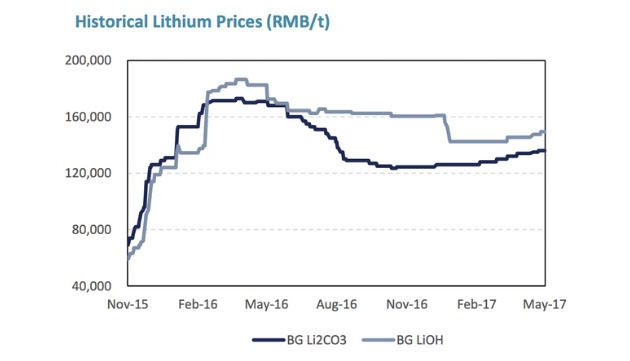

It has been relatively quiet around Nemaska Lithium the last six months or so, after it started construction on the Phase I plant and completed several early stage parts of the Whabouchi Mine, besides looking for capex financing packages along the way. Although lithium product prices held up very well at relatively high levels and are even slowly rising again:

Source: Galaxy Resources/CJ Securities

Source: Galaxy Resources/CJ Securities

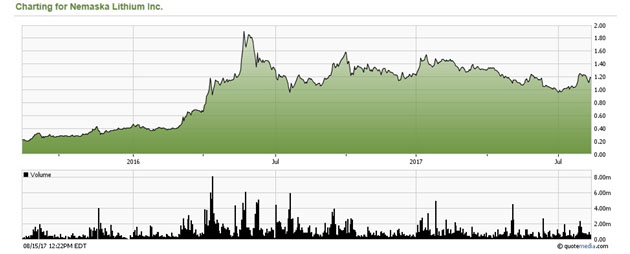

the Canadian stock market sentiment turned a bit soft/neutral, so an advanced and permitted lithium development story looking for major funding often doesn't get the most love from investors in this kind of climate, as can be seen in this chart:

Share price 2 year period

Share price 2 year period

However, Nemaska Lithium isn't sitting on its hands as far as funding goes, and recently managed to raise another C$50M @ C$1.05 again through a short form prospectus, supported by many institutionals. Proceedings will be used for further development of the project, and is in effect another equity part of capex. Together with the first raise, Nemaska now has raised $100M in equity for capex, which is the majority of the equity part of capex. This counts as a material development in my book, so I felt it was time to do an update, and what is a better means for this than a Q&A with CEO Guy Bourassa, to discuss this and various other things of interest.

TCI: Thank you Guy for taking the time to participate in this interview. It looks like the stock is suffering from the waiting game for capex funding here, but I believe this could be a blessing in disguise for new investors at this stage. What is your opinion on this, and could you elaborate why?

GB: I believe that the stock will begin to reflect the value that we have created in the company over the coming months. Over the past twelve months we have produced more than 1100t of concentrate at 6.2% Li2O, and built and commissioned the Phase 1 Plant so that we can produce battery grade lithium hydroxide samples for customers globally starting in September. In addition, we have also delivered 8.7t of lithium hydroxide to our first customer, Johnson Matthey. At the same time, we have raised $100M in project financing, which has allowed us to make tremendous progress on construction at the mine site and advance the detailed engineering of the commercial Hydromet, so Nemaska Lithium today is a much different company than it was just one year ago. We have made great advancements in executing on our plan to become the next lithium salts producer.

Whabouchi project: concentrator building

Whabouchi project: concentrator building

TCI: You just closed the $50M financing, which was great, no discount, no warrants. However, I am not a big fan of short form as it could create immediate pressure. Why did the institutional who bought this stock insist on short form?

GB: We opted to do a bought deal using a short form prospectus offering as it allowed us to offer the deal to a wide variety of investors including important institutional investors as well as retail investors. The bought deal structure usually allows for better terms and doesn't put pressure on the stock. Nemaska Lithium has a large shareholder base and this type of offering enables the largest audience to participate. Also, I dont see this as having an immediate pressure on the stock as this offering was not a unit offering and so there was no warrant to give an investor an incentive to sell the stock and hold the warrant to limit the risk. Anyone who took a position did so to take a position in the stock and had a long term view.

TCI: Could you disclose any of the names of the institutionals who participated?

GB: We do not disclose our investor shareholder base, unfortunately; you could consult Bloomberg for a public list of investors. I will say though that we have been able to attract extremely large and credible institutional investors globally.

TCI: What are you planning to do with this cash; could you break it down for the audience?

