The Gold Report: The Chinese yuan will soon join the International Monetary Fund (IMF) Special Drawing Rights (SDR) currency basket. The Chinese government hopes the yuan's inclusion will help undermine the U.S. dollar as the world's reserve currency. What will the likely impact be on gold?

Thibaut Lepouttre: Yes, the IMF has agreed to add the yuan to the SDR basket. At 11% the Chinese yuan will have a higher weighting in the SDR basket than either the Japanese yen or the British pound. But what's surprising is the rather small cut in the U.S. dollar ratio in the basket. The weighting will go down to 41.73% from 41.9%, just 0.17%. The Chinese will have to wait a few more years to see a significant cut in the weighting of the U.S. dollar.

"Callinex Mines Ltd. is definitely chasing an elephant on its Pine Bay zone."

What will be the effect on the gold price? Probably marginal because the weighting of the U.S. dollar remains virtually unchanged. It would have been different if all currencies had lost 10 or 11% of their value in the SDR basket. Then the U.S. dollar could have seen a sell off as central bankers around the world would be inclined to sell dollars to buy yuan for their reserves.

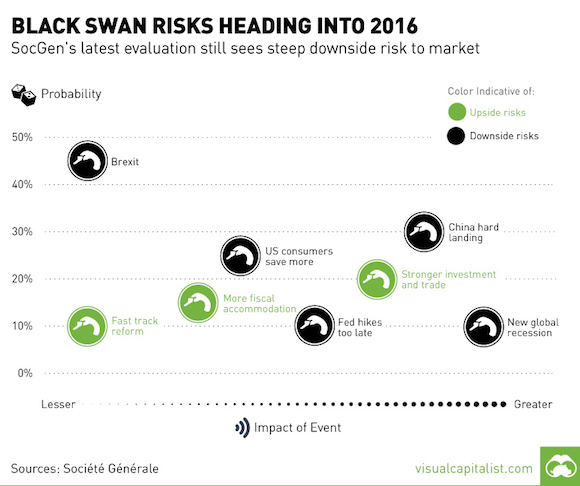

TGR: Vancouver-based Visual Capitalist recently posted an infographic outlining "black-swan" risks for 2016. Please rank the following in terms of what you believe could have the greatest impact on the gold price: Britain exiting the European Union, a hard landing of the Chinese economy, the Federal Reserve waiting too long to raise interest rates and U.S. troops on the ground in the Middle East.

TL: Having troops in the Middle East would probably have the biggest impact on the gold price because that would create the image of another war, which creates more uncertainty in the U.S. economy and society.

I would place Britain's exit from the European Union in the No. 2 spot because it has the potential to change the fundamentals of the European Union. If one country leaves, then what's holding back other countries like Greece or Italy to choose the easy way out?

"Integra Gold Corp.'s Triangle deposit is shaping up to be a massive project."

Third would be a hard landing by the Chinese economy. That could have some impact on the gold price, but if that happens, forced gold liquidation is a big risk. We saw that in August when a lot of gold and copper futures were sold to cover the margin calls in Chinese investment accounts.

And, finally, the U.S. Federal Reserve waiting too long to raise interest rates. The Federal Reserve is losing credibility. Most people tend to ignore its recent decisions. Let's see what happens in 2016.

TGR: Why hasn't the gold price reacted to greater global geopolitical uncertainty?

TL: Most investors are shrugging off geopolitical changes because we've had a lot of crises in the years since the global financial crisis. We had Greece collapsing and Spain almost collapsing. We had problems in Ireland. We had problems in Ukraine. Now we have problems in Syria. People are getting used to these things, and investors are asking: Why would we run to an asset class that has been slaughtered in the past three years? It's a combination of those factors.

TGR: Gold will likely end 2015 near a five-year low. How do you win as a precious metals equities investor in this market?

