Standard Lithium Ltd. (SLL:TSX.V; STLHF:OTCQX) shares are caught up in a battery metals sell off, but is it warranted given recent positive developments, ongoing supply challenges in the Lithium Triangle and exciting near-term company catalysts? Its Arkansas Project could reach commercial production by 2022, and ramp up to ~20K tonnes/year of lithium carbonate, bolting onto brine streams from three existing facilities, to feed a central crystallizer plant by the mid-2020s. [A crystallizer is standard equipment made by multiple manufacturers, used in many commercial applications, to convert a solution into a solid material.] In this case, the solid material would be a high-purity, finished lithium product.

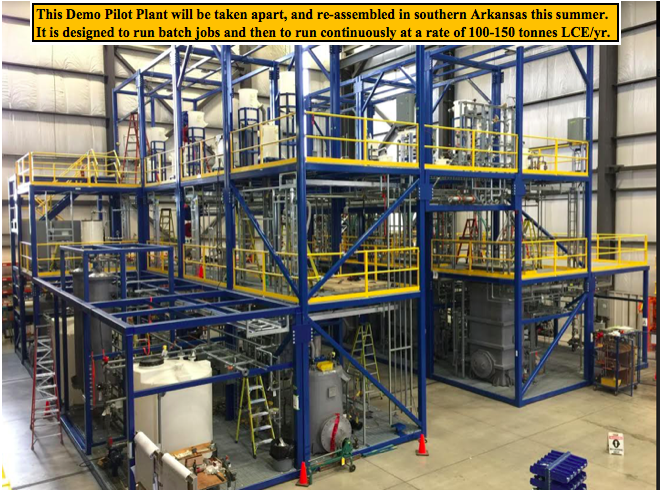

After successful bench and mini-pilot scale testing, Standard Lithium is at Demonstration Plant stage. The Demo Plant being constructed by Zeton Inc. is a 20m x 20m x 11m tall, industrial-scale modular facility designed to process tail brine from the Lanxess South Plant in southern Arkansas. Lanxess is a leading European specialty chemicals company with >15,000 employees in 33 countries. It develops, manufactures and markets a wide range of specialty chemicals and plastics. Last year, sales were nearly CA$11 billion.

The Demonstration Plant is based on Standard Lithium's proprietary technology that uses a solid sorbent material to selectively extract lithium. The plant is designed to continuously process a flow of tail brine at 50 gallons per minute from the Lanxess South Plant, equivalent to annual production of 100-150 tonnes lithium carbonate. The Demo Plant is designed to be expanded to commercial scale early next decade.

Dr. Andy Robinson, Standard Lithium President and COO, commented in a June 3rd press release,

"The Standard Lithium team is very pleased with both the speed of execution and the exceptional quality and attention to detail that Zeton are bringing to our Demonstration Plant. We are very confident that we will be delivering a high-quality plant to the project site in southern Arkansas, and we look forward to integrating it into Lanxess' brine operations. We are progressing very quickly on the ground, and hope to announce real progress in project implementation in the near future."

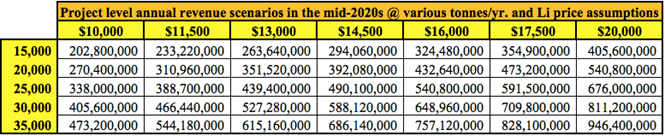

With all the doom and gloom around lithium pricing, even at current pricing of ~US$11.5K per tonne, 20K tonnes of lithium carbonate/year = US$230 million = ~C$311 million revenue at the project level. There are possible scenarios to produce up to 30K tonnes/year, for 25+ years by the second half of the 2020s. Subject to a formal JV between Standard and Lanxessin exchange for 100% funding of commercialization costs (hundreds of millions of CAD$ over several years)by Lanxess, Standard Lithium will end up with 30%-40% of the project. That's a win-win for both companies in my opinion.

I believe that lithium carbonate pricing will improve early next decade, perhaps meaningfully, as forecasts for the global electrification of commercial and passenger transportation and the deployment of large-scale energy storage systems, continue to rise.