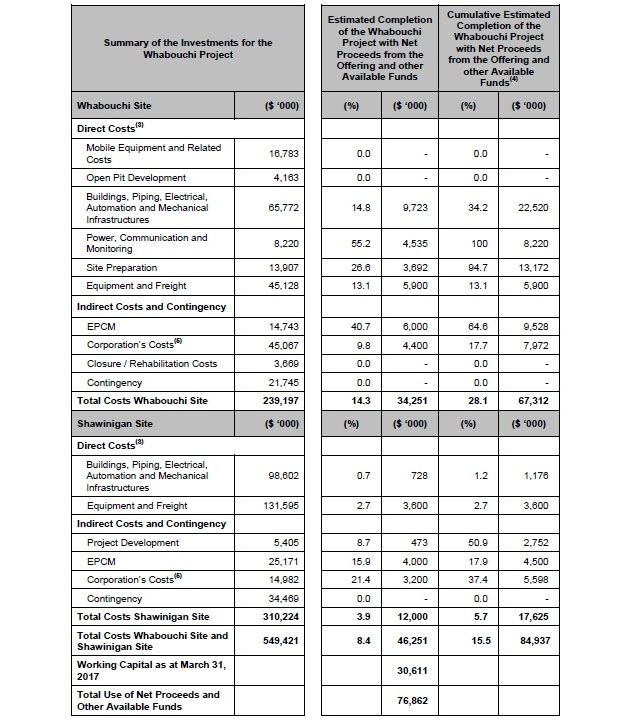

GB: We are continuing ongoing construction at the mine site, procurement of major equipment, as well as detailed engineering of the Hydromet plant and identification of long lead items and critical supplier negotiations and delivery schedules. In the prospectus of the last offering you can find a table describing expenditures with proceedings.

TCI: This table is shown here, plus notes, in order to get a better picture, and can be found on page 9-11 in the prospectus (on SEDAR):

TCI: We discussed earlier the promise of state-owned Quebec Ressources committing to $75M in debt as a backstop after private parties funded the rest of capex first. Do you have a public document of this promise, and how does this work, will this debt be first or second lien, any idea of interest rates?

GB: We are in active negotiation with private lenders. We don't have a public document on this, and Quebec is involved in these discussions and will have the same terms as the private lenders.

TCI: Do the banks involved in capex funding need any milestones, more off-take agreements?

GB: Lenders have indicated that they would like to see initial production of lithium hydroxide from Whabouchi concentrate being sent to customers from the Phase 1 Plant that we are on target to deliver in September. We currently have offtake agreements for approximately 50% of our commercial product and lenders have indicate that these offtake agreements are enough to satisfy their due diligence requirements. We remain very bullish on the price of lithium and would prefer to continue offtake negotiations once we have finalized our project financing, putting us in a stronger negotiating position with a clear production timeline.

Whabouchi project; bulk sample location

Whabouchi project; bulk sample location

TCI: Are you willing to disclose a timeline for capex funding?

GB: The capex funding is our current top priority and we are working to close it as quickly as possible. The mine has construction and commissioning timeline of 9 to 12 months and the Hydromet plant is 18 months construction and commissioning once financed.

TCI: Let's have a look at the discovery and integration of the Doris Zone. This was found during pit outline drilling at Whabouchi, what are your plans with this? Surely you are not going to change the FS economics anymore as the current resources are more than large enough, and you are in the middle of capex funding talks.

GB: Correct, we are focused on the project financing. There is no pressing need to update the feasibility given our life of mine is currently 26 years. Investors should view Doris as a bonus.

TCI: We briefly discussed the flow sheet. A 6.2% concentrate is already being produced through the Phase I Plant involving the DMS process, which is roughly about 2/3 of production. Besides this, a flotation part is also necessary to recover the other 1/3 of production, and this is being done at Lakefield, one of the most recognized third party processing and testing firms in North American mining. The plant building in Shawinigan is partly filled at the moment with parts of the flow sheet process. Can you explain what will happen when the mine and plant is at full commercial production capacity?

GB: We plan to produce 28,000t of LCE. Our line is fully flexible to produce both lithium hydroxide and carbonate. We will also consider selling concentrate if the price of concentrate continues to be strong and our margins looks healthy.

TCI: What parts of the flow sheet need a bigger scale, and which ones need multiple elements, more of the same?

GB: The electrolysis section is at scale and each module is autonomous and will only require additional electrolysis modules to be added to reach full capacity. The balance of the plant such as the kiln, dryer, crystalizer, etc. will be larger than the current Phase 1 Plant 1. This is off the shelf equipment and will be purchased at the appropriate size for the commercial facility. The impurity removals section is largely a series of tanks that are easily scaled and will require modifications to the chemistry to remove impurities at a larger scale.

