There is a local casino just "up the road" from where we reside that we visit (once in a blue moon), small sums of pocketed cash in hand, to play a few favored slot machines to see if we can defy the house odds and come home winners. Called The Great Blue Heron Casino, we have nicknamed it "The Blue Goose," in reference to how one usually feels upon departure.

On occasion, we drive back "down the road" with smiling faces because we spat in faces of the Gambling Gods and actually came out ahead. However, the majority of the time, we limp home dejectedly, vowing never ever to return. Then, a month later, back "up the road" we go with yet another modest wad of the ultimate in "risk capital" to fire into the vice machines, forgetting all vows of abstinence and reformation.

Now, being that it is the closest casino to the large Asian populations of the Greater Toronto Area, the Goose is frequented by busload after busload of (predominantly) gamblers of Chinese descent or origin, cash literally falling out of pockets, who dash immediately in the direction of the exclusive "high-roller" sections. I have observed from afar elderly Chinese women sitting at a slot machine for hours, reaching into well-guarded handbags for $100 bills, which they deposit with orderly precision and astonishing calm. The robotic nature in which they perform these functions are almost religious in nature but alas, this is not the point of the story.

Last evening, I was about to sneak into the "Goose" for a fast $500 "cleansing" when I looked up to see one of those packed tour buses unloading passengers. What struck me as "odd" was that all of these (predominantly Chinese) people were wearing surgical masks. The last time I saw people wearing surgical masks outside of an operating theater was during the SARS epidemic, circa 2002, and in the category of "How Quickly We Forget," global markets were roiled by that frightening pandemic. So, with the arrival of a new strain of microbe known as the "coronavirus" now dominating the news cycles, it was as if a large bucket of ice water was dumped down my (and the market's) back.

I recall reading John Naisbitt's 1982 bestseller Megatrends: Ten New Directions Transforming Our Lives, in which one of the major new directions was the "mutation of the microbe." The explosion of world travel, with emphasis on the mass immigration of Asians to every other continent on the planet, has made the transportation and incubation of harmful, if not deadly, strains of bacteria a definite problem. It was identified by Naisbitt forty years ago in his book, as was the ascension of China as a global powerhouse, and it would appear that both premonitions have now been proven correct.

Amazingly, however, the impact of a potential negative impact on retail trade and tourism has been largely brushed aside, as investors seized upon Thursday's 200-point drop in the Dow as a buying opportunity and moved the tape from red to green in the last hour of trading, before the exchange closed mildly negative.

This brings me to the point of this discussion: Just as the 2008 sub-prime crisis began as a "contained problem" affecting only isolated financial institutions, it was only when it began to spread across all of the banking sector that things went south. Similarly, the outbreak of the Ebola virus in 2014 clipped the markets for nearly 10%, so events such as the coronavirus certainly carry the potential to act as catalysts for profit-taking (at best) and outright panic(at worst).

In early Friday morning trading, markets appeared to have made their judgment; this was an isolated event and certainly nowhere as severe as either SARS or Ebola, so line up your favorite cash-burning electric car company trading at all-time nosebleed levels and margin the living st out of it. That was before a case of coronavirus was confirmed in Chicago, and then the st hit the proverbial fan. As I tweeted out on Thursday afternoon, "Is this the catalyst for the next market correction/crash?" along with a picture of a microbe. It was exactly that, which set up Friday's reversal, and despite a valiant effort to save the weekly charts from an ugly red candle, the S&P closed down 30.07 points or 0.9%.

I remain cautious on the near-term outlook for stocks and have made a small bet on a decline, which I'll cover in the "Positions" part of the subscriber section. In the interim, precious metals prices are mixed, with gold and silver trying to maintain their uptrends. I remain a buyer of physical metal ahead of the miners because I am fearful that an overall market correction has the potential to cause a divergence between the two.

We love the Gold Miners (GDX and GDXJ) for their leverage to the upside, so powerfully evident during the Q3/2019 advance, but the Gold Miners are not exactly on fire right now and the underperformance of the HUI, plus the dismal performance of silver (and the GSR) this month gives me pause. I await a more optimal entry level for the initiation of unleveraged positions. But as far as options, futures and the leveraged Gold Miner exchange-traded funds (NUGT and JNUG) are concerned, I need a much better entry level before taking on risk. In two or three months I may look back with regret, but for now, my January strategy of caution has been working.

Gold prices are hugging the uptrend line drawn off the December lows, and in fact have finally, here on Friday, moved away from actually straddling that line earlier in the week. A move in February gold above US$1,580/ounce would suggest a test of the US$1,613 top, while a series of closes below US$1,560 would send it to US$1,525. Mind you, if the U.S. markets buckle under the coronavirus catalyst, gold will move sharply higher, and embolden me to action and away from caution.

You all know how much I adore silver. Most of the jewelry I buy as gifts and for personal use have always been silver. I actually have a sterling silver bathroom tissue dispenser in the master bedroom. Despite that last admission probably falling into the "too much information" category, I wince every time I look at Tesla in the mid $500s/share and silver sub-$20/ounce. I throw quote monitors from office windows in absolute outrage at the incessant illegality of the Crimex paper shenanigans that blackwash the silver "market."

However, even as a steroid-filled silver bull, only through advancing senility have I been able to harness this inherent optimism and see the tree-diffused forest; my beloved silver is failing to hold up "her end." Silver prices are not acting as the precious metals leader they became last July. And that is bad.

