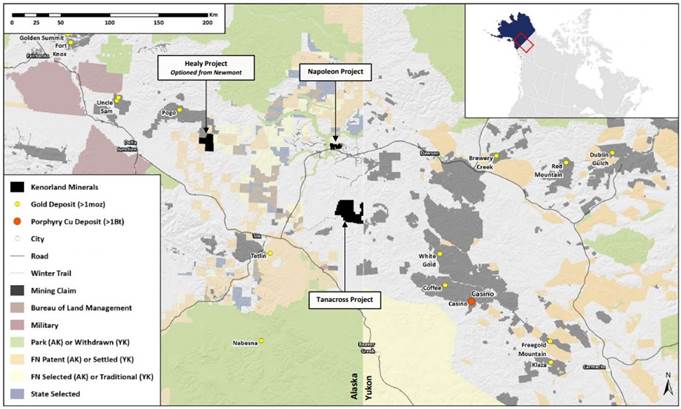

CEO Zach Flood has been busy building an interesting asset portfolio with equally interesting JV partners (Freeport McMoRan, Sumitomo and Newmont) for the last four years, until January of this year as a private company. After the reverse takeover of Northway Resources on January 4, 2021, the company started trading as Kenorland Minerals. Kenorland Minerals has a portfolio of seven projects, variable in stage of exploration. Five projects are located in Quebec, Canada, and two can be found in Alaska, USA. Please note the third project shown in Alaska on the map below, the Napoleon project, was sold recently to a private company on February 5, 2021.

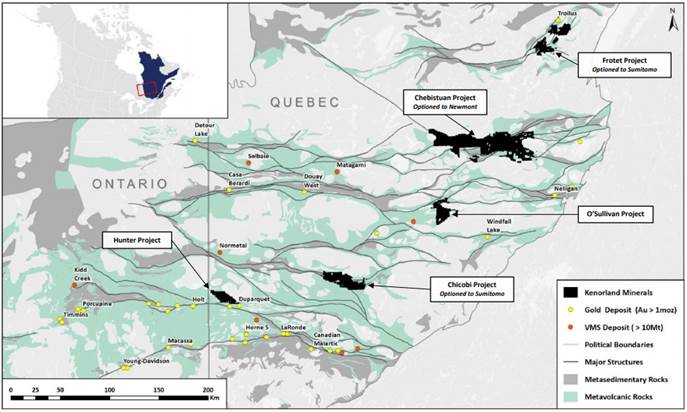

Two projects are optioned to Sumitomo Metal Mining Canada (Frotet and Chicobi in Quebec), and one other project (Chebistuan in Quebec) is optioned to Newmont. As the company is currently focusing on three projects, the Frotet JV project in Quebec, and the Healy earn-in JV project plus the fully owned Tanacross project in Alaska, I will focus on these projects as well. When looking into the financials, I noticed that the company spent significant money on Chicobi, as it did on Frotet, for 20192020 exploration (C$3 million vs C$4 million), so I wondered why Chicobi didn't make it to the flagship list although it was optioned to Sumitomo, and when it might be explored further. According to Flood, the Chicobi expenditures have all been focused on regional till sampling which requires sonic drilling, which is very expensive and very time consuming. They have not gotten to the diamond drill stage yet, but expect to later this year or early next year. So basically it's still grassroots stage and therefore not a "flagship." Kenorland is the operator on Chicobi, and Sumitomo can earn into 51% after spending C$4.9 million on exploration before May 31,2022, and into 70% after committing to another C$10 million within three years, to be indicated 90 days after reaching the 51% threshold.

Besides this, the exploration expenditures on Tanacross appeared to be substantial at almost C$6.8 million, paid for by 20182020 JV partner and copper giant Freeport McMoRan. C$1.94 million of this amount was spent on drilling, and other expenses were used for things like consulting, supplies, travel and accommodation. As Tanacross is a very large project as you will see later on in this article, I asked Flood if this wasn't an ideal candidate to option out again, as it seemed to me that scale and connected costs could only be a good fit for a (very) large company. Flood commented: "We are always open to bringing in a partner if it is the right deal."

