There is one redeeming benefit to writing "forecasts": they invariably and inevitably reduce you to a quivering mass of humility as the hubris born of luck and circumstance is replaced with the reality of randomness. I have been reading research reports for years and the most useful portions are those where an analyst goes back and reviews his/her reasons for owning something, and then a year later explains why it was flawed.

Interestingly, it is uncanny how random events otherwise known as "black swans," which carried computer-generated probabilities of occurring in the single-digit-percentages, are by and large the most common reasons for an investment theme blowing into smithereens. Accordingly, as I gaze out into the year 2018 and see all of the attendant risks so very well documented by the most revered investors of the past half century, I have to sweep them all under the proverbial rug because at the end of the day. What we all witnessed in 2017 was truly historic. The quantitative easing that is now credited with having "saved" the financial system in 2009 involved global central banks first creating money out of thin air, and then using that money to initially buy bad bonds, then good bonds, and then finally stocks in order to remove toxicity from member bank balance sheets and to increase the supply of money.

The problem with that is the central banks didn't create "money" out of thin air; they created an unprecedented quantity of debt (to the order of several trillions). As you have all read by now, the rescue mission embarked upon by Paulson, Bernanke, Draghi, Kuroda and Company was deemed "the largest financial experiment in global history," in that it was alleged that nobody would or could forecast the outcome in terms of economics. Alas, as true as that was, there were more than a few investors who would, and did, forecast the outcome of that massive money-printing fiasco in terms of asset prices and purchasing power of currencies. The simple result was a serial bubble in all things noncash.

"Never underestimate the replacement power of equities within an inflationary spiral."

I first heard that statement in 1979; I have been writing about it for decades; and I have repeated it every few months since the Great Financial Crisis of 2007-2008 came to an end with the S&P 500 approaching 666 in April 2009. The "inflationary spiral" referred to is "quantitative easing" (along with twin sibling TARP) because there is nothing that depicts monetary inflation better than the indiscriminate fabrication of liquidity around the world since 2009. Vast pools of liquidity sloshing around the trading floors and in the derivatives pits derived from a palpable desperation that was incubated by the unbridled greed of bankers. Under the guise of "saving the system," the global moneychangers saved only their cumulative net worth and retirement funds residing in their precious bank stocks. The "system" was fine; business was being transacted; crops were being grown; bills were being paid; and children were being educated. These transactions could not be quantified by the Wall Street Journal or on a Bloomberg terminal so they had zero effect in creating any offset to the panic being generated by very quantifiable losses in bank (and other) stocks. The financial economy was saved but the integrity of the fiat currency regimes around the world were (and are) disintegrating.

As I have written about many times this year, the emergence of Bitcoin and other blockchain technologies is the ultimate repudiation of cash as an asset class. All-time record highs on the S&P and the NASDAQ are further testimonials to the vileness of holding cash in a savings account, while the disappearance of the fixed income yields so necessary for retirement savings accounts have forced octogenarians into technology stocks as a means of protecting purchasing power and generating income.

By buying all of the income-producing bonds after the 2007-2008 meltdown, the price managers in the ivory towers removed all of the much-needed supply that would historically compete with stocks for investor money flow. The net result was a bottleneck of demand for stocks, with all of the trillions of bond market dollars and yen and euros diverted away from the safety of fixed income and into the chaotic vortex of algorithm-controlled equity markets, forcing valuations higher and higher with each passing month.

This is the Crime of the Century and it is my personal belief that 2018 will be Year One of the Great Reckoning. The propeller-heads on Wall and Bay Streets will go on CNBC and BNN and talk about "rebalancing" and "sector rotation" and "alpha" and "beta," but what they won't tell you is that when the plug is pulled from this bathtub full of rampant speculation and wild-eyed greed, none of those fancy catchphrases will save their clients from cataclysmic losses and the kinds of drawdowns in personal wealth from which there is no return, save a lottery win or messianic intervention. When that sullied financial bathwater begins to escape its turbid tub, there will be no quantitative easing or TARP to save investors; the bankers will have their gated communities and private island sanctuaries within which to ride out the storm while the public is left cold and naked on the bathroom floor.

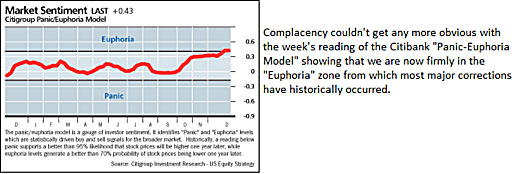

The market tops of 1929, 1969, 1987, 1999 and 2007 all had one thing in common: The asset class called cash was the singular most-hated asset on the planet. Portfolios were bereft of any significant cash levels such that when stocks began to swoon, there were few buyers providing support. As for sentiment, throughout most of 2017, professionals were in the nowhere-zone of "cautiously optimistic," which explains the sentiment readings in the chart provided below.