Before you throw this tardy missive into the bin, recall that in the very early stages of the gold breakout (June 2019), silver also acted in a "canine sort of way." Then, when gold gurus were calling for a 100 GSR (gold-to-silver ratio), I put out the now-famous "Short the GSR!" invective at 92.40 (within literally hours of the top)but not before taking huge flak and derision from not only the anti-precious metals battalions of Tesla-wielding, wild-eyed stockroaches but also (and with considerably more vitriol) from the gold bulls!

We may be in a stage of the Great Bull Market in gold that began on Dec. 4, 2015, at US$1,045, where gold leads and silver followhence the deteriorating GSR. What I am looking out for is a "slingshot trade," where the rampaging leader of a stock sector breaks out to new highs without any other sector members participating. People start to shout "Divergence!!!!" and sell both the leader and the other same-sector names, only to watch in horror as the leader rests and the followers suddenly explode higher. This is exactly what the silver metal and associated stocks did in the days and weeks after gold broke out above US$1,375.

To be sure, these are not easy markets to navigate and I, for one, am keeping my powder very dry, as my fear of a massive equity-market drawdown mitigates my precious metals ebullience. You will all recall, back in November, when I wrote that being "out" of my beloved Gold Miner ETFs (GDX and GDXJ) was actually more agonizing than back in March (2019) when they were down 12% and looking dreadful. Well, here we are in late January and I can tell you with total gums-exposed honesty that I am in the exact same state.

Bragging about an exit in the GDXJ at US$43 with it closing Friday at USD $41.79, is somewhat disingenuous, because we are a chip shot away from multiyear highs. That said, neither GDX or GDXJ has been able to take out the August 2016 highs at US$31.05 and US$49.37, which happened with gold trading at US$1,375.

So, with the metal now US$200 higher than the peak in 2016, either the miners are cheap, or the metal is rich, and therein lies my conundrum. I was trained many years ago by a brilliant futures trader that "lost opportunity is distinctly better than lost capital," which is closely mirrored by "when in doubt, stay out!" To be clear, I am 70% invested in physical gold and silver and a handful of juniors; I am flat the miner ETFs because holding stocks terrifies me. I am trying to position myself before the end of the month in more physical metal and/or the jettisoned Gold Miner ETFs. If a gun is placed "upside my head" forcing me to action, I'll opt for more silver first.

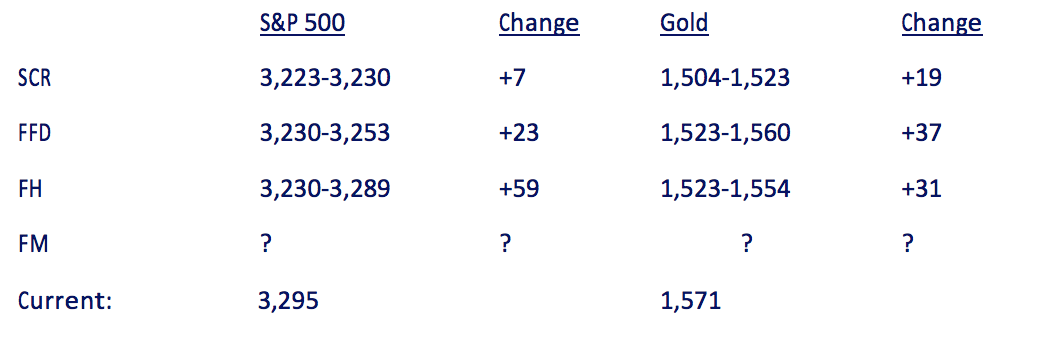

As we head into the last week of January, it is interesting to do the "January Barometer" (JB) analysis for stocks and for gold. Statistics show that as January goes, so goes the market for the rest of the calendar year. It is actually a tad more detailed than simply looking at the start and end levels for the S&P. The periods to be monitored are the Santa Claus rally (SCR) period (Dec. 24Dec. 31), the First Five Days (FFD; Dec. 31 closing priceJan. 8), First Half (FH; Dec. 31 closing priceJan. 15) and the Full Month (FM; Dec. 31 closing priceJan. 31 closing price). I like to do the same analysis for gold as an exercise only because gold is such a different beast so here we go:

As for the S&P, the JB for 2020 was in full "bull mode" with the SCR, FFD and FH readings all solidly positive, but with the late-week reversal, the S&P went out only 6 points above the FH close. Under the JB rules, stocks have to close out the month higher than the FH, FFD and 2019 closing prices, so if the big reversal on Friday sends the monthly close to under the FH close, then the JB is sending a mixed signal and the 2020 Trump Reelection Year may not go as swimmingly as one might have thought a week ago.

As for the JB for gold, with the close at US$1,571.90, things look decidedly better, as while the FFD close at US$1,560 was higher than the FH close at US$1,553, gold stands a very good chance of closing the month higher than the FH close, and that would be a huge positive for near-term performance.

The definition of the term "mixed emotions" is that it is the feeling one gets when that particularly hateful bullion bank trader drives your new Ferrari off a cliff. I have mixed emotions concerning gold because I have yet to buy the 2020 GGMA portfolio. As stated earlier, I am 70% long from purchases made in January 2019, but only 25% invested for new cash available for investment in 2020. Not to worry though, because I have a feeling that things will get resolved this week, for the better or for the worse.

With the coronavirus death toll having just jumped to 60% and now confirmed in Europe, traders in all markets are advised to beware the malevolent microbe.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

[NLINSERT]Disclosure:

1) Statements and opinions expressed are the opinions of Michael Ballanger and not of Streetwise Reports or its officers. Michael Ballanger is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Michael Ballanger was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts provided by the author.

Michael Ballanger Disclaimer:

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.