Quebec projects

As Quebec is the host of an extensive Greenstone Belt that contains some of the richest gold deposits on the planet, has favorable taxation on exploration and has relatively cheap exploration costs, CEO Flood was keen on amassing significant land positions in this jurisdiction:

It appears the more to the south, the more deposits were discovered. Kenorland has a technical presentation on its website that also shows a clear increase in exploration to the south. This could have been related to relatively easy to understand things like more extreme weather conditions and an increasingly harsh environment for exploration. Whatever the reasons were, according to Flood, he saw no reason to avoid for example the most Nordic trend in the Abitibi Greenstone Belt, the Frotet-Evens Greenstone Belt, which hosts only one significant deposit, the Troilus copper-gold porphyry (7 Moz Au), so he staked as much ground on the trend as he could. Let's have a look at their flagship Frotet project first.

Frotet project

The flagship Frotet project was staked in 2017, and is located adjacent to the Troilus deposit (7.06Moz Au Ind and Inf), owned by Troilus Gold. The Frotet Project is highly prospective for significant orogenic gold, intrusion-related gold (e.g., Troilus) and VMS mineralization. The two staged earn-in agreement allows Sumitomo to earn 65% by funding C$4.3 million in expenditures over an initial three years. Sumitomo has currently exercised this initial option, and has the option to earn an additional 15% (80% total) by funding another C$4 million over the following year. Once a joint venture is formed after reaching the 80/20 threshold, pro rata funding begins and any party diluted below a 10% interest will convert their interest to a 2% uncapped net smelter royalty.

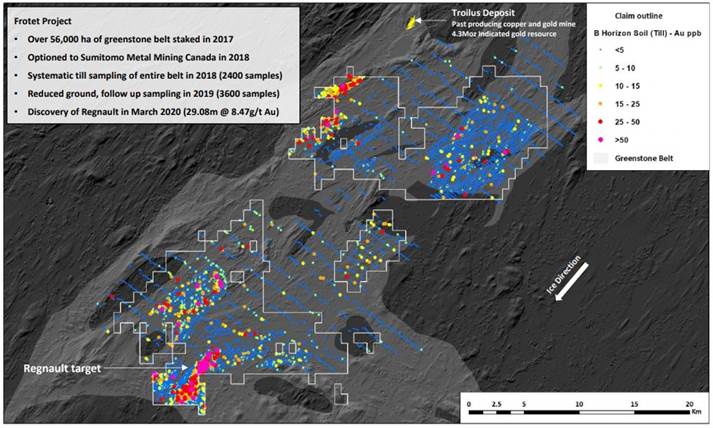

Frotet sampling in 2018 indicated lots of interesting targets, and the Regnault target obviously stood out:

I wondered if it wasn't possible to stake more ground south of the Regnault target as the gold samples extended to the border of the existing claims. According to Flood, the gold sampling, the magnetic signature and other reconnaissance exploration indicated a low probability of drilling success, and not at the least a park is located just south of the O3 ground that was acquired, so they had good reasons to decide not to stake further in that direction.

