Note: The company is raising C$17M in equity at C$0.30, with a full warrant at C$0.45, and is on track to finalize a C$9.5M gold/silver loan facility. All figures are US$ unless indicated otherwise. (Au) = gold, (Ag) = silver.

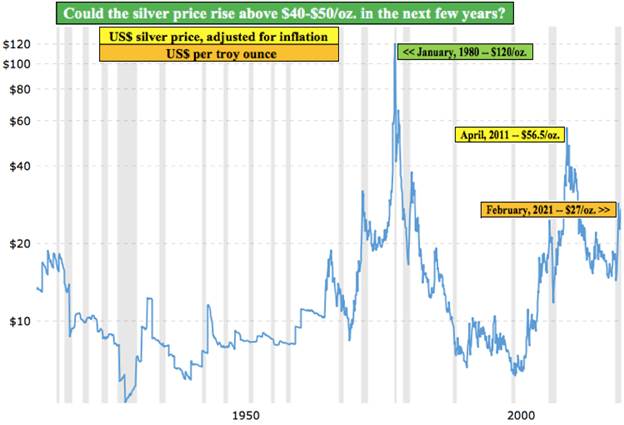

If gold (+24.4% in 2020) were to repeat that performance in 2021, it would end the year at $2,358/oz. If silver (+47.4% in 2020) were to do as well again this year, it would hit $40/oz.

In looking through recent analyst reports, GS, CIBC, JPM, Citi and Wells Fargo analysts are forecasting silver reaching $30$36/oz. and gold hitting $2,000$2,300/oz. by the end of next year.

Unlike some junior miners, VanGold Mining Corp. (VGLD:TSX.V, VGLDF:OTCQB) doesn't need $30+ silver or $2,000+ gold to thrive. CEO James Anderson believes his expert team can rehabilitate and restart the past-producing El Pinguico mine in central Mexico in six to nine months. VanGold has a pro forma Enterprise Value (EV) {market cap cash + debt} of $33.9M = C$43M.

VanGold delivers impressive PEA with ample room to grow

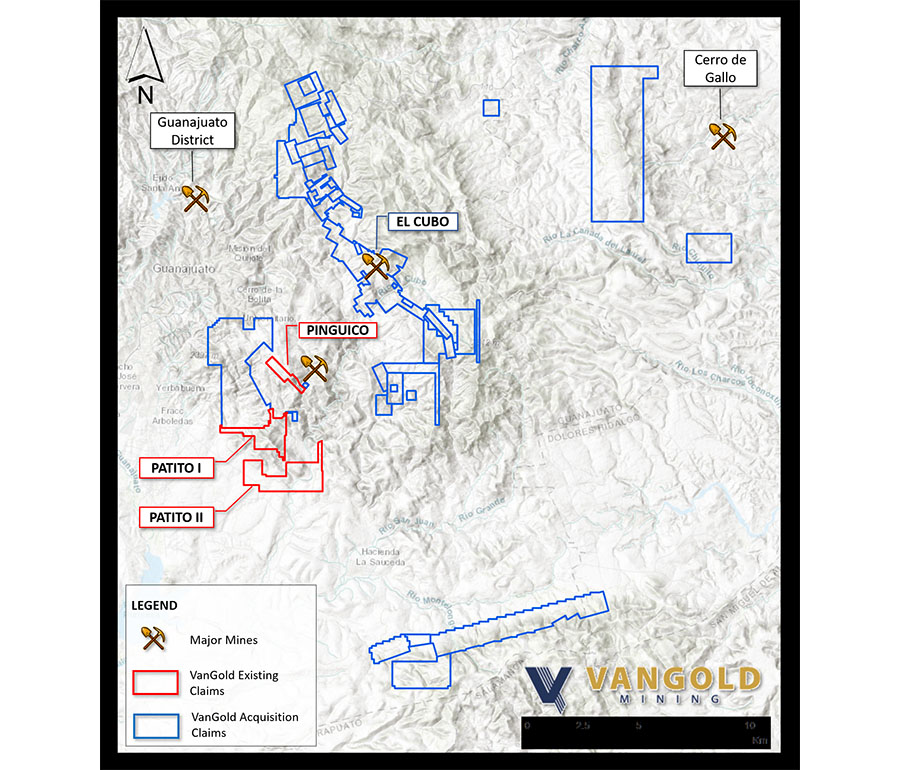

VanGold Mining's El Pinguico project, is a historic high-grade silver and gold mine in production from the late 1880s until 1913. It's located in the region of Guanajuato, in central Mexico, an area with 500 years of rich mining history.