On the other hand, long-term lithium supply is highly uncertain. Brine projects in Argentina and Chile are coming, but they're delayed due to funding and other challenges. Claimed project capacities of 20-40K tonnes of lithium carbonate/year may never be attained, look at Argentina's Orocobre Ltd., after four years, it's running at ~72% of nameplate capacity.

Of roughly 12 potentially viable brine projects in Chile and Argentina, I assume four won't make it and the other eight are delayed by an average of two years. I then pencil in a four-year ramp up period to 75% of stated project capacity. Under those assumptions, if 450K tonnes/year was expected from the Lithium Triangle in 2025what we might see, instead, is 225K tonnes/year in 2028! This means security of supply (from the U.S., Canada and Australia) will be of critical importance. Speed to market will be rewarded handsomely with long-term contracts at strong prices.

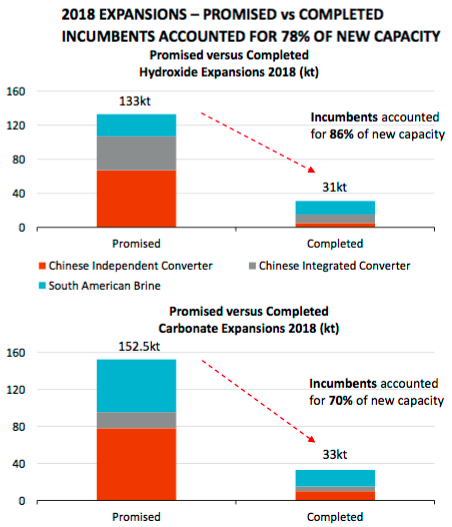

In the chart below we see a review done by Orocobre of 2018's expectations vs. reality, a combined 78% shortfall in hydroxide and carbonate expansions. 285.5K tonnes of new supply expected, 64K tonnes delivered. We see this year after year after year. . .when will the market catch on? This can only be good news for lithium pricing going forward.

Any lithium company, be it brine, hard rock, clay or "unconventional;" that can reach production by early next decade, will be in the driver's seat. I believe that Standard Lithium, with JV partner Lanxess could be in commercial operation by 2022. The Lanxess project has been de-risked in a number of important ways. I hope that readers and investors in lithium companies are starting to understand that risks avoided can add considerable value to a project. However, one risk still at large is technology and scale-up risk. With that in mind, I spoke at length with Standard Lithium's President and COO, quoted above, Dr. Andy Robinson. Robinson has 20+ years' experience as a geoscientist and has a PhD in Geochemistry. No one is better suited to be in the position he's in.

Peter Epstein: Please tell us about your background and what brought you to Standard Lithium.

Dr. Andy Robinson: I'm a PhD geochemist who worked in the engineering consulting world for 10 years, and then as an entrepreneurial project developer in the mining and power space for the last decade. Robert (CEO Robert Mintak) and I worked together at Pure Energy. When we took over management of Standard Lithium in the spring of 2017, we had a very clear vision of what we wanted to build. We took our experience in the lithium business, both in terms of modern technology and project development goals, and looked for the ideal project. The ideal project had to have:

- The right location for a modern approach,

- Existing infrastructure at the project sitenot hundredss of kilometers away

- The right partner,

- Minimal permitting & environmental risks, and

- A globally significant resource.

This was the only way we could realistically hope to get a project into commercial production within five years versus the usual 10 or more years.

Peter Epstein: How did your team choose a process technology to move forward with?

Dr. Andy Robinson: We took an agnostic approach to processing technology. The project drives the process. We started by understanding project fundamentals, then we developed a flow sheet that would work for our specific project in Southern Arkansas. Our process development work was guided by the philosophy that we didn't just want it to work in a labwe wanted a robust flow sheet that could work economically at commercial-scale.

Peter Epstein: Please describe the steps your team went through at the bench and mini-pilot plant stages.

Dr. Andy Robinson: At the bench-scale, we worked with large volumes of real brine from the projectwe then tested a whole range of different technologies, ranging from those already in commercial use, through to novel and experimental technologies, to determine which general "suite" of technologies would work best with our brine's characteristics. We quickly determined that a modern alternative to the types of technologies developed in the 1970s and commercialized in the 1990s would be the ideal solution.