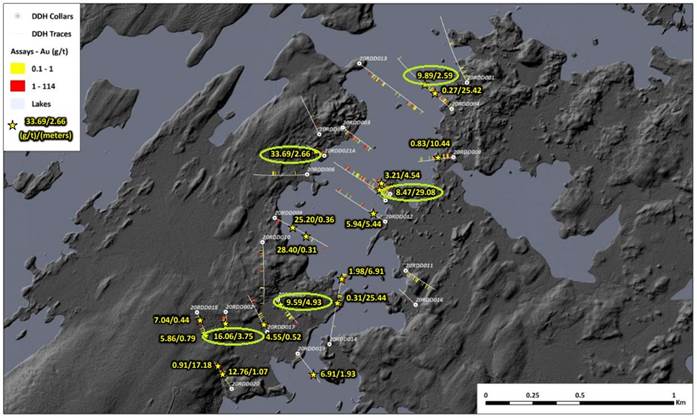

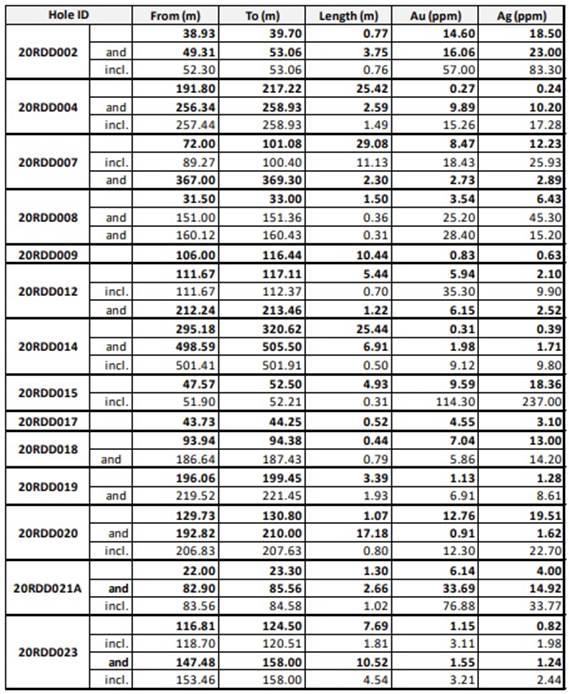

Drilling in 2020 by Kenorland returned solid results for the northern part of their Regnault target, highlighted by for example the impressive 29m @ 8.47g/t Au from 72m, but also 2.6m @ 9.9g/t Au from 256m depth, 4.9m @9.59g/t Au from 47m, and 3.75m @ 16g/t Au from 49m depth.

Regnault was a greenfields target, and was a completely blind discovery, as there was no outcropping quartz veins. I asked Flood out of curiosity exactly how he became interested in this distinct area. He stated that "The systematic geochemical sampling really guided us to the Regnault area and there is a very large footprint, extending 45km along strike."

14 of 23 initial holes hit economic mineralization, which is a promising start. As can be seen in the table with drilling highlights, lots of holes hit gold in multiple instances:

For a total blind greenfield discovery these are impressive results, as some well-known deposits were hit only after dozens of holes. It is good to see how management followed up on the most successful hole 20RDD007, with 20RDD021-023, but it isn't easy to duplicate the same kind of results. Notwithstanding this, the variety of locations and depths suggest a widespread stockwork of veins. If management is on to a second Troilus type of deposit, the potential is significant, as mineralization over there is also found over a large strike length, and in addition is open at depth. Troilus is hosted in diorite, and in porphyritic felsic intrusions, and this is also seems to be the case at Regnault. The difference is that 90% of Troilus mineralization appears as disseminated low grade gold, and most of Regnault mineralization seems to be high grade veins.

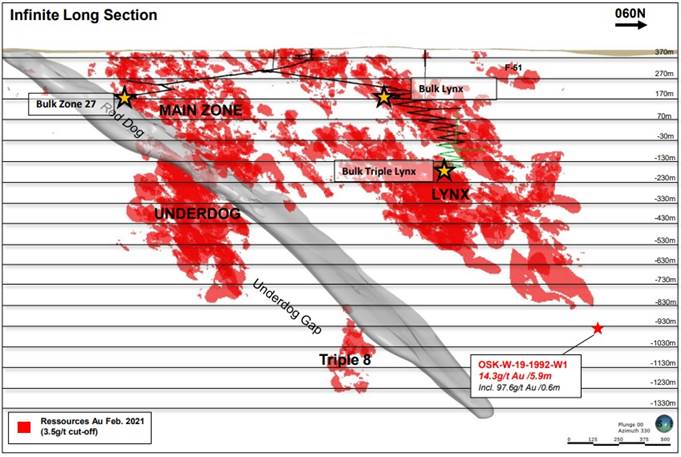

Therefore management thinks Regnault could also be an intrusion-related gold system, similar to Windfall, Cote Lake or the Chibougamau camp, where intrusive phases precipitate through mafic/felsic volcanics, but at higher grades. A long section of Windfall (Osisko Mining) can be seen below:

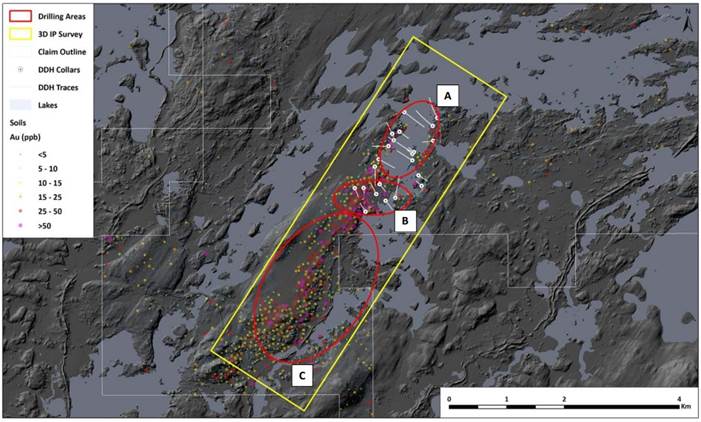

It is still early days and orientation of veins is still unknown, but Kenorland already has established a potentially mineralized zone of 2000 by 500m, and it will be important to prove up continuity now, and find out if there could be open pit potential and/or Windfall-style potential at depth. The current scale and drill results certainly warrants the quest for a multi-million ounce target, but only time and a lot of drilling will tell. Sumitomo is certainly interested, and currently proceeding with the Phase 2 earn-in (up to 80%) with an approved budget of C$3.8M, consisting of a 3D IP Survey and a 9,000m drill program starting in Q1, 2021, also targeting the southern part of Regnault:

Sumitomo Metal Mining is a Japanese mining giant, and has interests in large copper mines and mid-tier gold mines/projects in Japan, Australia and the Americas. It is aggressively looking for other projects, and also investing in exploration all over the world. I'm not really convinced that it is sheer coincidence they picked Frotet, as the Troilus deposit is nearby, and could provide synergies although the mineralization is different. For Sumitomo, my guess is Troilus would rank as a medium-scale operation (see 2020 Activity report as part of their 2020 Annual Report), and Regnault might be a nice high grade bolt on in the far future, as they commented:

"We have had to slow the pace of exploration activities due to the effects of the COVID-19 pandemic. The pace of global development in regard to considering the acquisition of new interests has also slowed and we think we have to respond through investigation and preparation. In addition to the minor participation in large-scale projects that we have undertaken in the past, we are also pursuing negotiations on medium-scale mine operations, where we can act as the operator."

At the very least, by JV-ing Regnault with Kenorland, Sumitomo has already assured it has been taken off the market, in case a substantial deposit could be in the making. Notwithstanding these hypothetical forward looking visions, a lot of exploration has to be completed first.

The current 9,000m drill program will consist of three parts:

A. 3,000m of drilling from ice stepping out from previously intersected mineralized zone, focusing on highlights like 20RDD007 (29m @ 8.47g/t Au)

B. 3,000m of drilling from land stepping out from previously intersected mineralized zones

C. 3,000m of drilling for regional targets at Regnault South targeting new mineralized zones

This program has started on March 4, 2021. Results are expected to roll in from the first week of April onwards. The 3D IP survey is currently being completed, covering over 4km of the Regnault trend, and resulting preliminary sections and targets should be released early May.