TL: The most important point is to do your homework. Investors need to find quality companies and follow them closely. Some companies with projects based in the U.S. or Canada obviously still have difficulty attracting investor attention even when they produce good results. One example is Columbus Gold Corp. (CGT:TSX.V; CBGDF:OTCQX), which drilled some game-changing holes on its Eastside gold project in Nevada. Columbus Gold has now set its sight on making a 10 million ounce (10 Moz) discovery as the mineralization at Eastside is more widespread than originally anticipated.

"The impact of the weak Colombian peso on Red Eagle Mining Corp. will be huge."

But the problem of poor share price performances largely seems limited to American and Canadian companies. In Australia, where the dollar has also lost ground to the U.S. dollar, similar to what has happened with the Canadian dollar, Australian gold producers and exploration companies are performing much better. Midcap producers like Regis Resources Ltd. (RRL:ASX) and Northern Star Resources Ltd. (NST:ASX) have more than doubled their share prices in the past 12 months. And Cardinal Resources Ltd. (CDV:ASX), an exploration play, has seen its share price quadruple over the last year on a multimillion-ounce discovery in Ghana.

TGR: Given the expected uncertainty in 2016, should investors boost their precious metals holdings? What role will equities play in that strategy?

TL: I'm convinced that precious metals should have some allocation in any portfolio as an insurance policy against tough times. For example, two years ago an ounce of gold in Russia cost about 40,000 rublesnow it's about 71,000 rubles. That's a 77% increase in the domestic currency, whereas the gold price in U.S. dollars decreased by 15%.

What role should precious metals equities play in such a strategy? Gold and silver mining companies obviously offer much higher leverage to the gold price. But it works both ways, so when the gold price goes down, mining equities get crushed. Mining equities should be part of the speculative portion of one's portfolio. It all depends on an investor's appetite for risk.

TGR: You continue to write reports on various companies. What are your top three picks for 2016?

TL: People have holidays coming up and they might want to do some research so I will give you five: Columbus Gold, Integra Gold Corp. (ICG:TSX.V; ICGQF:OTCQX), Red Eagle Mining Corp. (RD:TSX.V), Redstar Gold Corp. (RGC:TSX.V) and Focus Ventures Ltd. (FCV:TSX.V). Four of those are focused on gold, while Focus Ventures is developing a phosphate project in Peru.

TGR: Let's start with Columbus. The company has a considerable stake in the Paul Isnard gold project in French Guiana where Nordgold N.V. (NORD:LSE) is earning a 50% interest, but it also has the 10 Moz Eastside exploration-stage project in Nevada. With the combination of those two assets, does it become a likely takeover target?

"Redstar Gold Corp.'s Unga is an exceptional property with exceptional grades."

TL: Columbus is an important company to watch in 2016. The company not only has one horse in the stable with Paul Isnard, but also a promising exploration property in Nevada. Nordgold will likely try to acquire the remaining stake in Paul Isnard (as Nordgold has always bought out its minority partners in the past) and then spin off Eastside as part of a new company because Nordgold, as a Russian company, wouldn't really be welcome in the U.S. Nothing is guaranteed but I think Columbus Gold is a reasonable candidate for merger and acquisition activity, either by selling Paul Isnard or entering into a joint-venture agreement with a senior producer for Eastside.

TGR: Will Red Eagle ultimately win control of CB Gold Inc. (CBJ:TSX.V) in its battle with Batero Gold Corp. (BAT:TSX.V)?

TL: Yes, there will probably be an amicable solution in the next 1224 months. Red Eagle will likely have to acquire the remaining shares of CB Gold in a private transaction with Batero.

TGR: What impact is the weak Colombian peso having on Red Eagle?

TL: The impact will be huge. The U.S. dollar versus the Colombian peso exchange rate is about 3,150:1. Red Eagle based its feasibility study on an exchange rate of 1,900:1, so it gets about 6065% more pesos for each dollar. Some 30 or 40% of the company's operating expenses will be paid for in Colombian pesos and this means Red Eagle could shave off about 50% of those expenses, which could reduce the all-in sustaining costs by at least $100 per ounce ($100/oz). That would be an impact of $45 million ($45M) per year based on the 40,00045,000 ounce (4045 Koz) per year production rate. My hope is that the company will try to lock in at least a part of its currency exposure because it's prudent to hedge against the Colombian peso while it can get value.