However, in the last quarter of the year, as records tumbled and the mania took hold, investor sentiment readings were flashing a major warning signal. Or were they? This rush to jettison fiat in favor of anything non-fiat is perfectly understandable given the insanity of the central bank balance sheets expansions. The big question for all of us is this: What event or series of events will conspire to reverse the rush from cash to a rush to cash? More importantly, will we be able to move nimbly enough to avoid being caught in a liquidity-squeeze maelstrom, as tens of millions of investors all clamor for the exits all at once? These are the major issues for me as we enter 2018 in light of stretched CAPE ratios and technically overbought conditions.

One of the bright spots for me was the manner in which gold and silver ended the year, with the gloom of late November being replaced with a sizable mid-December rally that was, notwithstanding the fact that I am now long 100% of the NUGT and JNUG ETFs discussed in early December.

On December 10, I wrote: "Accordingly, the proper action for me will be to add to positionsslowlywith the JNUG and NUGT ETFs containing maximum leverage (and risk) in advance of the 'turn.' For the retirement account, I will stick to physical silver (no leverage) and for the taxable accounts, I will move next week to accumulate an additional position to the tiny option purchases made the week of November 27. Remember that we still have tax-loss selling to get through, so the optimum acquisition period should be the last two weeks of Decemberunless, of course, the big money decides to preempt the retail bargain hunters, which I view as a distinct possibility." I am now long one of my biggest call positions ever in the ETFs, with average costs on the NUGT Feb $30 calls at $2.78 (now $4.00), and the JNUG Feb $15 calls at $3.06 (now $3.75).

I see another $50 upside in gold before the end of January, and another $2.80 in silver and a GTSR (gold-silver ratio) at 70. If I see $1,360 gold by my "Milestone Birthday" on February 16, (also option expiry day for every option I own), I presume that money flows will have the two Gold Miner ETFs challenging at least a couple of the highs seen in past rallies. Those highs are a great many points above where we closed out 2017.

Risk Management

One of the most difficult things to do, each time I put on a trade, is to take a loss. Why is it that I find using stop-losses so difficult? Gerald M. Loeb wrote one of the finest books ever in The Battle for Investment Survival, and in his masterpiece (second only to Jesse Lauriston Livermore's Reminiscences of a Stock Operator) he clearly says that one should use a "10% Rule" in managing drawdowns. Loeb and Livermore traded in the days of stone knives and bearskins; we trade in the days of artificial intelligence and algorithms. They enjoyed the wonderment and purity of free markets; we have to navigate government and Central Bank Intervention. They had despots like Hitler and Stalin; we have despots like Bernanke, Draghi, and Abe.

So the next time I want to be lectured by someone about risk, let it be Ray Dalio or Stanley Druckenmiller, or perhaps even Eric Sprott, who have had to cope with the insidious interventions of governments. I do not want it to be some Millennial podcaster explaining the reasons why the "mantle" has been passed from semi-senile Boomers to the "New Regime," techno-savvy French Foreign Legion of stock market geniuses all because it is "truly different this time." From this septuagenarian scribe, a forty-year veteran former "registered advisor:" Trust this: In today's world, stop losses are useless. So are the words of your "wealth management professionals," who would have you believe that "over time, rebalancing will smooth out your returns." Whenever your returns are subpar, wait for the buzzwords like "rebalancing" or "asset rotations" or "long-term adjustment." They will be the clarion calls to fire your advisor. Especially the fee-based advisors. What made their clients comfortable in 2017 will make them antsy in 2018. What worked last year will not work in 2018; you can bank that along with your bitcoins.

No forecast issue is complete without a comment on the base metals, and since Dr. Copper is the king, the ten-year chart looks spectacular. However, the RSI at 72.96 is screaming overbought, so chasing the base metals equities in here would be a tad risky. Nevertheless, it all comes down to the mighty U.S. dollar and monetary policy; if interest rates are allowed to rise in reaction to heightened inflationary expectations, the USD will rise creating a headwind for all USD-denominated commodities (including copper).

Since the converse is also true, one has to question the resolve of the central banks in that regard when you factor in how much interest must be paid each month on the massive amounts of new debt created since 2009. From my standpoint, I see no reason to expect any change in policy that will cause a cataclysmic drop in economic activity. Ergo, continued weakness in the USD versus the international basket of similarly worthless fiat currencies will create a tailwind for the metals, and for Dr. Copper as well. Long-dated call options on Freeport-McMoRan Inc. (FCX:NYSE) after the RSI comes down into the 40s from the current 80 level would be welcomed.

