A few nights back, a good friend of mine from Perth, Australia, e-mailed me an article skillfully written by someone from the firm of Goehring & Rozencwajg, in which the lead story was entitled, "The Bell Has Rung: the Contrarian Power of Magazine Covers." In this really good body of work was a magnificent flashback to a Businessweek cover that I actually cut out in 1979 and had Xerox'd and mailed to all of my clients (numbering 27) by the following weekend.

It was a Businessweek cover that had on it "The Death of Equities," and as it was within literally three years of the beginning of the greatest bull market in stocks ever, it also marked the top of the "non-equities" cycle, whose main component was the commodities sectorled, of course, by gold. The firm juxtaposed their review of the 1979 article against the recent April 2019 Bloomberg Businessweek cover page entitled, "The Death of Inflation," in which the authors point to the myriad of reasons why inflation rates are declining and why they will continue to decline. The implied conclusion is that one should avoid inflation hedges (like gold and silver, and to a larger degree commodities) and instead stay with stocks and bonds and live long and prosper.

It was a wonderfully written article. After I calmed down and got down from the table upon which I was jumping, I found myself in conflict. Upon the conclusion of the fourth reading, it hit me. As much as it had me cheering from the sidelines that finally we were overdue for a bona fide commodities cycle, I found myself glued to the frailties of the thesis.

The article "The Death of Inflation" is, in a word, wrong. It assumes (and asks you and I to assume) that the published "inflation rate," which emanates from the U.S. Commerce Department and excludes food and energy, is a solid number. I submit to all of you that the published "rate of inflation" is nothing but rubbish. It is a contrived, fabricated number designed to, at first glance, placate the masses. Far more importantly, it placates the investor class and cajoles them into believing that the rate of producer and consumer price advances is "muted," thus justifying ownership of U.S. Treasuries and common stocks.

Let me give you a classic example of the hidden effects of inflation. You have all noticed how supermarket items have masked price increases through reduced volumes. The 10-pack of Ivory soap is today priced a tad higher than in 2010 but each bar of soap has been reduced in size by around 30%. That is inflation.

A better example is the marina where I dock my boat in the summer. In 2014, when we first joined, there were a number of perks, including Wi-Fi, free newspapers, complimentary coffee, and cable TV hook-ups. Dockage fees have risen around 10% in a five-year time frame but gone are all of the amenities that made one content to pay premium dollars to become a member. That, too, is inflation.

The slow creep of these cuts is also seen in the real estate market, where lot sizes are the size of postage stamps while running water is considered an upgrade. Everywhere you turn, you see a carefully contrived pattern where whatever the bankers have in inventory or pledged as collateral against their mortgage book is inflating while all of the traditional inflation hedges (such as commodities) are deflating. That is "targeted" inflation, and make no mistake, it is the continuum of interventions that are training the investor class where to place their bets.

Whenever I read an article that tries to draw a parallel between today's markets and virtually anything prior to the election of Ronald Reagan (and appointment of Alan Greenspan), I am forced to ignore the assumptions. The assumptions to which I refer are those that choose to discount the interventions in day-to-day trading as a rationale for supporting the conclusion. If the published numbers surrounding what constitutes our "cost of living" are frail, frayed and flawed, how, pray tell, is one able to model a "real" rate of return (ROR)? How, when the risk-free rate of return (typically the 2-year US Treasury) is being clouded by a rate of inflation that lies between "corrupted" and "connived?"

There is nothing more sobering than doing one's bookkeeping. When I am forced to sit down and go through all of the statements and all of the tax returns and every single trade in any given tax year, it is like putting a volume accelerator in each of my ears and then screeching fingernails down the entire length of a blackboard over and over and over again, all the while playing a Barry Manilow album in the background. Nothingrepeatnothing sends me into madness more rapidly than looking back upon trades or deals or drilling programs that have dominated my portfolio especially over the last five years, because what always begins with optimism and excitement, has tended to devolve into pessimism and boredom.

When we are finally able to look back upon the 20092018 era of "buy the f---ing dip" methodology, with financial assets in complete and total meltdown and hard assets in early-stage, hard-fought acceptance, very few of us have the energy nor the tolerance to rise up on any sort of soapbox and claim victory. What the bankers have done, with the aid of regulators and elected officials, has been nothing short of criminal, but in the court of public opinion, they gave the younger generation a glimpse at "controlled" (as opposed to "free market") capitalism. Now we have all of these Millennial and Gen-Y traders swooping in and out of markets like birds in a marsh at sunset, and all that matters is that the "system" remains intact and the banks remain solvent so that the campaign contributions will continue to flow and the status quo is allowed to prevail.