TGR: Integra recently published an updated resource estimate for the Triangle gold deposit, part of its Lamaque South project in Val-d'Or, Québec. What were your first impressions of the Triangle resource?

TL: Just a few weeks before the resource estimate was published, I wrote that I was expecting the total to come in at 1.61.7 Moz, so at 1.67 Moz, I was quite happy. The Triangle zone now contains 1.2 Moz gold at a cutoff grade of 5 grams per ton (5 g/t). That's great because the average grade is around 9 g/t. That should be viable for any underground mine, especially considering that the orebody isn't too far from surface. There's much more to come at the Triangle zone, too, because 17,000 meters (17,000m) of drilling at Triangle was not included in the resource estimate. The next resource update will incorporate at least 30,000m of additional drilling at Triangle. It's shaping up to be a massive project.

TGR: Will Integra need to raise cash for further drilling?

TL: The company has $2527M in the bank, enough to drill another 100,000m in 2016. All is going well, and South Lamaque will contain more than 2 Moz in the not-so-distant future. Integra is doing the right thing by proving up ounces, despite the current state of the market.

TGR: Integra has found about five mineralized "C" structures at anywhere from 650750m underground. Tell us about those.

TL: Integra recently discovered a sixth "C" structure as well but these structures have not been completely drilled out. There's much more exploration potential at depth at Lamaque South but it doesn't always make sense for a small company like Integra to go after the deep ore when it can build a 12- or 13-year mine life on what it has right now. But there is no reason why the mineralization should not continue to a depth of 1,500 or 2,000m as it does at the nearby LaRonde mine owned and operated by Agnico Eagle Mines Ltd. (AEM:TSX; AEM:NYSE).

TGR: Redstar is a relatively new name on the gold exploration scene. Tell us about the Unga project in Alaska and some drill results to date on the Shumagin vein.

TL: I have been keeping my eye on it for quite a while because it is an exceptional property with exceptional grade. The historic resource estimate averages 28 g/t gold and 4 ounces per ton silver. That's awesome. Redstar will follow up on the historical drill results and then publish a resource estimate. Unga Island is uninhabited, so exploration work doesn't really disturb anyone and the company gets along with the Aleut people. Even though it's an uninhabited island, it's just a two-hour flight from Anchorage. Redstar has an interesting property, but a lot of additional work needs to be done to reach a critical mass at Unga Island.

TGR: What is Alaska like as a mining jurisdiction in comparison to other mining-friendly states like Nevada?

TL: I consider Alaska to be as lenient or more lenient than Nevada because almost the entire Alaskan economy is based on oil, gas and mining. I consider Alaska a fantastic jurisdiction. The weather in Nevada is obviously better, but if I had to choose between Alaska and Nevada as being a more mining-friendly destination, it would be a tough choice.

TGR: Focus Ventures has a rock phosphate project in Peru. Typically, you focus on gold. Why are you interested in phosphate?

"Rye Patch Gold Corp. is an excellent company."

TL: I get interested whenever there's a good opportunity, be it gold, phosphate or any other commodity. Focus's Bayovar 12 project is probably the most straightforward mining project in the world. Focus will remove 12 to 25m of overburden, which is basically just sand, to reach the phosphate layers, which are visible to the naked eye. Focus simply needs to wash the phosphate, concentrate it and ship to a port 30 kilometers (30km) away. It's probably the best project I have seen in a long time. The company should release the Bayovar 12 prefeasibility study before the end of 2015. I expect an after-tax net present value in excess of CA$300M based on the known mineralization. Its market cap is less than CA$15M, yet Focus should be able to get Bayovar 12 into production for less than US$50M.

TGR: Jurisdiction is playing a bigger role in selecting precious metals equities in a risk-averse market. What are your favorite mining jurisdictions?

TL: North America, some of the Latin American countries (definitely not Venezuela) and Australia are still the top tier mining jurisdictions. Investors should be cautious with other mining destinations, especially in Africa with the Democratic Republic of the Congo, Zimbabwe or South Africa. My golden rule is that you should only invest in countries where you would like to travel to for a non-safari vacation.