Finally, in keeping with the copper correlation theme, no discussion of precious metals could be complete without mentioning silver. Silver has been the widowmaker (or "divorce-maker") for many investors since 2011, when it peaked out at around $50 per ounce. There is an old expression that says that "silver investors are gold investors on double steroids!" I know this to be true from my speaking engagements, and from attending the various investment conferences around the globe and observing the many different characteristics of the crowd.

Serious gold investors, as a group, are generally a sophisticated, well read and highly educated breed of investor, distrustful to a degree of establishment methodologies and practices. They are generally askers of well-researched questions and are quite knowledgeable in the area of basic geology and exploration. Over the forty years of being a gold investor myself, I quite prefer the company of a gold investor to that of a stock jockey or a techie. The former tend to dwell on "crushing the competition" with a "killer trade," while the latter lose my attention within fifteen seconds of opening their 200-IQ mouths. Gold investors can usually tell you who is leading the NHL in goals or which NFL teams are in the hunt for a wild-card berth in the post-season, and can quite often tell you which one of the Two Hands Shiraz wines won awards in 2014. They are an interesting crowd, by and large, and I quite enjoy them.

Serious silver investors are a vast chasm of difference to their gold counterparts. They are usually not as well-spoken nor as educated, and they are not askers of well-thought-out questions, but more "tellers" of random data points. In fact, they are "yellers" of factum related to government conspiracies, military psy-ops, Lee Harvey Oswald and alien abductions. As opposed to the business casual dress code of the gold investor, the silver investor is usually seen in military fatigues, unshaven, in need of a haircut, and usually wearing a T-Shirt with the likeness of Che Guevara or Jimi Hendrix on the front. In the 1990s berets were commonplace, but have recently been replaced with baseball caps with SWAT emblazoned on the brim. Topics of conversation, where there is actually a rare interchange of ideas and information, tend to focus on extremesas in the "complete collapse of Western civilization" or the "removal of the U.S. dollar as a medium of exchange," but always and without fail, the inevitability of the confiscation of their silver by government. On this last point, of someone taking away their "stack," faces redden; saliva pools at the corners of mouths; eyes bulge; and respiration and heart rates elevate as if they are under physical attack. As unflattering as these exchanges tend to render them, I respect these patriots for their passion and their undying certainty that Donald Trump is really a Vulcan with his ears trimmed.

I own physical silver in retirement accounts, and in the taxable accounts, I have a combination of silver shares and ETFs. I abhor the stranglehold that the Commercials have had on the silver market for what seems like an eternity. But in recent weeks, the COT report is revealing a gradual shift in positioning by the bullion banks that just may lead up to a move through the all-critical $20 level.

While the possibility that any breakout above $20 would be met with a bullion bank assault, it was only a few years ago, in mid-2010, that they got caught with their pants down when silver finally broke out, giving investors are $50/ounce print in early 2011. That assault in 2011 was soundly rebuked by the global bankers, and by April 2013, it was down under $30 and on its way to the December 2015 low at $13.87.

Luckily, the fiat police have got their hands full with the legions of Millennial cryptojunkies springing up everywhere in fiduciary protest against this global currency debasement, so silver in 2018 may represent less of a bull's eye for the regulatory rangers as they draw beads on bitcoin and its thousands of phony, fabricated brethren. I see a move back into the $20s in the first half the year, after which we will have to reassess because it has been proven exceedingly difficult to game a market as thoroughly rigged as silver. My only hope is that the price managers and algorithm designers at 33 Liberty St. in New York are too busy trying to lasso the cryptos and leave silver alone as a "lesser evil."

With the Internet now a massive source of investment knowledge, opinion and deception, you will soon be reading voluminous tomes of "Get rich quick!" emails designed to liberate you from your hard-earned savings and critical investment capital. The quote I inserted above is really all one needs to know about asset prices in the years ahead. The Fed will have a new chairman in 2018 and the critical question is "Will the punchbowl be drained in 2018?" For the past nine years, there has been an injection tube feeding the financial punchbowl with all manner of fiscal and monetary stimuli, which has kept all of the bank collateral (real estate, stocks, bonds) afloat despite massive debt and swamping entitlements obligations. The Fed has stated that the tube is now shut off as the tightening cycle has begun.

But, if inflation rears its ugly head and it causes civil discontent, the tube will not only be removed, the plug at the bottom of the bowl will be removed and the contents allowed to drain. Food prices, rents and health care will be the barometer by which policy pitchforks and torches are trotted out, so keep your seatbelts securely fashioned in the New Year and stay alert. Draining punchbowls do not permit rising stock markets and rampant speculation.

2018 will be an interesting year.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger's adherence to the concept of "Hard Assets" allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Disclosure:

1) Michael J. Ballanger: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: None. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies referred to in this article: None. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures are below.

2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Streetwise Reports does not accept stock in exchange for its services. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article.

All charts and images courtesy of Michael Ballanger.

Michael Ballanger Disclaimer:

This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.