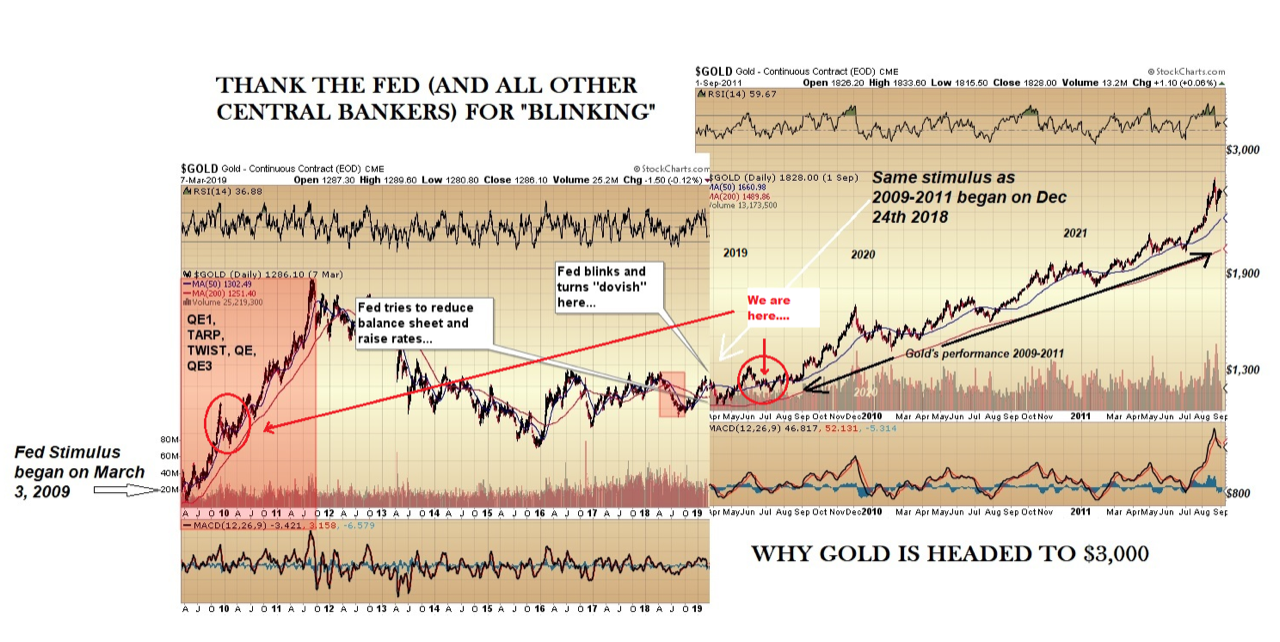

I continue to proffer the thesis that gold (and that ridiculously underpriced stepchild silver) are in good shape technically, with relative strength index (RSI), moving average convergence/divergence (MACD), and histograms all trending higher but nowhere close to even mildly overbought. The graphic below lays out my 20192021 thesis, as I believe the late 2018 "pivot" by the central bankers was a carbon copy of the one that occurred in Q1/2009. If investors wade into the precious metals in the second half of 2019 the way they pounced in Q3/2010, they will be doing so with an additional $9 trillion of credit creation as armament for the assault.

It is important to recall that in 2010, the investing public was still reeling from the all-out devastation wrought upon them by the bankers, and did not have nearly the liquidity then that they have today. Yet, in the final analysis, forecasting gold's direction, amplitude and timing is an exercise in handicapping the odds in the same manner that you try to predict the outcome of a horse raceand as everyone learned too painfully from this year's Kentucky Derby, you can pick the horse and still lose all of your money if someone intercedes and disqualifies the winner. That is exactly what has happened to investors in gold that correctly predicted the monetary and fiscal turmoil that unfolded in 2009: They picked the right horse but the central bank racing stewards disqualified it in 2011. Total, complete, unadulterated disqualification the likes of which we are encountering here in 2019.

You really cannot imagine what is was like to be writing about the events leading up to the $1,900 peak in gold prices in 2011. Many of us had the move absolutely nailed and that included the top in silver in April 2011. At the time, I was buying a friend of mine a one-ounce silver birthday gift at Scotia-Mocatta in downtown Toronto, and as I walked into the bank, I was surprised by the line-up, which included no fewer than perhaps thirty people. Sales staff equipped with pens and clipboards moved up and down the line asking, "Buying or selling?" followed by "Gold or silver?"

But what grabbed me by the throat was that every single answer was "Buying!" and then "Silver!" That week, silver had approached $45/ounce, having advanced from $25 in late 2010, and I remember calling my good friend, who ran a superb blog called "The Fundamental View," warning him to scrap his plans for a bullish report on silver due to hit the blog that weekend. It was within literally days of the top in silver at $50, and while it was a fairly easy call based upon the unanimity of opinion (by those that normally lose money), the violence with which it occurred evoked the same emotions as watching the Zapruder film years after the JFK assassination.

It was a blatant, criminal, orchestrated intervention by the Crimex racing stewards; they decided that Silver Streak was not to be the winner, so they disqualified it in favor of StockRoach. Down went the precious metals in April 2011, and up went the S&P500, all because of the importance of deflecting attention away from sound money and toward financial "assets." The interventions of April 2011 will remain forever etched in the collective psyches of precious metals investors the world over, and the long-term generational impact is still looming large eight years later.