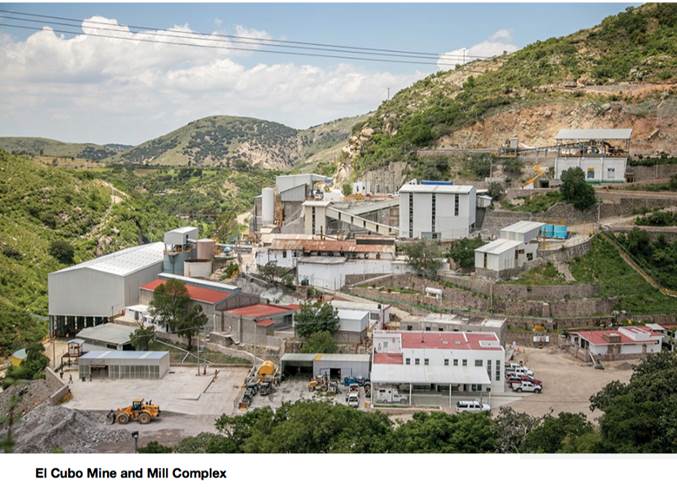

Readers may recall that in December, management announced a bold proposal to acquire the nearby El Cubo mine and mill complex (El Cubo) owned by Endeavour Silver. Closing on this C$19M deal, expected in March, would be a game-changer.

Recent work by VanGold and third-party consultants has established a 27.6M ounce (Indicated [26%] + Inferred [74%]) silver equiv. (Ag Eq) resource. The 20.4M Inferred ounces carry a high grade of 435 g/t Ag Eq = 6.5 g/t gold (Au) equiv.

Combined, the two operations could deliver up to 1,500 tonnes per day (tpd) of silver and gold ore to the mill. However, Mr. Anderson's team plans to send just half that amount in the initial years while it develops a robust, optimized mine plan that avoids mining dilution.

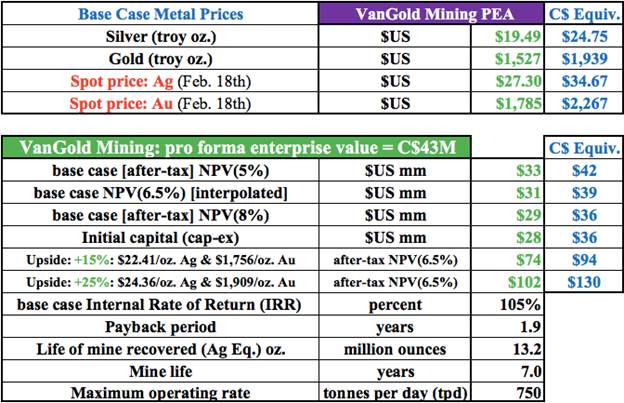

In a Preliminary Economic Assessment (PEA) completed this month by Behre Dolbear & Co., a seven-year mine life would exploit a bit more than 50% of a newly defined [7.2M Indicated + 20.4M Inferred = 27.6M] Ag Eq ounce resource.

Readers should note that despite a promising third-party PEA, there's still considerable risk and a number of challenges to overcome (not to mention COVID-19). However, I believe it's a question of when, not if, the company crosses over to sustainable profitability.

Restarting mining, milling and waste storage operations at two mine sites, concurrently, represents a significant challenge. However, Anderson, the board and VanGold's on-the-ground team (including three world-class technical advisors) have advanced the company quite nicely.

Risks mitigated by strong balance sheet, near-term production

If investor appetite is any indication, shareholders seem comfortable with VanGold's risk profile. The team is not only finding silver and gold, they've found eager investors to fund expansion, enabling the share price to rise from a low of $0.03 last year, to a (way oversubscribed) private placement price at $0.30. The private placement has now been upsized three times to C$17M.

Behre had already been conducting engineering work for VanGold in connection with the proposed acquisition, refurbishment and operation of El Cubo, and restart of El Pinguico. The Group is billed as one of the oldest and most trusted mineral industry advisory firms in the world, specializing in technical and and strategic studies for mining companies.