TCI: I see you have hired quite a bit of new staff. Do you believe the company is ready now to take this to production, or do you need more people?

GB: We have optimized our structure and filled key positions already with extremely experienced people who are well qualified for their roles. Nemaska Lithium has adopted a participative management philosophy, which supports an autonomous decision-making process at all levels. Participative management is at the center of our culture of accountability, creativity and innovation that is demonstrated by all of our employees. I am extremely proud of our teams and their capacity to deliver in such a fast paced and dynamic environment. We actually simplified our structure by taking out the VP Operations position, as this was the result of the first blueprint for our organization made by consultants and was useful for bringing the Phase I plant into production.

TCI: Another interesting thing I hear quite frequently is the possibility of a takeover by, for example, Galaxy Resources. Are you open for a takeover at the usual premiums at all at this stage, or are you and the large shareholders in this for the big exit at production stage? Could you disclose anything on this subject?

GB: I cannot comment on rumors as to a potential takeover or partnership with Galaxy or others. We are open to discussions with others, of course, but I would only consider this after we have executed on our plan to build the mine and Hydromet plant. I believe that the value for our shareholders will have increased significantly by that time.

TCI: I believe Nemaska is an excellent investment opportunity, since the post-tax NPV8 of Whabouchi is $928M, which is C$1200M, which in turn is 2.65 times the current market cap of C$452M, and most equity is already raised. With more equity raised for capex, say $100M, the total number of shares outstanding comes in at about 500M. This means when Whabouchi would go into production, and we assume a conservative P/NPV ratio of 1, that the hypothetical corresponding share price could be C$2.4. What is your comment on this, and do you have other ambitions in this regard?

GB: I think this is still very conservative. Once in commercial production I think we should be valued on an EBITDA multiple at 10 to 15 times EBITDA as a chemical company. We believe that at our nameplate production we should be close to C$200M EBITDA (assuming a conservative $10,000/t LCE) starting in 2020. When one multiples that by 10 we would be about C$4 a share. Having said that I can make no predictions about the share price of Nemaska only to say that I believe we are undervalued here today.

TCI: This will definitely be the case when project financing can be arranged. Are there any things that could pose a risk, is Shawinigan fully permitted for operation for example? Are other operational permits pending or could anything else be of concern?

GB: Our risk mostly lies with the project financing, which we are currently working on. We are fully permitted and funded for the Phase 1 Plant and the commercial plant permitting is on-going and I don't see anything to hinder this process given our Phase 1 Plant is currently operational, using the same process as the commercial facility. The General Certificate of Authorization at the mine site is the overriding permit needed for construction and operations, and the other permits are filed as needed.

TCI: We are closing in on the end of this interview. Do you have any other interesting information for the audience, which might strengthen the case you are making for Nemaska?

GB: I believe that Nemaska Lithium is on the cusp of finalizing its project financing and the true value of all our work to date is about to be unlocked. Nemaska Lithium is extremely well positioned to take advantage of the current supply shortage for lithium. The lithium ion battery market is rapidly growing and in need of new suppliers. We are one of very few companies that can enter the chain of supply for battery compounds in the next five years. Finally, given the production from our Phase 1 Plant we will already be qualified as a supplier allowing us to be in the market immediately. This is an excellent position to be in.

TCI: Thank you Guy, and I do hope you can achieve your goal of funding capex at the end of Q3/beginning of Q4. The Whabouchi project will be derisked for the most part in that case, and it looks like a very interesting (re-)entry point by then, as a steady rerating seems inevitable towards production. The usual risks remain, of course; I'm assuming construction and ramp up goes well, lithium prices don't go below $10,000/t (now over $15,000/t and rising again), and stock market sentiment on the TSX remains neutral to positive during this period. Good luck with the project financing, and I will keep tracking this story closely.

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter on my website www.criticalinvestor.eu, and follow me on Seekingalpha.com, in order to get an email notice of my new articles soon after they are published.

The Critical Investor's Disclaimer:

The author is not a registered investment advisor, currently has a long position in this stock, and Nemaska Lithium is a sponsoring company. All facts are to be checked by the reader. For more information go to www.nemaskalithium.com and read the companys profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Shawinigan; location of plants

Shawinigan; location of plants

Want to read more Energy Report articles like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent articles with industry analysts and commentators, visit our Streetwise Articles page.

Streetwise Reports Disclosure:

1) The Critical Investor's disclosures are listed above.

2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Streetwise Reports does not accept stock in exchange for its services. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article.