The Q2/2009 correction in gold was an AprilJune event that was the precursor to the move from the mid-$800s through $1,100 by the end of the year. If I am correct, that is exactly where we are today, only the 2019 lows have seen three assaults of $1,267, and all three have been soundly rejected. It evokes memories of December 2015, when gold probed the $1,045 level before being soundly rejected, then exploding higher for the next six months.

I am accumulating gold and silver here in the spring of 2019 not because of the "Thirty-Five Reasons to Own Gold NOW!!" e-mail blasts nor the interviews with billionaire gold bugs who have now been wrong since 2011. I am accumulating gold because it is ridiculously cheap as measured against the inflation spoken of earlier in this missive. To "inflate" is to "blow up" or "fill with matter" or "make full," as in a balloon or a series of blood vessels connected to an organ or the amount of "currency in circulation." But whatever the intended recipient, it is a purely "relative" event because, unlike a tree that inflates through organically created matter that stays for hundreds of years, monetary inflation is at once both temporary (in that it can be removed by central bank "RePo" operations) and static (in that, like a tube of toothpaste, once squeezed, the paste is impossible to return to its vessel).

The world in which we all dwell is at once both difficult and wondrous, in that those who have been living in the Western World of lifestyle advancement and luxury are now frightened by the arrival of others of our species who would covet the same. However, what we all seek as investors is not a title nor a moniker nor a reference number; what we all need is the assurance that we are all investing and trading under the umbrella of "free markets," and absent the hovering, scolding, finger-wagging of a seemingly entitled member of the elitist class. If any of you revered readers can offer me some insight, please do. ([email protected])

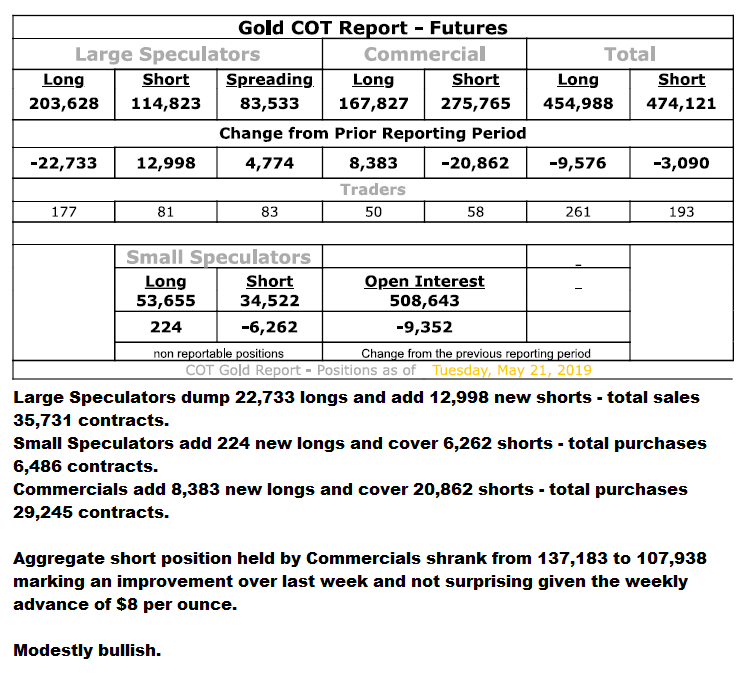

COT Report

They sold the crap out of it last week at $1,300; they covered it all this week at $1,270. They pocketed $30/ounce on nearly 30,000 ounces, and that is a US$90 million payday, no matter what you say and how it sounds.

To my fellow gold and silver bulls I say this: When I was inhaling the KoolAid at $857 gold in 1979, I was a 26-year-old freshman in the space. When I was selling silver and gold near the top in 2011, I thought I was a "veteran," but I did it for all of the wrong reasons. When I went bullish at the seven-year lows in December 2015 at $1,050, I was pounding the table. Every trade I make is constructed on the basis of history, and what I believe to be true today is that this love affair with central banks and financial assets is coming to a thunderous end. It will probably take a two-year advance in gold, to test the all-time highs, to convince the Millennials to get on board, just as it did for them to inhale the Bitcoin story. When this all happens, there will be nary a party, nary a tribute, and certainly nothing resembling a celebration. The interventionalists will be grasping at anything resembling a "control string" to regain the reins of order in their petty little arena of Pavlovian indoctrination and training.

Take heart in your research; take solace in your resolve; and take courage in our collective convictions. Our day is very, very close.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

[NLINSERT]Disclosure:

1) Statements and opinions expressed are the opinions of Michael Ballanger and not of Streetwise Reports or its officers. Michael Ballanger is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Michael Ballanger was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts and images provided by the author.

Michael Ballanger Disclaimer:

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.