Alaska projects

Kenorland has three projects in its Alaska portfolio: it fully owns the Tanacross project, and is earning up into the Healy project from Newmont in a JV as mentioned. Management sold the most early stage Napoleon project to private company J2 Metals at the following terms in order to focus better on Tanacross and Healy:

- 15% of the issued and outstanding shares in J2 on a fully diluted basis;

- a 1% net smelter returns royalty on the Napoleon Project; and C$500,000 in committed expenditures on the Napoleon Project by J2 within 12 months of the effective date pursuant to an operator services agreement in which Kenorland acts as operator on market standard fees.

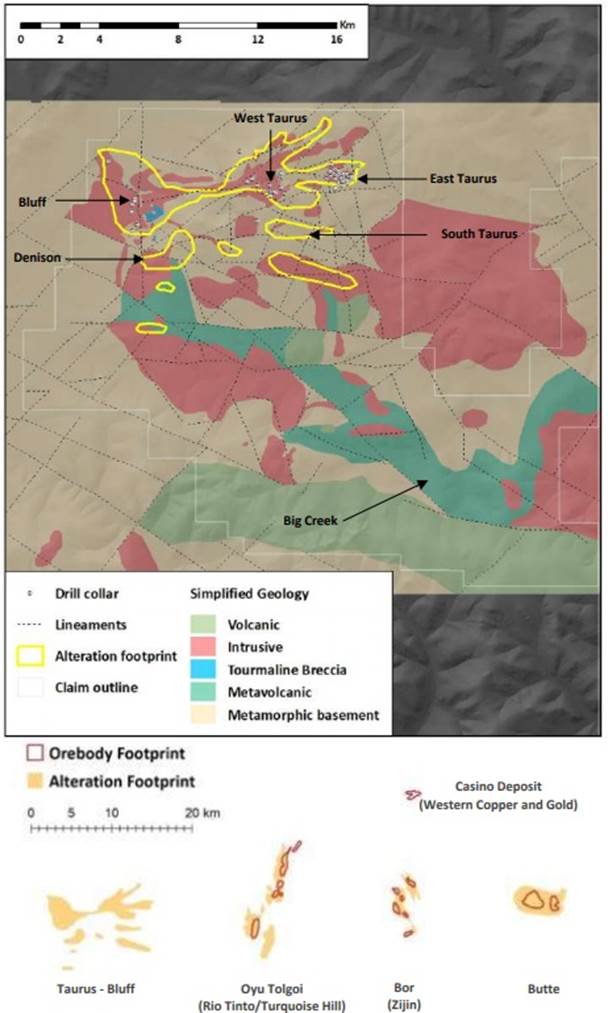

Tanacross project

The Tanacross project is a project formerly explored in 20182020 by Freeport McMoRan and others. These parties drilled results like 239m @ 0.30%Cu and 0.23g/t Au, and 276m @0.23%Cu and 0.16g/t Au, but abandoned the project as they aimed at higher grades and they tapered back exploration when the market was hit hard due to the pandemic. The drill results seem low grade, but current copper production is at an average grade of about 0.50% Cu at the moment, and average development copper grade is falling below this, so Tanacross isn't far off, certainly not at current copper and gold prices. The issue here is a matter of size, and this is something Tanacross doesn't seem to lack. It is a district scale collection of alteration footprints, covering porphyry centers, analogue to very large low grade deposits like Pebble and Casino.

As can be seen, the scale of the alteration footprint is colossal, but the drill bit will have to verify potential mineralization of course. For 2021, reconnaissance exploration is planned (mapping, geochemistry, geophysics), followed by 2,000m of drilling starting in June of this year, to test new targets in the area.