The PEA uses a silver price of $19.49/oz., and a gold price of $1,527/oz.generating an after-tax NPV(6.5%) of ~$30.7M = C$39M. However, at metal prices +25% above the base case ($24.36 / $1,909), the NPV(6.5%) is ~$102M = C$130M.

As I write this, spot silver is at $27.30/oz and spot gold = $1,785/oz. Compare that C$130M figure to VanGold's pro forma EV of ~C$43M {pro forma cash = C$17.5M, pro forma debt = C$9.5M}

If in a few years VanGold has identified five years' of Measured and Indicated resources that support operating above 750 tpd (mill capacity = 1,500 tpd), then an increase in throughput would be contemplated. Under Endeavour Silver, the mill routinely ran at >1,000 tpd and the mill is reportedly in great shape.

Anderson's team believes there might be opportunities to acquire outright, or toll-mill, stranded deposits in the region. If true, the mill could be running at 1,0001,250 tpd by the end of next year, but only if it makes sense to do so. There's zero interest in growing the operation for growth's sake.

Given the recent excitement around El Cubo, one might wonder why Endeavour didn't keep the El Cubo complex and try to make it work. It did try, from 20122019, but US$ silver prices were in the mid-teens/oz for most of that time. El Cubo was deemed too small to move the needle for a company that now has an EV of C$1.2 billion. (~28x larger than VanGold's).

Blue-sky potential from exploration and higher operating rates

There's substantial blue-sky potential for the combined El Cubo and El Pinguico project on at least two fronts. First, the PEA contemplates a 7-year mine life, yet (in my opinion) under the right circumstances, there's enough Indicated + Inferred Ag Eq ounces to support >7 years at 750 tpd or >1,000 tpd for 7 years.

The trick to (profitably) increase throughput is to only process ore that has minimal waste rock mixed in (in other words, avoid mining dilution). Second, if management can find higher-grade material at El Pinguico or El Cubo and work it into the mine plan, that would enhance production levels and project economics.

A big risk of moving a junior miner forward is access to capital. Here, VanGold is in pretty good shape. Upon closing a raise for gross proceeds of C$17M, drawing down a silver/gold loan for ~C$9.5M (in 6090 days), and satisfying the immediate C$6.4M cash portion of the C$19M acquisition price next month, there should be ~C$17.5M in available working capital.

C$17.5M would go a long way towards funding the total amount of upfront cap-ex needed (~C$21M) to proceed with the mine plan in the PEA, using mining contractors. The contractor alternative is estimated to be 42% cheaper in terms of upfront cap-ex than pursuing an owner-operated scenario.

The Mother Vein could be a company-maker .

The Veta Madre (Mother Vein) is a regional fault structure that hosts a world famous silver and gold-bearing epithermal system. This structure likely crosses VanGold's property at depth. Over several centuries, over a billion ounces of silver have been taken from the Veta Madre, and perhaps 67 million ounces of gold.

Where the Mother Vein (hopefully) comes into contact with the company's other vein structure, is an area that could host a sizable, high-grade deposit.

Just a few months ago, the Mother Vein narrative represented most of the upside potential in the VanGold story. Today there are a number of near-term catalysts that could be big events for the company.

VanGold's prospects have been BOTH enlarged and (somewhat) de-risked. De-risked by raising substantial funds, delivering a PEA and establishing a meaningful 27.6M Ag Eq ounce (Indicated + Inferred) resource.

Conclusion

As a larger company with a valuable mill, VanGold will have the opportunity to potentially consolidate nearby resourcesbut only if the price is right and the logistics are complementary to the company's prevailing mine plan.

For readers looking to increase their exposure to silver and gold (especially silver given current spot prices), choosing a junior like VanGold Mining (TSX-V: VGLD) / (OTCQB: VGLDF), with a strong management team and board, in a very good jurisdiction, that could be in commercial production this year, seems like a reasonable speculation to consider.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University's Stern School of Business.

[NLINSERT]Disclosures / disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about VanGold Mining, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of VanGold Mining are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned stock and warrants in VanGold Mining, and the Company was an advertiser on [ER].

While the author believes he's diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will be (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts and financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover any specific events or news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure:

1) Peter Epstein's disclosures are listed above.

2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the decision to publish an article until three business days after the publication of the article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.