TGR: Callinex Mines Inc. (CNX:TSX.V; CLLXF:OTCQX) recently announced a 10,000m drill program at the Pine Bay project in Flin Flon, Manitoba. Is this an attempt to expand on the VMX discovery announced in September? When could we see results and what will you be looking to hear?

TL: Callinex will indeed be following up on the new discovery and the 10,000m drill program (split up in 6,000m this winter followed by an additional 4,000m in the summer) will try to find out if there's indeed a larger target around the discovery hole. You should keep in mind Placer Dome, which previously owned the property, had an exploration target of 30 million tonnes of rock, so Callinex is definitely chasing an elephant on its Pine Bay zone. Callinex's ultimate goal is to find a large mineralized structure that wouldn't only be appealing to HudBay Minerals as its 777 concentrator will be running out of feed, but would also be appealing for any other copper-focused producer.

TGR: What are some other companies that you're following with projects in North America?

TL: Rye Patch Gold Corp. (RPM:TSX.V; RPMGF:OTCQX) is an excellent company. It owns Lincoln Hill, a small open-pit gold project that is 23km from Coeur Mining Inc.'s (CDM:TSX; CDE:NYSE) Rochester mine in Nevada. Rye Patch's preliminary economic assessment (PEA) on Lincoln Hill envisions an open pit using a gold price of $775/oz, which is probably the most conservative economic study that I have seen in the past five years. That means the economics will be robust. The current mine plan calls for processing about 170 Koz gold and a little bit less than 4 Moz silver.

"TerraX Minerals Inc. is a prime takeover candidate because it has everything most senior producers would want."

But the real catalyst will be the results of ongoing metallurgical studies. The current PEA bases its economics on a run-of-mine heap-leap operation. But next door at Rochester, Coeur is crushing the ore before it reaches the leach pad and it is recovering roughly 92% of the gold. Rye Patch's PEA considers 65% a viable recovery rate. If Rye Patch could boost its recovery rate to 80 or 85%, more gold would be produced and lower-grade ore would become economic.

TGR: Why would Lincoln Hill get financing over similar projects?

TL: The initial capital expenditure would be about $30M, and if you add a crushing circuit that would rise to $3537M. That is financeable. Also, if Rye Patch boosts gold recoveries and production in the first few years of mine life, the internal rate of return could be in excess of 50%, even at $1,100/oz gold.

TGR: Are there other companies in North America that you follow?

TL: Another one is TerraX Minerals Inc. (TXR:TSX.V). It is a prime takeover candidate because the company has everything most senior producers would wanta huge land package in an attractive greenstone belt that once hosted two producing mines; it is a 15-minute drive from the airport, and there are trained mine laborers nearby. The first resource estimate, which I hope to see by mid-2016, should be between 1 and 2 Moz but with a clear exploration plan to add ounces.

TGR: How much working capital does TerraX have?

TL: The company has almost $5M in working capital and plans to use that to prove up as many ounces as possible. The management team and Osisko Gold Royalties Ltd. (OR:TSX) own about 33% of the outstanding shares, so the risk of a hostile takeover bid is minimal.

TGR: Any others in North America?

TL: Keep an eye on Pilot Gold Inc. (PLG:TSX), which is moving ahead with its two Nevada projects: Kinsley Mountain and Goldstrike. The company recently issued a maiden resource estimate for Kinsley Mountain, and it had two promising drill intercepts at Goldstrike. Pilot Gold has great projects and $10M in cash but the company wants to preserve capital, so it will likely scale back exploration in 2016.

TGR: Some companies that you follow, like Focus Ventures, have unconventional narratives. Give us a couple of those.

TL: I just visited Inca One Gold Corp.'s (IO:TSX.V) Chala One ore processing plant and the newly acquired plant from Montan Mining Corp. (MNY:TSX.V) called Mollehuaca. Inca One completed construction of the 100 ton-per-day (100 tpd) mill at Chala One and had it running at in excess of 100 tpd for a few days in the summer. Now the company is securing funding to buy more ore and get Mollehuaca running. Montan had placed it on care and maintenance as it was unable to acquire more ore, whereas Inca One might be in a better position to attract fresh cash.