Healy project

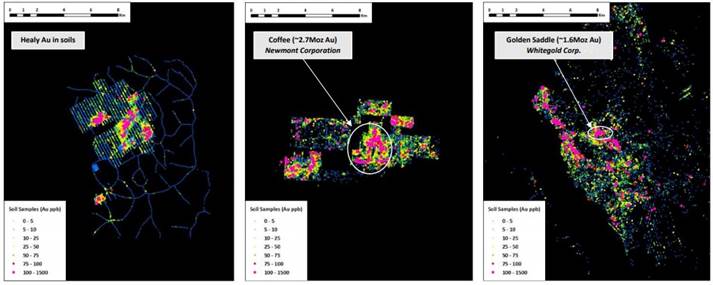

Kenorland's second Alaska project is the Healy project, which it is earning into 70% from Newmont Corporation, for spending US$4 million in exploration expenditures over a four-year period. This project is also of considerable scale, has seen extensive soil sampling and 10 holes of near surface RC drilling, with a highlight of 49.4m @ 0.42g/t Au. Healy can be compared for size with the likes of Coffee (Newmont) and Golden Saddle (Whitegold), when looking at sampling maps:

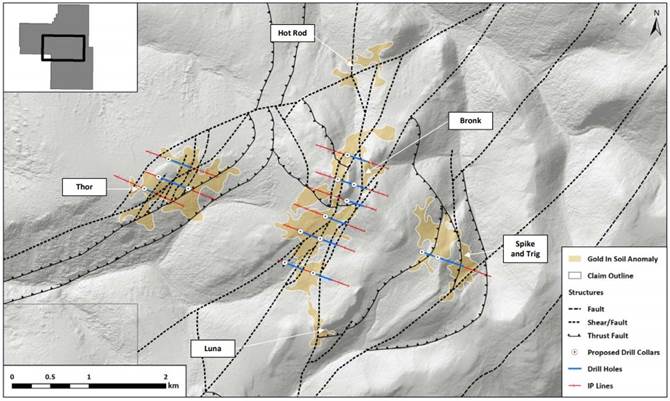

The intersected mineralization is characterized by broadly disseminated gold in bedrock. The area is host to several large, low grade deposits like Fort Knox, Livengood and Pogo (all >10Moz Au). Management has planned a 4,000m diamond drill program for 2021, starting in August, 2021, and will target the strongest chargeability anomalies associated with faults and coincident gold in soil anomalies. The planned drill holes will closely follow IP lines, which in turn followed the soil anomalies, as can be seen on this map:

It can be seen that the gold in soil anomalies are located in the vicinity of faults, as is often the case. This can also be observed on a larger scale in the entire Greenstone Belt, as many deposits are found close to major fault lines.

As a quick recap, the timelines for the various exploration programs for this year look like this:

As the company can drill all winter at Frotet, and the Alaska projects have a winterbreak, news flow is guaranteed as assays are generated throughout the year.

4. Conclusion

As a greenfield explorer, Kenorland Minerals managed to land a few impressive JVs, interesting projects and lots of cash. This has everything to do with management, as CEO Zach Flood is widely considered a talented geologist, already with a ton of experience under his belt and trained by the very best in the industry. As a consequence, his backing is also top notch so he doesn't have to worry about money soon. At his first rodeo as a CEO, he already showed why he has earned the trust of many, as Regnault returned good results, and has the potential to host a significant deposit. The Alaska projects have the potential to generate even larger resources, but are still early days. As the share price has come down after the RTO in January and the current sell-off due to rising interest rates, Kenorland Minerals seems a pretty interesting exploration bet for junior mining investors after the dust has settled on the markets.

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter, in order to get an email notice of my new articles soon after they are published.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long-term commodity pricing/market sentiments, and often looking for long-term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

[NLINSERT]Disclaimer: The author is not a registered investment advisor, and currently has a long position in this stock. Kenorland Minerals is a sponsoring company. All facts are to be checked by the reader. For more information go to www.kenorlandminerals.com and read the company's profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Streetwise Reports Disclosure:

1) The Critical Investor's disclosures are listed above.

2) The following companies mentioned in the article are sponsors of Streetwise Reports: Troilus Gold. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts and graphics provided by the author.

to the Manitou Gold Project, NW Ontario, Canada")