So, we spent the time at bench-scale solving chemistry problems of selectively extracting lithium from the brinethen we ran two programs of mini-pilot work to build our understanding of the process engineering. One was done at a batch-scale, then we scaled that up and ran it on a continuous basis. Now, in June 2019, we've just completed two years of test work on our southern Arkansas brines.

Peter Epstein: What were the key takeaways from each stage?

Dr. Andy Robinson: At the bench-scale, we learned that direct lithium extraction from the tail brine using a highly selective solid sorbent was the way to go. At the mini-pilot-scaleusing both chemical and process engineers from a wide range of disciplinesallowed us to develop the simplest, most efficient flow sheet we could, at a reasonable cost. We're using equipment and processes already in use around the world, at very large commercial-scale, in complementary existing industries.

Peter Epstein: Please describe Standard Lithium's upcoming Demonstration Plant, what do you hope to achieve?

Dr. Andy Robinson: The upcoming Demonstration Plant will be final proof-of-concept for our Projectit's a large Plant, that can be scaled directly to a commercial facility. It's designed to process up to 50 gallons per minute of tail brine from Lanxess' South Plant, and produce at a rate of 100-150 tonnes of lithium carbonate per year, so about 10 to 12 tonnes per month. We hope to scale our Demo Plant up to 9,000-10,000 tonnes/year during the first phase of commercial execution.

Peter Epstein: If all goes as planned, Standard Lithium could be in commercial operations in 2022? 2023? Do you have a goal?

Dr. Andy Robinson: We're aiming for a commercial decision in the first half next year, and our goal is to be in commercial operations by 2022. I should add that 2022 is aggressive, but achievableas opposed to the aspirational targets suggested by other brine projects. Some of those projects are years away from a Bankable Feasibility Study, and then will require several more years to design, permit, win over local communities, obtain funding, construct solar evaporation ponds, regional infrastructure like roads, and build a processing facility.

Many companies are suggesting three-year ramp up periods to full capacity, but if history is any guide, it will probably be longer. So, Standard Lithium could reach initial commercial operations years before some, if not most, of the brine projects in the 'Lithium Triangle.' If true, we would hope to lock-in long-term contracts (through Lanxess) at very favorable pricing.

Peter Epstein: Might you be able to sell lithium output into specialty niche-markets that command premium pricing?

Dr. Andy Robinson: That's a great question. If one looks at Lanxess' business model, it centers around taking raw materials and converting them into a large variety of tertiary products that maximize the value obtained from their feedstock. They do these conversions using their global specialty chemicals expertise. Several niche lithium chemicals command high margins and typically are served by a small number of manufacturers. Lanxess is a leading global specialty chemical company, they know how to: a) build & operate a chemical plant, and b) extract maximum value from their chemical feedstock!

Peter Epstein: What would you like to say to readers who are still unsure about your operational flow sheet?

Dr. Andy Robinson: We think there's still a general misunderstanding in the lithium industry about lithium processing technology. There's a pervasive thought that evaporation ponds are conventional and therefore "safe," and that anything different is high-risk. In reality, each evaporation pond project is unique, each has initial, and ongoing, chemical & operational challenges; Orocobre is an example of taking the traditional approach and not delivering battery-quality, or nameplate capacity.

Interestingly, FMC (now Livent Corp.) has been successfully operating an "alternative" lithium-selective sorbent technology (similar to ours) in Argentina since the 1990s. Standard Lithium (TSX-V: SLL) / (OTCQX: STLHF) is not engaging in a high-risk processing technologywe're simply making incremental improvements to what has already been done successfully for decades.

Once people see our onsite Demonstration Plant in continuous operation later this year, I think perceptions will change as to our technology being unconventional. We don't have untested technology, we have customized technology, specifically designed with our project fundamentals in mind. The project drives the process. It took years of hard work and millions of dollars, but we think we're about to cross the finish line regarding proof of concept. That should turn a lot of heads.

Peter Epstein: I look forward to seeing that Demonstration Plant!

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University's Stern School of Business.

[NLINSERT]Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Standard Lithium, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Standard Lithium are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned shares of Standard Lithium and it was an advertiser on [ER].

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he's diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure:

1) Peter Epstein's disclosures are listed above.

2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Graphics provided by author.