TGR: Any others?

TL: Cancana Resources Corp. (CNY:TSX.V) operates a small-scale, high-grade manganese mine in Brazil, in a joint venture with a subsidiary of The Sentient Group. The company should be considered an exploration company, while it continues to produce small amounts of organic manganese that is essentially used as fertilizer, for instance for soy plants in Mato Grosso province. Cancana's plan is to more than double production to 50,000 tons (50 Kt) of manganese in 2016. At that level it could look at offtake agreements because most of the manganese production is being stockpiled. Cancana also plans to release a maiden resource estimate on its manganese property and there are about 60 drill targets that the joint-venture partners want to test in 2016.

TGR: Does the market understand a publicly traded manganese fertilizer story?

TL: I don't think that most people know that manganese isn't just used in the steel sector and that this type of manganese is mostly used as fertilizer due to its exceptional qualities. Cancana produces the highest-grade manganese in the world.

And finally, Blackheath Resources Inc. (BHR:TSX.V) also belongs in the list of "special" companies, as it's continuing to advance its tungsten projects in Portugal. The company completed a maiden resource estimate at the Covas project, drilled some nice and long intercepts at Borralha, and is now looking at the potential of the Bejanca project, which contains a mix of tin and tungsten.

TGR: We're nearing Christmas. Could you give investors an item to put in their stockings?

TL: I'll give you two. The first one is Cardinal Energy Ltd. (CJ:TSX), which has free cash flow at $45/barrel oil. It also pays a nice dividend that it can afford.

The other company is Jericho Oil Corp. (JCO:TSX.V). It's looking for undervalued assets in Kansas and Oklahoma. The company just announced an acquisition that will triple output to more than 300 barrels of oil per day. At current oil prices, Jericho will continue to look for and buy distressed assets for a few dozen cents on the dollar. Those are two Christmas "stocking stuffers" that are long plays in the oil space, because let's be honest, do you see the oil price below $40 in three years from now?

TGR: Thank you for your insights and enjoy the holiday season.

Thibaut Lepouttre is the editor of the Caesars Report, a newsletter and mining portal based in Belgium that covers several junior mining companies with a special focus on precious metals and base metals. Lepouttre has a Bachelor of Law degree and two economics masters degrees that have forged his analytical approach to the mining sector. Considered a number cruncher, Lepouttre focuses on the valuations of companies and is consistently on the lookout for the next undervalued mining company.

Read what other experts are saying about:

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

DISCLOSURE:

1) Brian Sylvester conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report and The Life Sciences Report, and provides services to Streetwise Reports as an independent contractor. He owns, or his family owns, shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of Streetwise Reports: Columbus Gold Corp., Callinex Mines Inc., Integra Gold Corp., Pilot Gold Inc., Red Eagle Mining Corp., Redstar Gold Corp., Rye Patch Gold Corp. and TerraX Minerals Inc. The companies mentioned in this interview were not involved in any aspect of the interview preparation or post-interview editing so the expert could speak independently about the sector. Streetwise Reports does not accept stock in exchange for its services.

3) Thibaut Lepouttre: I own, or my family owns, shares of the following companies mentioned in this interview: Cardinal Energy Inc., Jericho Oil Corp., Focus Ventures Ltd., Blackheath Resources Inc., Columbus Gold Corp., Integra Gold Corp., Inca One Gold Corp., Rye Patch Gold Corp., Red Eagle Mining Corp., Cancana Resources Corp. and Callinex Mines Inc. I personally am, or my family is, paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: Focus Ventures Ltd., Blackheath Resources Inc., Rye Patch Gold Corp., Cancana Resources Corp., Inca One Gold Corp., Integra Gold Corp., Columbus Gold Corp. and Callinex Mines Inc. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I determined and had final say over which companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts' statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.